Advertisement

- United States

- /

- Tech Hardware

- /

- NasdaqGM:PMTS

Exploring December 2024's Undervalued Small Caps With Insider Action In US

Simply Wall St

Reviewed by Simply Wall St

Over the last 7 days, the United States market has experienced a 4.0% drop, yet it remains up by 24% over the past year with anticipated earnings growth of 15% per annum in the coming years. In this dynamic environment, identifying promising small-cap stocks with insider activity can offer investors unique opportunities to capitalize on potential market inefficiencies.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Capital Bancorp | 14.6x | 3.0x | 46.01% | ★★★★☆☆ |

| Franklin Financial Services | 10.0x | 2.0x | 38.82% | ★★★★☆☆ |

| McEwen Mining | 4.0x | 2.1x | 47.75% | ★★★★☆☆ |

| ProPetro Holding | NA | 0.6x | 40.11% | ★★★★☆☆ |

| First United | 13.7x | 3.1x | 47.37% | ★★★☆☆☆ |

| Limbach Holdings | 36.7x | 1.9x | 43.29% | ★★★☆☆☆ |

| RGC Resources | 17.3x | 2.4x | 21.29% | ★★★☆☆☆ |

| Community West Bancshares | 18.7x | 2.9x | 42.25% | ★★★☆☆☆ |

| Delek US Holdings | NA | 0.1x | -58.79% | ★★★☆☆☆ |

| Sabre | NA | 0.5x | -83.42% | ★★★☆☆☆ |

We're going to check out a few of the best picks from our screener tool.

OneWater Marine (NasdaqGM:ONEW)

Simply Wall St Value Rating: ★★★★★☆

Overview: OneWater Marine operates as a recreational boat retailer and distributor with a market cap of approximately $0.47 billion.

Operations: The company generates revenue primarily from its dealerships and distribution segments, with recent figures showing $1.62 billion from dealerships and $156.06 million from distribution. The gross profit margin has shown variability, reaching a high of 31.75% in June 2022 before declining to 24.71% by December 2024. Operating expenses, including significant general and administrative costs, impact overall profitability, contributing to the negative net income observed in recent periods despite substantial revenues.

PE: -50.5x

OneWater Marine, a small-cap company in the U.S., recently reported a reduced net loss of US$5.71 million for the year ended September 2024, down from US$38.59 million previously, indicating potential financial improvement despite revenue dipping to US$1.77 billion from US$1.94 billion. Insider confidence is evident with recent share purchases in November 2024, suggesting belief in future growth prospects amid revised credit agreements and cautious optimism for fiscal 2025 revenue between US$1.7 billion and US$1.85 billion amidst external challenges like hurricanes impacting early performance.

