Quote of the Week: “Tariffs are taxes that are stagflationary for the world as a whole, more deflationary for the tariffed producer, and more inflationary for the importer that imposes the tariffs.” - Ray Dalio (from his recent post )

Our recent updates have been pretty US-heavy, and for good reason. Trump’s “shock and awe” approach to trade (with a side of WTF) has kept markets guessing. But with tariffs now hitting global markets hard, it’s time to zoom out.

We’re kicking things off with what these new tariffs could mean for companies exporting to the US. Then, we’ll dig into how key global markets are positioned, looking at valuations, earnings expectations, and where money might flow next.

Spoiler: There’s more going on than just the headlines.

🎧 Would you prefer to listen to these insights? You can find the audio version on our Spotify, Apple Podcasts or YouTube!

What Happened in Markets This Week?

Here’s a quick summary of what’s been going on:

💸 Amazon joins list of TikTok bidders ( CNBC )

- Amazon has submitted a last-minute bid to acquire TikTok’s U.S. operations, aiming to scoop up the app just days before a potential ban deadline hits on April 5.

- The move follows TikTok’s push into e-commerce and a previous partnership with Amazon that let users shop directly from videos.

- If Amazon pulls this off, it gets 170M U.S. users and a ready-made video commerce engine—plus a shot at owning the next-gen shopping funnel. But with regulatory headwinds and political skepticism high, the odds look slim. Either way, watch Amazon’s moves for future social shopping plays.

💳 Visa bids $100m to replace Mastercard as Apple’s credit card partner ( Reuters )

- Visa is dangling $100M to steal the Apple Card from Mastercard, aiming to become Apple’s new network partner.

- Apple is shopping for a new issuer after breaking up with Goldman Sachs, with Amex, Barclays, Synchrony, and JPMorgan also in the mix.

- A Visa-Apple deal could tighten Visa's grip on premium card users and pressure Mastercard’s market share. If Amex snags both the issuing and network roles, it could boost its card volume significantly. This is also a wake-up call: Big Tech’s financial partnerships are fluid and increasingly up for grabs.

- Keep an eye on Visa, Amex, and Mastercard. Whoever lands Apple wins a major boost in transaction volume and brand visibility.

🏰 Trump to charge tariffs of up to 50% on 'worst offenders' globally ( BBC )

- Trump just unveiled across-the-board tariffs: a 10% baseline on all imports, with sharply higher rates on countries like China (up to 54%), the EU (20%), and smaller export-heavy nations like Vietnam (49%).

- These new levies hit trillions in trade, target supply chain hubs, and yank tax-free status from Chinese e-commerce packages (think Shein and Temu). Markets were bracing for a 15-20% average tariff rate, but Trump delivered closer to 30%, pushing the U.S. into century-high protectionism.

- Prices are set to rise, corporate margins will get squeezed, and global growth could take a hit. Megacap stocks exposed to China, like Apple, Amazon, and Nike, slumped after hours, signaling broader market pressure ahead. Recession risks are rising, and a rebound isn’t guaranteed with tit-for-tat retaliation a real possibility. Analysts say these tariffs are likely to stick, so don’t expect a quick fix.

- Global trade just got a lot messier, so investors ar e rebalancing toward domestic-facing sectors and bracing for inflation shocks.

💊 Hims & Hers to sell Eli Lilly’s Zepbound on its platform ( Sherwood )

- Hims & Hers is now offering Eli Lilly’s Zepbound, a popular weight-loss drug, on its platform at full retail price ($1,899/month).

- The move follows an FDA decision that cut off Hims' ability to sell cheaper, compounded semaglutide, which had been a major revenue source.

- This deal gives Hims a path back into the GLP-1 game, but pricing may limit traction. Without discounts like those offered by Ro or Amazon, user adoption could be soft. The company’s revenue recovery now hinges on higher-priced, branded options rather than inexpensive compounded drugs.

- Hims is back in the weight-loss race, but without pricing power, investor expectations should stay measured.

👕 Clothing prices could surge if these tariffs stick ( Axios )

- Trump’s new tariffs hit apparel hard, with steep duties on imports from China, Vietnam, and Bangladesh—three countries that supply over half of U.S. clothing and shoes.

- 👕The U.S. makes just 3% of its own apparel, so costs will rise fast, and working-class consumers will feel it first.

- Expect margin pressure for retailers like Walmart and Nike and potential demand shifts toward discount or secondhand markets. Domestic manufacturing won’t fill the gap anytime soon because labor is too costly and capacity too low. The retail sector may face prolonged pricing and inventory challenges.

- Price hikes and squeezed margins are almost inevitable, so some investors are reassessing their retail exposure, especially to apparel-heavy names.

⏱️ The clock never stops ticking on America’s national debt problem ( Sherwood )

- The U.S. could hit its debt ceiling “X-date” as early as May, according to the CBO, risking missed payments on Social Security, military salaries, and more.

- With the national debt now at $36.1 trillion, which is 98% of GDP, and rising fast. Washington is staring down yet another fiscal standoff just months into 2025.

- A drawn-out ceiling battle could trigger market volatility, higher Treasury yields, and flight to safety. Any sign of actual default—even if brief—could spark a downgrade or liquidity crunch. The debt trajectory also raises long-term inflation and interest rate risks.

- Some investor are bracing for a bumpy summer, trimming their risk-on exposure, watching bond yields, and avoiding overexposure to U.S. government-dependent sectors.

💥 Liberation Day: Tariff Shock Hits Harder Than Expected

Despite months of tough talk, the actual tariffs dropped on Wednesday still managed to surprise the market. They’re bigger, broader, and blunter than expected.

Some see a global recession on the horizon. Others are still hoping this is a classic case of negotiating through chaos. Ray Dalio chimed in last week , warning that a lot of what happens from here, depends on second-order effects like currency moves, policy shifts, and reciprocal tariffs.

The bottom line is don’t bet on a single outcome. But buckle up, it feels safe to assume that volatility is likely here to stay.

⚖️ Tariffs Will Hit Unevenly Across Consumers and Companies

It’s not just who gets hit, but how hard. Foreign manufacturers are clearly in the firing line, but the pain will vary:

- 🥫 Essential goods might still find buyers, even at higher prices.

- 🎮 Discretionary items? Not so lucky.

- 💸 Lower-income US consumers will feel the pinch more, they rely more on imported goods and have less wiggle room.

- 🌍 Foreign exporters from lower-tariff countries will have a leg up on pricier peers.

In many cases, imported products will still be cheaper than US-made equivalents—but wallets have limits.

✨ Expect selective demand destruction. Consumers will stretch for some goods and drop others entirely.

🌅 Silver Linings Are Out There… Sort Of

Yes, the tariff wave is mostly bad news, but a few bright spots could emerge:

- ✂️ Rate cuts are back on the table if recession fears grow.

- 🏛️ Fiscal stimulus, especially in infrastructure, could support select sectors.

Infrastructure investment is great news for companies dealing with construction and materials. Real estate and homebuilders would also benefit from lower borrowing costs, and high-dividend sectors like utilities could shine in a lower-rate world.

Countries with strong balance sheets, like Germany, are best positioned to open the fiscal floodgates.

Also worth noting: not all tariff pain will be permanent. Loopholes and exemptions are almost inevitable, especially for goods the US can’t produce or for countries with leverage to boost US imports.

