- United States

- /

- Consumer Finance

- /

- NasdaqGS:CACC

Top Growth Companies With Insider Ownership On US Exchanges October 2024

Reviewed by Simply Wall St

As the U.S. stock market experiences gains following a strong jobs report, investor confidence in the economy is bolstered despite recent volatility and geopolitical tensions. In this environment, growth companies with significant insider ownership can offer unique insights into potential opportunities, as insiders' vested interests often align closely with shareholder value creation.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| GigaCloud Technology (NasdaqGM:GCT) | 25.7% | 24.3% |

| Atour Lifestyle Holdings (NasdaqGS:ATAT) | 26% | 23.2% |

| Victory Capital Holdings (NasdaqGS:VCTR) | 10.2% | 32.2% |

| Atlas Energy Solutions (NYSE:AESI) | 29.1% | 42.1% |

| Super Micro Computer (NasdaqGS:SMCI) | 25.7% | 28.0% |

| Hims & Hers Health (NYSE:HIMS) | 13.8% | 41.3% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.4% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 14.0% | 95% |

| BBB Foods (NYSE:TBBB) | 22.9% | 51.2% |

| Carlyle Group (NasdaqGS:CG) | 29.5% | 22% |

Let's explore several standout options from the results in the screener.

Credit Acceptance (NasdaqGS:CACC)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Credit Acceptance Corporation provides financing programs and related products and services in the United States, with a market cap of approximately $5.27 billion.

Operations: The company generates revenue of $815.20 million from offering dealers financing programs and related products and services in the United States.

Insider Ownership: 14.1%

Credit Acceptance shows potential as a growth company with high insider ownership, despite recent financial challenges. The company's revenue is forecasted to grow significantly faster than the US market, at 51.9% annually. However, profit margins have decreased from 35.6% to 22.3%, and there has been substantial insider selling recently. Recent debt financing agreements extended credit facilities and adjusted interest rates, reflecting strategic financial management amid a net loss of US$47.1 million in Q2 2024.

- Delve into the full analysis future growth report here for a deeper understanding of Credit Acceptance.

- Our expertly prepared valuation report Credit Acceptance implies its share price may be lower than expected.

MediaAlpha (NYSE:MAX)

Simply Wall St Growth Rating: ★★★★★★

Overview: MediaAlpha, Inc. operates an insurance customer acquisition platform in the United States and has a market cap of approximately $1.19 billion.

Operations: The company's revenue segment is primarily from Internet Information Providers, generating $496.67 million.

Insider Ownership: 12.5%

MediaAlpha, Inc. demonstrates growth potential with significant revenue increases, reporting US$178.27 million in Q2 2024 compared to US$84.77 million a year ago, and forecasts annual revenue growth of 22.7%, outpacing the US market average. Despite past shareholder dilution, its return on equity is projected to be very high in three years. The recent extension of its partnership with Insurify may enhance its market position as it connects insurers with high-intent shoppers through a robust technology platform.

- Unlock comprehensive insights into our analysis of MediaAlpha stock in this growth report.

- Our comprehensive valuation report raises the possibility that MediaAlpha is priced higher than what may be justified by its financials.

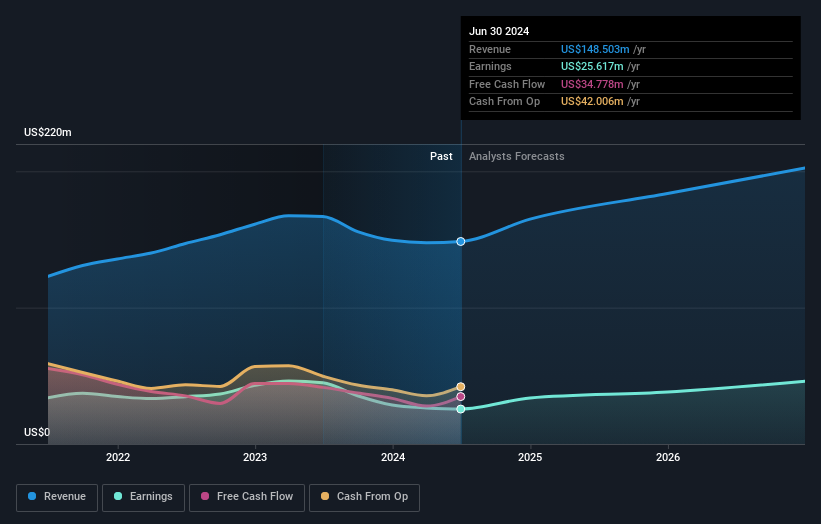

SmartFinancial (NYSE:SMBK)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: SmartFinancial, Inc. is a bank holding company for SmartBank, offering financial services to individuals and corporate customers in Tennessee, Alabama, and Florida, with a market cap of $480.48 million.

Operations: The company's revenue segment, totaling $148.50 million, is derived from offering a variety of financial services to both individual and corporate clients across Tennessee, Alabama, and Florida.

Insider Ownership: 17%

SmartFinancial's earnings are projected to grow significantly at 21.1% annually, outpacing the US market, though revenue growth is slower at 12.4%. Recent financials show a drop in net income and profit margins compared to last year. Despite low substantial insider buying recently, more shares were bought than sold by insiders over three months. The company trades well below its estimated fair value and has completed a share buyback program worth US$8.45 million since 2018.

- Click here to discover the nuances of SmartFinancial with our detailed analytical future growth report.

- In light of our recent valuation report, it seems possible that SmartFinancial is trading beyond its estimated value.

Turning Ideas Into Actions

- Access the full spectrum of 183 Fast Growing US Companies With High Insider Ownership by clicking on this link.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CACC

Credit Acceptance

Engages in the provision of financing programs, and related products and services in the United States.

Exceptional growth potential with imperfect balance sheet.