Advertisement

- United States

- /

- Hospitality

- /

- NasdaqGS:HTHT

3 High Growth Companies Insiders Are Betting On

Simply Wall St

Reviewed by Simply Wall St

As the U.S. stock market shows signs of stabilizing with the S&P 500 and Nasdaq attempting to break their recent losing streaks, investors are keenly observing companies that demonstrate resilience and potential for growth amid economic uncertainties. In this environment, stocks with high insider ownership often attract attention, as they suggest a strong alignment between company leadership and shareholder interests, potentially indicating confidence in future performance.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Atour Lifestyle Holdings (NasdaqGS:ATAT) | 26% | 25.7% |

| Duolingo (NasdaqGS:DUOL) | 14.4% | 37.1% |

| Hims & Hers Health (NYSE:HIMS) | 13.2% | 21.8% |

| Corcept Therapeutics (NasdaqCM:CORT) | 11.7% | 36.7% |

| Coastal Financial (NasdaqGS:CCB) | 14.5% | 46.3% |

| Astera Labs (NasdaqGS:ALAB) | 15.9% | 61.3% |

| BBB Foods (NYSE:TBBB) | 16.2% | 41.1% |

| Clene (NasdaqCM:CLNN) | 20.7% | 59.1% |

| Upstart Holdings (NasdaqGS:UPST) | 12.7% | 100.1% |

| Credit Acceptance (NasdaqGS:CACC) | 14.4% | 33.6% |

Here's a peek at a few of the choices from the screener.

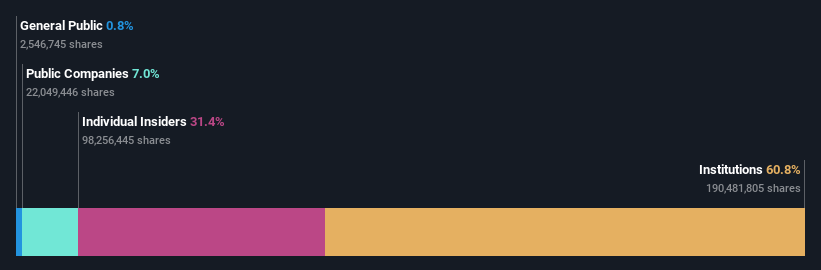

H World Group (NasdaqGS:HTHT)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: H World Group Limited operates leased and owned, manachised, and franchised hotels in the People’s Republic of China with a market cap of approximately $11.92 billion.

Operations: The company's revenue segments include leased and owned hotels, manachised hotels, and franchised hotels in the People’s Republic of China.

Insider Ownership: 31.4%

Earnings Growth Forecast: 21.1% p.a.

H World Group shows potential as a growth company with high insider ownership, despite recent challenges. The company's net income declined to CNY 49 million in Q4 2024 from CNY 743 million a year ago, yet it continues expanding its hotel network significantly. Revenue for the full year increased to CNY 23.89 billion, supported by strong manachised and franchised operations. Earnings are expected to grow significantly at an annual rate of 21.1%, outpacing the US market average.

- Dive into the specifics of H World Group here with our thorough growth forecast report.

- Our valuation report unveils the possibility H World Group's shares may be trading at a premium.

Krystal Biotech (NasdaqGS:KRYS)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Krystal Biotech, Inc. is a commercial-stage biotechnology company focused on discovering, developing, manufacturing, and commercializing genetic medicines for diseases with high unmet medical needs in the United States, with a market cap of approximately $5.45 billion.

Operations: Krystal Biotech generates revenue primarily from its business of developing and commercializing pharmaceuticals, amounting to $290.52 million.

Insider Ownership: 10.4%

Earnings Growth Forecast: 31.8% p.a.

Krystal Biotech demonstrates strong growth potential, with earnings expected to increase by 31.8% annually, surpassing the US market average. Recent Q4 2024 results showed net income rising to US$45.48 million from US$8.69 million a year ago, despite large one-off items impacting financials. The company received positive EMA recommendations for its VYJUVEK® product, enhancing its market position in Europe and supporting revenue growth forecasts of 25.7% annually over the next three years.

- Delve into the full analysis future growth report here for a deeper understanding of Krystal Biotech.

- According our valuation report, there's an indication that Krystal Biotech's share price might be on the expensive side.

RH (NYSE:RH)

Simply Wall St Growth Rating: ★★★★★☆

Overview: RH, along with its subsidiaries, operates as a retailer in the home furnishings market and has a market cap of approximately $4.28 billion.

Operations: The company's revenue is primarily derived from its Restoration Hardware (RH) segment, generating $2.92 billion, with an additional contribution of $191.13 million from Waterworks.

Insider Ownership: 17.3%

Earnings Growth Forecast: 53.8% p.a.

RH's growth potential is underscored by its high expected earnings growth of 53.8% per year, significantly outpacing the US market average. However, insider activity shows substantial selling in the past three months, raising concerns despite a forecasted high return on equity of 79.2%. The company's revenue is projected to grow at 11.4% annually, faster than the broader market but below the threshold for rapid expansion. RH trades at a discount to fair value estimates yet faces challenges with profit margins and interest coverage.

- Navigate through the intricacies of RH with our comprehensive analyst estimates report here.

- Our valuation report here indicates RH may be overvalued.

Make It Happen

- Access the full spectrum of 205 Fast Growing US Companies With High Insider Ownership by clicking on this link.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if H World Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:HTHT

H World Group

Develops leased and owned, manachised, and franchised hotels in the People’s Republic of China.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor