Advertisement

- United States

- /

- Software

- /

- NYSE:ESTC

March 2025's Noteworthy Stocks Estimated Below Intrinsic Value

Simply Wall St

Reviewed by Simply Wall St

As February 2025 comes to a close, the U.S. stock market has experienced a mixed performance with major indexes posting losses for the month despite a late surge fueled by easing inflation concerns. Amidst this volatile environment, identifying stocks that are potentially undervalued can offer opportunities for investors seeking value; such stocks might be trading below their intrinsic value due to market fluctuations or broader economic uncertainties.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| MINISO Group Holding (NYSE:MNSO) | $20.81 | $41.03 | 49.3% |

| Atour Lifestyle Holdings (NasdaqGS:ATAT) | $30.71 | $59.36 | 48.3% |

| Lantheus Holdings (NasdaqGM:LNTH) | $93.82 | $182.42 | 48.6% |

| Limbach Holdings (NasdaqCM:LMB) | $83.00 | $160.52 | 48.3% |

| Cadre Holdings (NYSE:CDRE) | $33.62 | $64.89 | 48.2% |

| JBT Marel (NYSE:JBTM) | $132.00 | $262.89 | 49.8% |

| Albemarle (NYSE:ALB) | $77.03 | $151.13 | 49% |

| Fluence Energy (NasdaqGS:FLNC) | $5.72 | $11.42 | 49.9% |

| Workiva (NYSE:WK) | $87.52 | $170.87 | 48.8% |

| Driven Brands Holdings (NasdaqGS:DRVN) | $17.53 | $34.71 | 49.5% |

Let's take a closer look at a couple of our picks from the screened companies.

DoorDash (NasdaqGS:DASH)

Overview: DoorDash, Inc. operates a commerce platform that links merchants, consumers, and independent contractors both in the United States and internationally, with a market cap of approximately $83.36 billion.

Operations: The company's revenue segment is Internet Information Providers, generating $10.72 billion.

Estimated Discount To Fair Value: 40.5%

DoorDash's recent financial performance shows a transition to profitability with a net income of US$123 million in 2024, contrasting with the previous year's loss. The company is trading significantly below its estimated fair value of US$333.73, suggesting potential undervaluation based on cash flows. Despite large one-off items affecting results and insider selling, DoorDash's revenue growth outpaces the broader market, supported by strategic partnerships like those with The Home Depot and Ibotta.

- Our earnings growth report unveils the potential for significant increases in DoorDash's future results.

- Dive into the specifics of DoorDash here with our thorough financial health report.

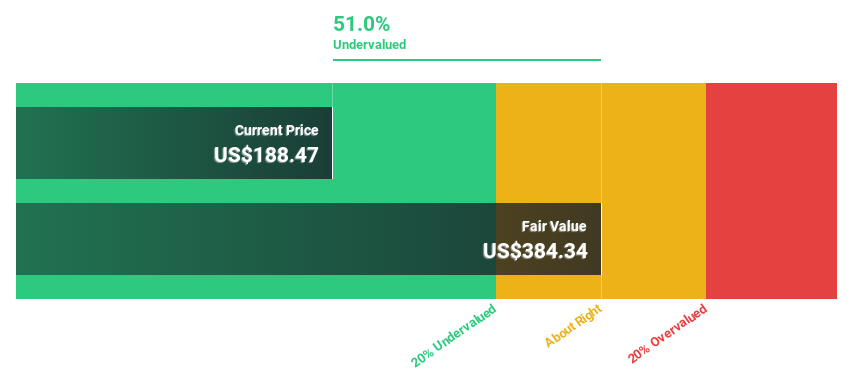

Carvana (NYSE:CVNA)

Overview: Carvana Co. operates an e-commerce platform for buying and selling used cars in the United States, with a market cap of $50.25 billion.

Operations: The company generates revenue primarily from its retail segment, specifically in the gasoline and auto dealers category, amounting to $13.67 billion.

Estimated Discount To Fair Value: 40.8%

Carvana's recent earnings report highlights a shift from a net loss to a net income of US$79 million in Q4 2024, with revenue climbing to US$3.55 billion from US$2.42 billion year-on-year. Trading at 40.8% below its estimated fair value of US$393.87, Carvana appears undervalued based on cash flows despite insider selling and interest coverage concerns. Revenue growth is projected at 17.9% annually, surpassing the broader market's pace, while earnings are expected to grow significantly over the next three years.

- The growth report we've compiled suggests that Carvana's future prospects could be on the up.

- Take a closer look at Carvana's balance sheet health here in our report.

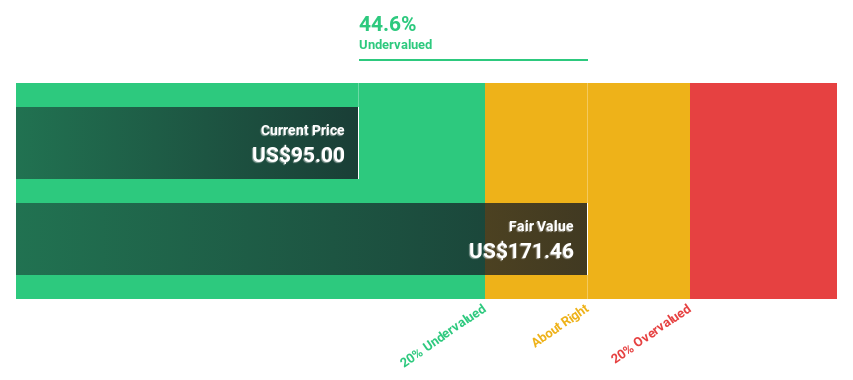

Elastic (NYSE:ESTC)

Overview: Elastic N.V. is a search AI company offering hosted and managed solutions for hybrid, public, private, and multi-cloud environments globally, with a market cap of approximately $12.15 billion.

Operations: The company's revenue segment is primarily derived from Software & Programming, accounting for $1.43 billion.

Estimated Discount To Fair Value: 33.3%

Elastic's recent earnings report shows a net loss of US$17.06 million for Q3 2025, despite revenue growth to US$382.08 million from US$327.96 million year-on-year. The stock trades at 33.3% below its estimated fair value of US$174.42, suggesting potential undervaluation based on discounted cash flow analysis, although insider selling raises concerns. Elastic's forecasted annual profit growth is robust, and revenue is expected to grow faster than the overall U.S. market rate over the next three years.

- The analysis detailed in our Elastic growth report hints at robust future financial performance.

- Click here and access our complete balance sheet health report to understand the dynamics of Elastic.

Turning Ideas Into Actions

- Gain an insight into the universe of 199 Undervalued US Stocks Based On Cash Flows by clicking here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Elastic might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ESTC

Elastic

A search artificial intelligence (AI) company, provides software platforms to run in hybrid, public or private clouds, and multi-cloud environments in the United States and internationally.

Undervalued with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|32.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|45.4% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$174.00|37.0% undervalued

AG

Community Contributor