- United States

- /

- Consumer Finance

- /

- NasdaqGS:CACC

Credit Acceptance Corporation's (NASDAQ:CACC) CEO Compensation Looks Acceptable To Us And Here's Why

Key Insights

- Credit Acceptance will host its Annual General Meeting on 5th of June

- Salary of US$1.00m is part of CEO Ken Booth's total remuneration

- The overall pay is 92% below the industry average

- Credit Acceptance's EPS declined by 20% over the past three years while total shareholder return over the past three years was 4.0%

Performance at Credit Acceptance Corporation (NASDAQ:CACC) has been rather uninspiring recently and shareholders may be wondering how CEO Ken Booth plans to fix this. One way they can exercise their influence on management is through voting on resolutions, such as executive remuneration at the next AGM, coming up on 5th of June. Voting on executive pay could be a powerful way to influence management, as studies have shown that the right compensation incentives impact company performance. We think CEO compensation looks appropriate given the data we have put together.

See our latest analysis for Credit Acceptance

Comparing Credit Acceptance Corporation's CEO Compensation With The Industry

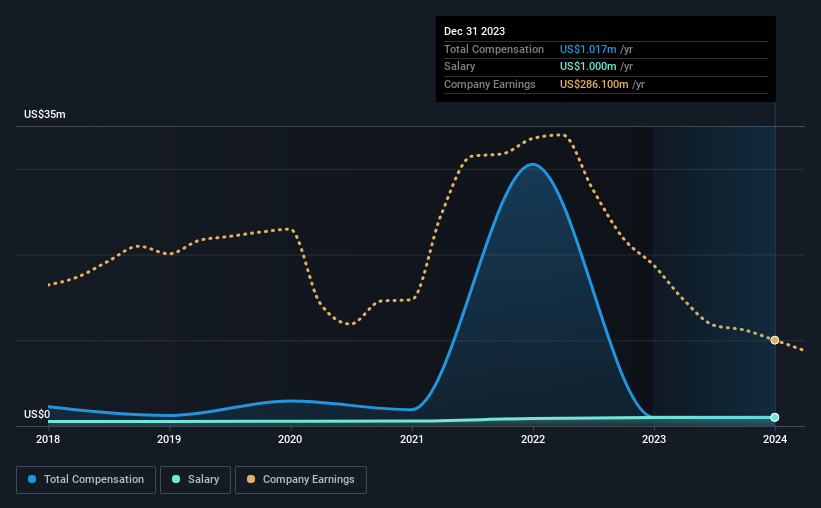

At the time of writing, our data shows that Credit Acceptance Corporation has a market capitalization of US$5.9b, and reported total annual CEO compensation of US$1.0m for the year to December 2023. That is, the compensation was roughly the same as last year. In particular, the salary of US$1.00m, makes up a huge portion of the total compensation being paid to the CEO.

On comparing similar companies from the American Consumer Finance industry with market caps ranging from US$4.0b to US$12b, we found that the median CEO total compensation was US$12m. Accordingly, Credit Acceptance pays its CEO under the industry median. Moreover, Ken Booth also holds US$63m worth of Credit Acceptance stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$1.0m | US$1.0m | 98% |

| Other | US$17k | US$15k | 2% |

| Total Compensation | US$1.0m | US$1.0m | 100% |

Talking in terms of the industry, salary represented approximately 17% of total compensation out of all the companies we analyzed, while other remuneration made up 83% of the pie. Credit Acceptance has gone down a largely traditional route, paying Ken Booth a high salary, giving it preference over non-salary benefits. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at Credit Acceptance Corporation's Growth Numbers

Over the last three years, Credit Acceptance Corporation has shrunk its earnings per share by 20% per year. It saw its revenue drop 17% over the last year.

The decline in EPS is a bit concerning. And the fact that revenue is down year on year arguably paints an ugly picture. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Credit Acceptance Corporation Been A Good Investment?

Credit Acceptance Corporation has generated a total shareholder return of 4.0% over three years, so most shareholders wouldn't be too disappointed. Although, there's always room to improve. As a result, investors in the company might be reluctant about agreeing to increase CEO pay in the future, before seeing an improvement on their returns.

To Conclude...

Credit Acceptance pays its CEO a majority of compensation through a salary. Despite the positive returns on shareholders' investments, the fact that earnings have failed to grow makes us skeptical about the stock keeping up its current momentum. These concerns could be addressed to the board and shareholders should revisit their investment thesis to see if it still makes sense.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. That's why we did some digging and identified 1 warning sign for Credit Acceptance that investors should think about before committing capital to this stock.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:CACC

Credit Acceptance

Engages in the provision of financing programs, and related products and services in the United States.

Exceptional growth potential with imperfect balance sheet.

Similar Companies

Market Insights

Community Narratives