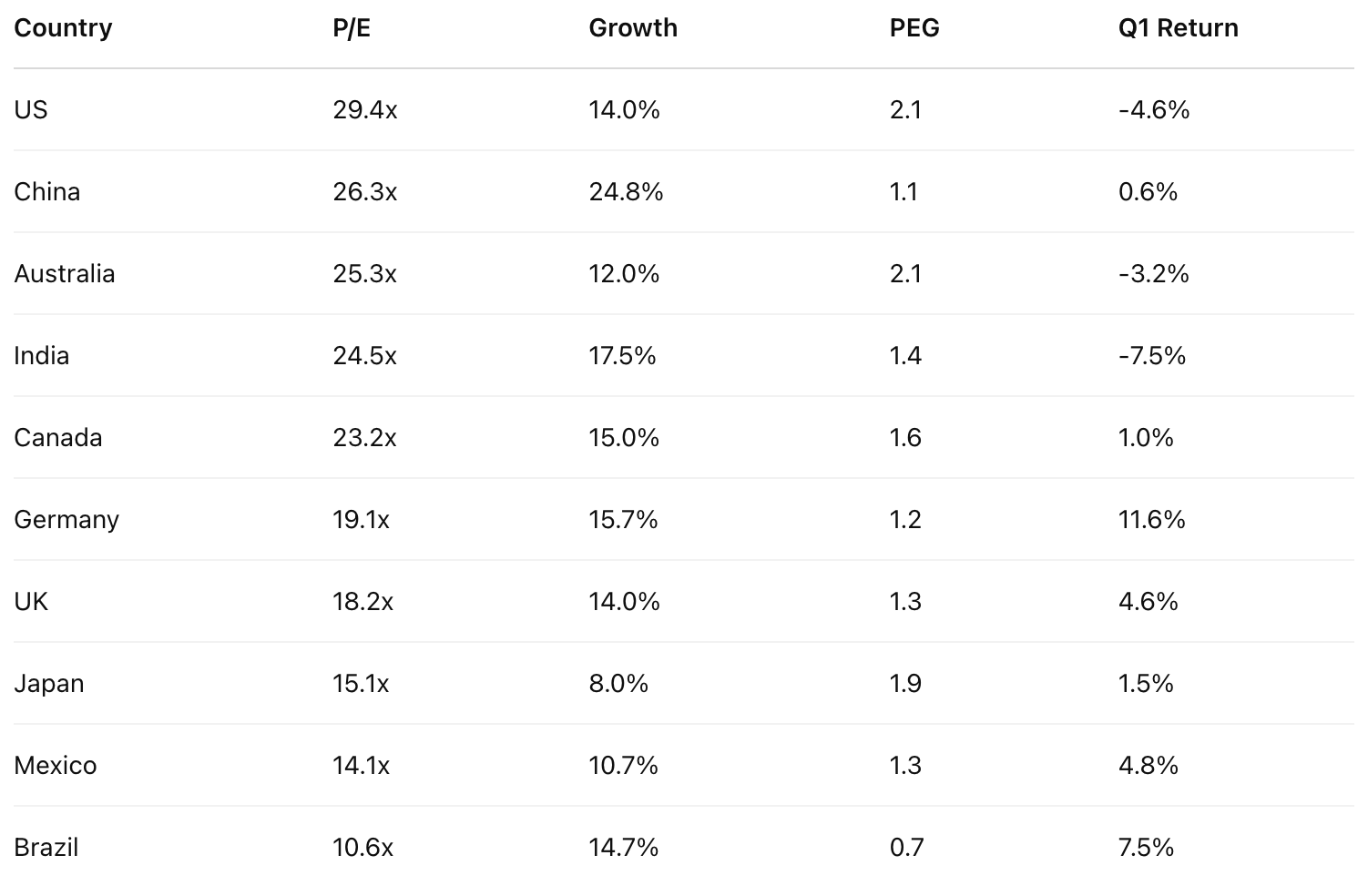

📊 Global Valuations: Who’s Cheap, Who’s Not?

Here’s a quick snapshot of P/E ratios, expected earnings growth, and PEG ratios across major markets.

👀 PEG ratios help normalize these numbers—and the median sits around 1.4x. The US and Australia look stretched, while Brazil, China, and Germany offer more value on paper.

PEG ratios don’t necessarily imply that a market or stock price is ‘cheap’ or ‘expensive’, but they do give us an indication of expectations for growth.