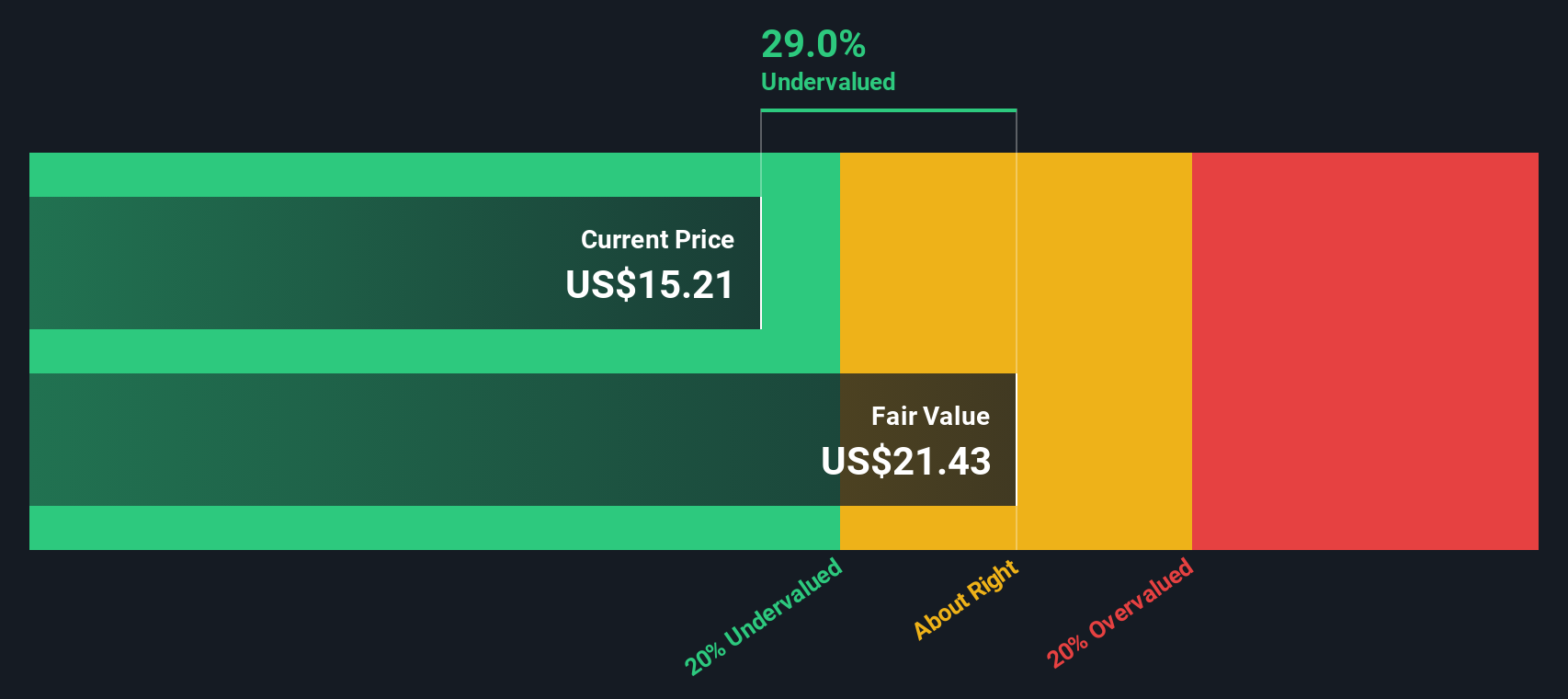

CPI Card Group (NasdaqGM:PMTS)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: CPI Card Group is a company specializing in the production and provision of payment card solutions, including prepaid debit and credit cards, with a market capitalization of approximately $0.36 billion.

Operations: The company generates revenue primarily from its Debit and Credit segment, contributing $365.45 million, and the Prepaid Debit segment with $94.14 million. The gross profit margin has shown fluctuations over time, reaching 38.21% in September 2024. Operating expenses are a significant component of costs, with General & Administrative Expenses being a major part of it at $101.46 million as of September 2024.

PE: 23.5x

CPI Card Group, a smaller U.S. company, has shown insider confidence with recent share purchases, reflecting potential belief in its prospects. The firm reported Q3 2024 revenue of US$124.75 million but saw decreased net income at US$1.29 million from the previous year. Despite this, it raised its earnings guidance for 2024 to mid-to-high single-digit growth and completed a repurchase of 486,464 shares for US$8.85 million by September end, signaling strategic financial maneuvers amidst challenging profit margins and higher-risk funding reliance.

- Click to explore a detailed breakdown of our findings in CPI Card Group's valuation report.

Explore historical data to track CPI Card Group's performance over time in our Past section.

Maravai LifeSciences Holdings (NasdaqGS:MRVI)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Maravai LifeSciences Holdings focuses on providing specialized products for nucleic acid production and biologics safety testing, with a market cap of approximately $2.20 billion.

Operations: Nucleic Acid Production and Biologics Safety Testing are the primary revenue streams. The company's gross profit margin showed a notable trend, peaking at 83.35% in Q1 2022 before declining to 46.36% by Q4 2024. Operating expenses have consistently been a significant component of the cost structure, with General & Administrative Expenses being substantial throughout the periods analyzed.

PE: -3.5x

Maravai LifeSciences Holdings, a company with a volatile share price over the past three months, faces challenges with its external borrowing as the sole funding source. Recent leadership changes saw R. Andrew Eckert take over as Chairman from founder Carl Hull, potentially steering new strategic directions. Despite reporting a net loss of US$99 million for Q3 2024 and facing goodwill impairment charges of US$154 million, insider confidence remains noteworthy through recent share purchases by key individuals.

- Take a closer look at Maravai LifeSciences Holdings' potential here in our valuation report.

Learn about Maravai LifeSciences Holdings' historical performance.

Next Steps

- Get an in-depth perspective on all 47 Undervalued US Small Caps With Insider Buying by using our screener here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:PMTS

CPI Card Group

Engages in the design, production, data personalization, packaging, and fulfillment of payment cards in the United States.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|21.0% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.7% undervalued

RO

Community Contributor