Advertisement

- United States

- /

- Specialty Stores

- /

- NYSE:WSM

Williams-Sonoma, Inc.'s (NYSE:WSM) CEO Compensation Is Looking A Bit Stretched At The Moment

Key Insights

- Williams-Sonoma will host its Annual General Meeting on 29th of May

- CEO Laura Alber's total compensation includes salary of US$1.60m

- The overall pay is 71% above the industry average

- Williams-Sonoma's total shareholder return over the past three years was 74% while its EPS grew by 19% over the past three years

CEO Laura Alber has done a decent job of delivering relatively good performance at Williams-Sonoma, Inc. (NYSE:WSM) recently. As shareholders go into the upcoming AGM on 29th of May, CEO compensation will probably not be their focus, but rather the steps management will take to continue the growth momentum. However, some shareholders may still be hesitant of being overly generous with CEO compensation.

See our latest analysis for Williams-Sonoma

How Does Total Compensation For Laura Alber Compare With Other Companies In The Industry?

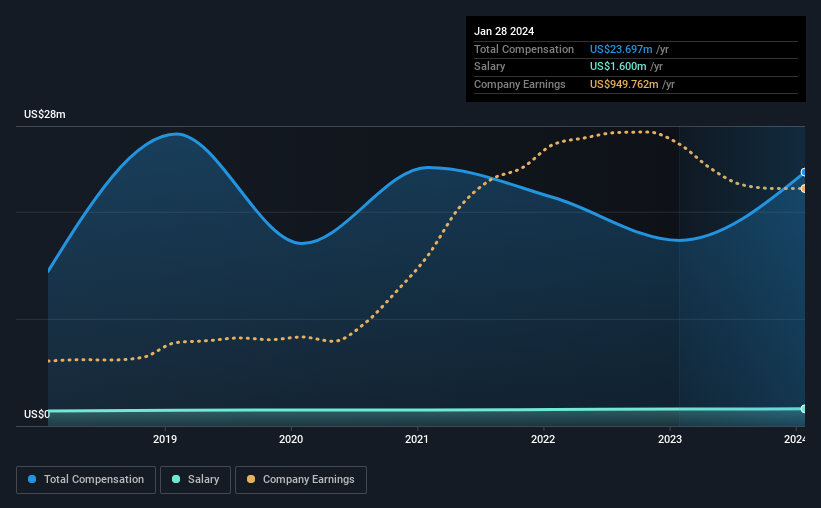

Our data indicates that Williams-Sonoma, Inc. has a market capitalization of US$20b, and total annual CEO compensation was reported as US$24m for the year to January 2024. We note that's an increase of 37% above last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at US$1.6m.

On comparing similar companies in the American Specialty Retail industry with market capitalizations above US$8.0b, we found that the median total CEO compensation was US$14m. Hence, we can conclude that Laura Alber is remunerated higher than the industry median. Furthermore, Laura Alber directly owns US$160m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2024 | 2023 | Proportion (2024) |

| Salary | US$1.6m | US$1.6m | 7% |

| Other | US$22m | US$16m | 93% |

| Total Compensation | US$24m | US$17m | 100% |

Speaking on an industry level, nearly 17% of total compensation represents salary, while the remainder of 83% is other remuneration. It's interesting to note that Williams-Sonoma allocates a smaller portion of compensation to salary in comparison to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

A Look at Williams-Sonoma, Inc.'s Growth Numbers

Williams-Sonoma, Inc. has seen its earnings per share (EPS) increase by 19% a year over the past three years. Its revenue is down 11% over the previous year.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. The lack of revenue growth isn't ideal, but it is the bottom line that counts most in business. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Williams-Sonoma, Inc. Been A Good Investment?

Most shareholders would probably be pleased with Williams-Sonoma, Inc. for providing a total return of 74% over three years. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

In Summary...

Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. Still, not all shareholders might be in favor of a pay raise to the CEO, seeing that they are already being paid higher than the industry.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. That's why we did some digging and identified 1 warning sign for Williams-Sonoma that you should be aware of before investing.

Switching gears from Williams-Sonoma, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

Valuation is complex, but we're here to simplify it.

Discover if Williams-Sonoma might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:WSM

Williams-Sonoma

Operates as an omni-channel specialty retailer of various products for home.

Outstanding track record with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

SSAB in pole position when it comes to the combination of steel tariffs and the EU's investment drive

Fair Value SEK 98.20|46.5% undervalued

PI

Community Contributor

The Future of Lennar and Homebuilding Faces Short Term Challenges with Potential for Long Term Growth

Fair Value US$162.49|34.1% undervalued

ZE

Community Contributor

Saudi Aramco (SASE:2222): Not The Sexiest High Dividend Yield Stock, But One With Interesting 'Convertible-Like' Qualities

Fair Value ر.س37.02|31.1% undervalued

EV

Community Contributor