As always, it’s not just the multiples, it’s how reality stacks up against expectations. If US companies stumble, the rotation trade could gain more momentum.

As we mentioned last week, there was quite a lot of rotation during the first quarter. Whether that continues could depend on how US companies live up to what investors are expecting. Money must go somewhere, so some markets could benefit from being the best alternative, even if the outlook is only mediocre.

Below we take a closer look at six of these markets.

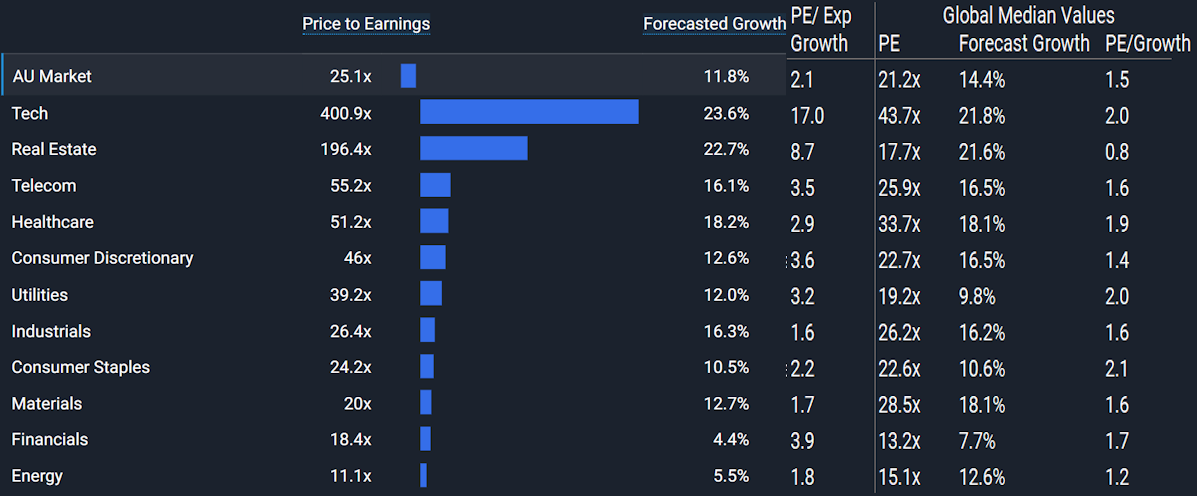

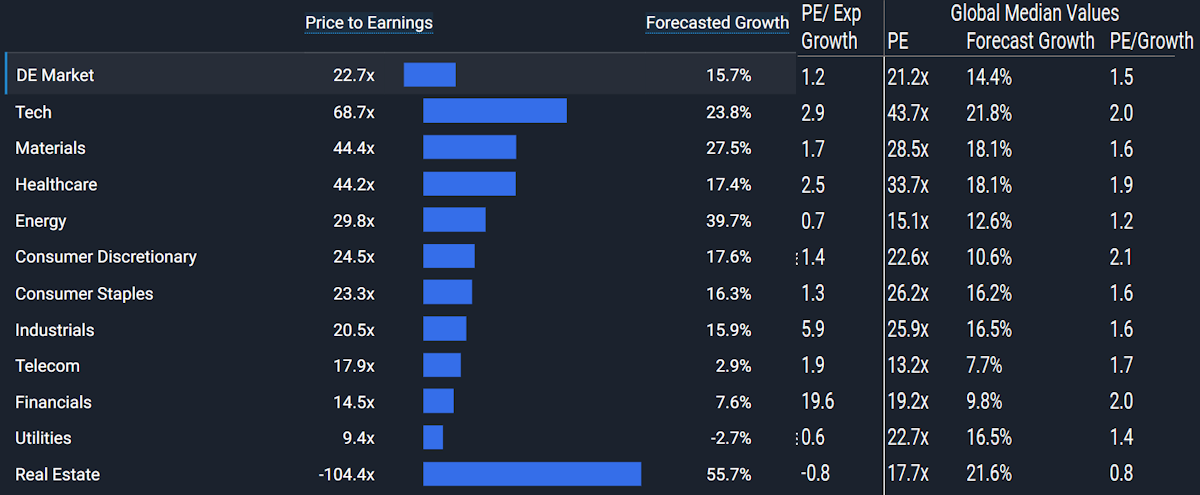

🇦🇺 Australia: High Multiples, Modest Growth

The image below lists the PE ratios and forecast earnings growth rates for each sector in Australia, along with the PE/Forecast Growth (PEG) ratio. The columns on the right are the median values for the 10 markets listed above, and a rough approximation for global sector valuations.

Australia’s market is trading at 25x earnings—about average historically—but earnings growth of just 12% leaves it looking pricey.

✨ The PEG ratio of 2.1 is inflated by the tech sector, but even other sectors trade above global averages.

