- United States

- /

- Banks

- /

- NasdaqGS:STBA

Exploring 3 Undervalued Small Caps With Notable Insider Buying

Reviewed by Simply Wall St

The United States market has remained flat over the last week, yet it has shown a 7.8% increase over the past 12 months with earnings forecasted to grow by 14% annually. In this context, identifying small-cap stocks that appear undervalued and have notable insider buying can be an intriguing opportunity for investors seeking potential growth in a steady market environment.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Shore Bancshares | 10.6x | 2.4x | 6.47% | ★★★★★☆ |

| First United | 9.7x | 2.6x | 46.65% | ★★★★★☆ |

| MVB Financial | 11.5x | 1.6x | 26.97% | ★★★★☆☆ |

| S&T Bancorp | 11.0x | 3.8x | 41.45% | ★★★★☆☆ |

| Thryv Holdings | NA | 0.8x | 13.13% | ★★★★☆☆ |

| German American Bancorp | 17.1x | 5.7x | 49.30% | ★★★☆☆☆ |

| West Bancorporation | 14.3x | 4.4x | 42.41% | ★★★☆☆☆ |

| PDF Solutions | 193.3x | 4.4x | 18.93% | ★★★☆☆☆ |

| Delek US Holdings | NA | 0.1x | -199.46% | ★★★☆☆☆ |

| Titan Machinery | NA | 0.2x | -368.51% | ★★★☆☆☆ |

Let's take a closer look at a couple of our picks from the screened companies.

Potbelly (NasdaqGS:PBPB)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Potbelly operates a chain of sandwich shops and has a market cap of $0.09 billion.

Operations: Revenue primarily comes from Potbelly Sandwich Shops, with gross profit margin showing an upward trend, reaching 35.70% by the end of 2024. Costs of goods sold (COGS) and operating expenses are significant components of the cost structure, impacting overall profitability. Despite fluctuations in net income over time, recent periods indicate a positive net income margin improvement to 8.71%.

PE: 7.1x

Potbelly, a small but expanding player in the fast-casual dining sector, recently reported a full-year net income surge to US$40.29 million from US$5.12 million the previous year, despite a slight revenue dip. Insider confidence is evident with recent share purchases by company insiders. Franchise agreements across multiple states, including Virginia and Texas, highlight Potbelly's strategic growth ambitions to bolster its market presence while contributing to local economies through job creation. However, potential investors should note that earnings are forecasted to decline significantly over the next three years due to reliance on external borrowing for funding expansion efforts.

- Take a closer look at Potbelly's potential here in our valuation report.

Examine Potbelly's past performance report to understand how it has performed in the past.