On a positive note, the “baseline” 10% tariff from the US (versus 25% for many others) could give Aussie exporters a relative edge.

🇨🇦 Canada: Tariff Watch Continues

Canada's facing a mixed bag. For now, the original 25% tariff still applies, but there's potential for that to be rolled back under the USMCA trade framework.

- ⚙️ Sectors like autos, steel, and aluminum remain exposed, and there’s always the risk of escalation.

- 📉 Materials are vulnerable to both tariffs and slower global growth.

- 🏠 Real estate and financials could rebound if rates fall and expectations remain low.

PEG ratios here are close to the global median, but sentiment may shift fast if trade tensions ease.

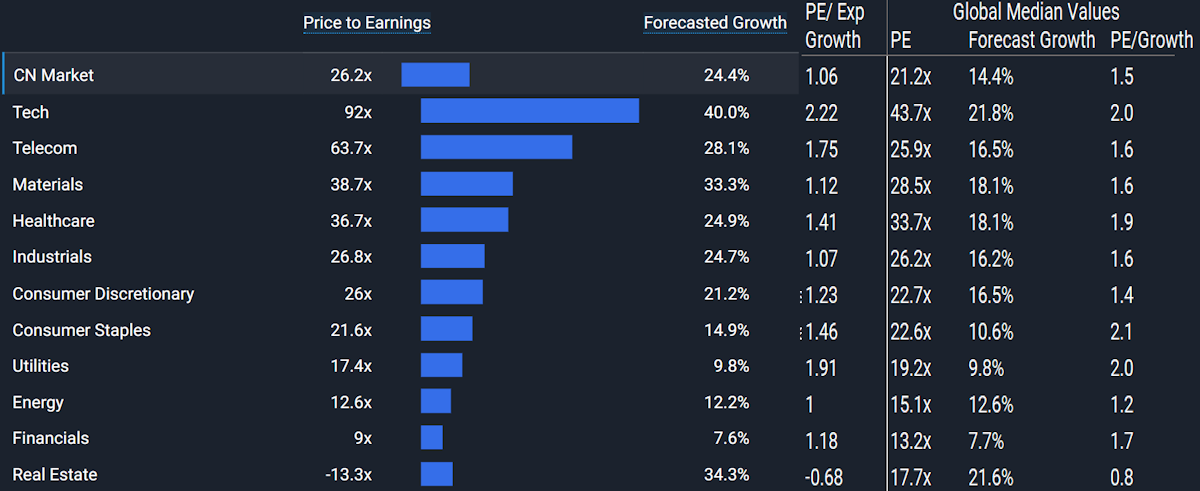

🇨🇳 China: Back in the Crosshairs (But With a Twist)

A 54% tariff is brutal, but funnily enough, China may actually reclaim lost ground.

- 🌏 Countries like Vietnam and Cambodia, once seen as alternatives, now face even higher tariffs.

- 🧱 But real estate woes and local government debt still weigh heavily.

- 🔧 Government intervention remains a major risk factor for investors.

Tech names and stimulus-aligned sectors may still find favor. But for now, many analysts believe China looks like a value trap with a few exceptions.

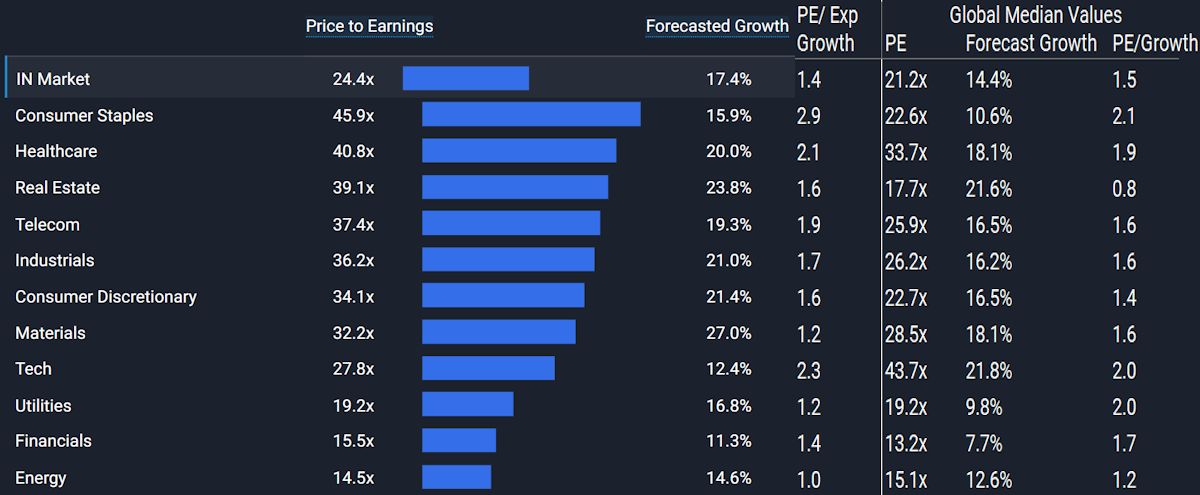

🇮🇳 India: Solid Story, But Momentum’s Missing

India’s market lost steam in late 2024 as valuations peaked and China rolled out heavy stimulus.

Q4 earnings were softer, and investors have yet to re-engage, but fundamentals remain strong:

- 📈 Domestic inflows are picking up.

- 📉 Exports to the US will face a 27% tariff, which is lower than most of Asia.

- 🇮🇳 India’s economy is less reliant on US trade and more on internal growth and development.

There’s potential for a US-India trade deal down the line. But for now, the bigger story remains India’s own industrialization wave.

🇩🇪 Germany: Tariff Trouble Meets Fiscal Firepower

Germany’s powerhouse auto sector is directly in the firing line, thanks to Trump’s 25% tariff on vehicles and parts. Add to that a blanket 20% tariff on all German exports, which is the highest among European peers, and you’ve got a serious headwind.

- 💊 Exceptions may be carved out for pharmaceuticals, but most industries are bracing for impact.

- 📉 Valuations are already below global averages in several sectors, and expectations are subdued.

- 💸 Meanwhile, Germany is breaking with its tradition of fiscal restraint to fund defense spending.

The country is in a strong position to use debt to reignite its economy, and possibly that of its neighbors.

🇬🇧 UK: Cheap Stocks, But Few Catalysts

The UK economy hasn’t grown much in the last decade, and its equity market has reflected that. Most listed companies earn abroad, which helps, but not enough to excite investors just yet.

- 📊 Valuations are low, but there’s no clear growth story to trigger a re-rating.

- 🇬🇧 Post-Brexit, the UK enjoys a lower tariff rate than the EU, which could be a bargaining chip.

- 💷 Lower rates would help if recession fears come true, though there’ll likely be more pain before relief.

If capital rotates out of the US, UK stocks may catch a bid purely on relative value. But for now, it’s a contrarian play.

💡 The Insight: Think in Decades, Not Months

Donald Trump isn’t just tweaking trade policy, he’s trying to redesign the global economic order. It’s a massive experiment, and financial markets are the testing ground. The outcomes are still wildly uncertain.