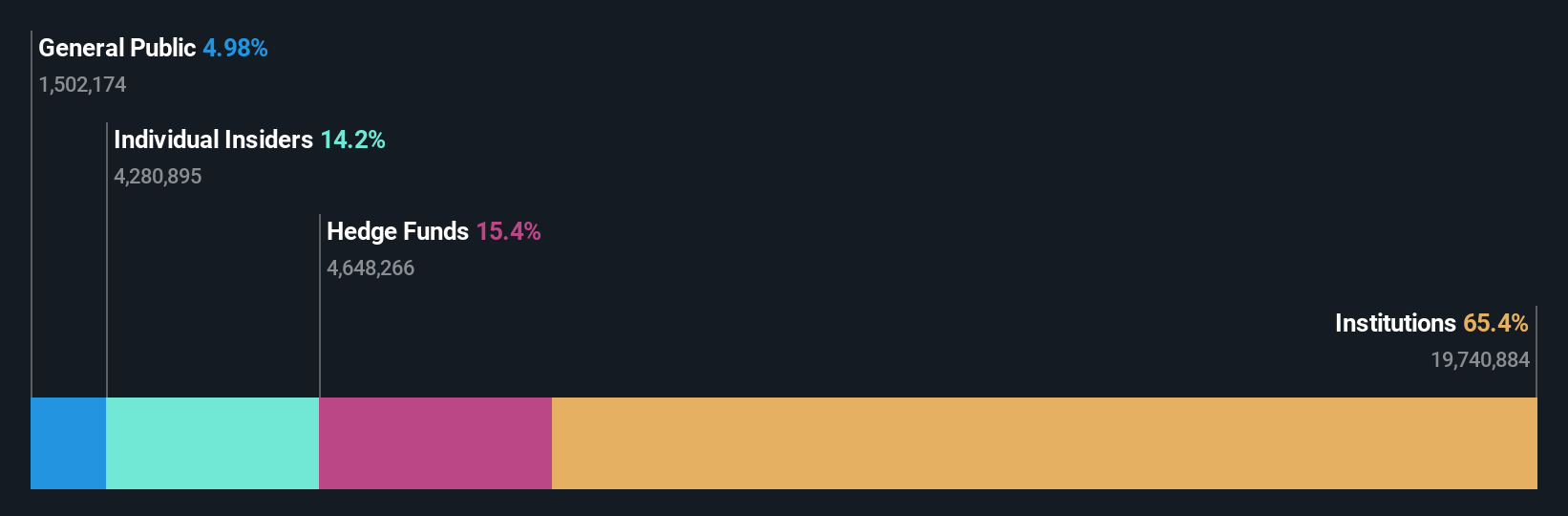

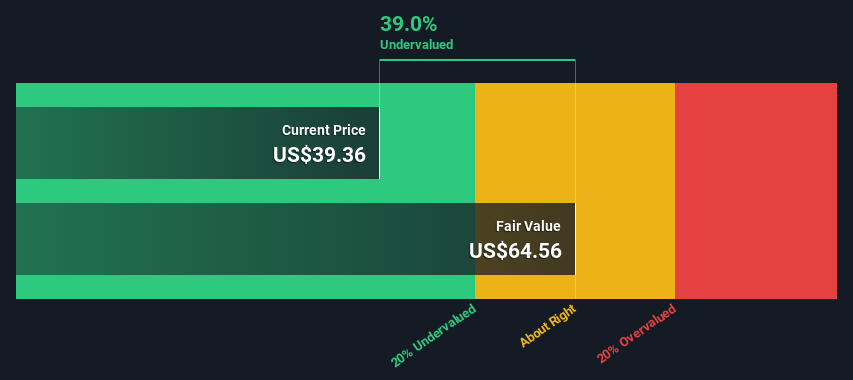

S&T Bancorp (NasdaqGS:STBA)

Simply Wall St Value Rating: ★★★★☆☆

Overview: S&T Bancorp is a financial holding company that provides a range of community banking services, with operations focused on offering personal and commercial banking products.

Operations: Revenue predominantly stems from community banking, with a reported $383.76 million in the latest period. The gross profit margin consistently stands at 100%, indicating no cost of goods sold is reported. Operating expenses, mainly driven by general and administrative costs amounting to $175.63 million, significantly impact net income margins which fluctuate around 34%.

PE: 11.0x

S&T Bancorp, a small yet significant player in the financial sector, recently reported a decline in earnings for 2024. Net interest income fell to US$334.81 million from US$349.41 million the previous year, while net income decreased to US$131.27 million from US$144.78 million. Despite these challenges, they raised their quarterly dividend by 3% to US$0.34 per share, reflecting confidence in future stability and potential growth within the industry context despite forecasted earnings declines over the next three years.

- Click here and access our complete valuation analysis report to understand the dynamics of S&T Bancorp.

Gain insights into S&T Bancorp's past trends and performance with our Past report.

Tompkins Financial (NYSEAM:TMP)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Tompkins Financial operates as a financial services company providing banking, insurance, and wealth management services with a market capitalization of $0.91 billion.

Operations: The company generates revenue primarily from banking, insurance, and wealth management services. Operating expenses are a significant component of its financial structure, with general and administrative expenses consistently forming a large portion. The net income margin has shown variability over time, reaching as high as 31.13% but also declining to 3.29% in recent periods.

PE: 13.2x

Tompkins Financial, a small-cap entity in the U.S., displays potential value with its recent earnings growth. For Q4 ending December 31, 2024, net interest income rose to US$56.28 million from US$52.36 million the previous year, while net income increased to US$19.66 million from US$15 million. Basic earnings per share grew to US$1.38 from last year's US$1.06, highlighting operational efficiency despite no recent share repurchases or insider confidence activities noted recently. Earnings are projected to grow annually by nearly 12%, indicating promising future prospects for investors seeking opportunities in smaller companies with growth potential.

Taking Advantage

- Navigate through the entire inventory of 88 Undervalued US Small Caps With Insider Buying here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade S&T Bancorp, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:STBA

S&T Bancorp

Operates as the bank holding company for S&T Bank that provides retail and commercial banking products and services to consumer, commercial, and small business in Pennsylvania and Ohio.

Very undervalued with flawless balance sheet and pays a dividend.

Market Insights

Community Narratives