🧠 For investors and analysts alike, forecasting just got a whole lot harder. So what can you actually do about it?

- ✅ Stick with companies that have a clear competitive edge and a proven track record. Moats matter, especially in chaotic environments.

- 🔁 Diversify not just by sector, but by business model and geographic focus.

- 💵 Be picky with valuations. A margin of safety can cushion plenty of shocks.

- 📉 It’s incredibly tricky to try and time the market, so dollar-cost averaging (both for buying and selling) can be a useful method here.

✨ Long-term thinking isn't just good investing, it’s also how you stay sane when headlines get noisy.

Key Events During the Next Week

There’s not a huge lineup of economic data next week, but we do get several sentiment indicators—and they’ll help reveal how consumers, businesses, and central bankers are feeling post-tariffs.

Here’s what’s on deck and why it matters for investors:

Monday

- 🇩🇪 Germany Trade Surplus

- Forecast: $17.4B , up from $16B

- ➡️ Why it matters: A growing trade surplus signals strong exports. That’s bullish for Germany’s industrial sector, especially important as the country braces for US tariffs.

Tuesday

- 🇦🇺 Australia Westpac Consumer Confidence

- Expected to dip 0.9% to 95 (after a 4% rise in Feb)

- ➡️ Why it matters: Confidence impacts spending. A dip could signal softer demand ahead for Aussie retailers and services.

- 🇦🇺 Australia NAB Business Confidence

- Forecast: -3 vs. -1 last month

- ➡️ Why it matters: Weak sentiment from businesses often precedes slower hiring or investment, watch the sectors most reliant on domestic demand.

- 🇨🇦 Canada Ivey PMI

- Expected to fall to 48 , from 55

- ➡️ Why it matters: A reading below 50 indicates contraction. Could point to slowing momentum in Canada’s economy, which would influence rate cut expectations.

Wednesday

- 🇺🇸 FOMC Meeting Minutes

- ➡️ Why it matters: Investors will parse every word for clues on the Fed’s next move. Any dovish tilt could boost rate-sensitive sectors like real estate and tech.

Thursday

- 🇺🇸 US Inflation (CPI)

- Headline: 2.5% , down from 2.8%. Core: 3.0% , down from 3.1%.

- ➡️ Why it matters: Inflation is still the Fed’s top concern. A cooler reading could strengthen the case for rate cuts, good news for growth stocks and housing.

- 🇺🇸 Initial Jobless Claims

- Forecast: 226K , up from 219K

- ➡️ Why it matters: A rising trend here could flag cracks in the labor market, adding pressure on the Fed to act.

Friday

- 🇨🇳 China New Loans

- Expected: CNY 4T , up from CNY 1T in Feb

- ➡️ Why it matters: A big jump in lending could signal a fresh round of stimulus—bullish for commodities and China-exposed companies.

- 🇬🇧 UK Manufacturing Production

- Forecast: -3% YoY , down from -1.5%

- ➡️ Why it matters: A deeper contraction could reinforce the UK’s sluggish growth narrative—watch for pressure on industrial and cyclical names.

- 🇺🇸 US Producer Prices (PPI)

- Expected: 3.0% , down from 3.2%

- ➡️ Why it matters: Like CPI, this feeds into inflation expectations. A soft print here would support the “rates are coming down” story.

- 🇺🇸 University of Michigan Consumer Sentiment

- Forecast: 56.4 , slightly down from 57

- ➡️ Why it matters: This index is a solid early read on consumer mood. Lower sentiment could weigh on retail and discretionary sectors.

And just like that, the first quarter earnings season kicks off on Friday with the first of the big banks. Earlier in the week a handful of notable companies are due to report.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Richard Bowman

Richard is an analyst, writer and investor based in Cape Town, South Africa. He has written for several online investment publications and continues to do so. Richard is fascinated by economics, financial markets and behavioral finance. He is also passionate about tools and content that make investing accessible to everyone.