Advertisement

- United States

- /

- Real Estate

- /

- NYSE:CWK

3 US Stocks Estimated To Be Up To 35.4% Below Intrinsic Value

Simply Wall St

Reviewed by Simply Wall St

As major U.S. stock indexes are set to open sharply higher following the recent election results, investors are keenly observing market movements and potential opportunities. In this environment, identifying undervalued stocks can be a strategic approach, as these equities may offer significant upside potential when their intrinsic value is recognized by the market.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| First National (NasdaqCM:FXNC) | $21.37 | $42.26 | 49.4% |

| Western Alliance Bancorporation (NYSE:WAL) | $84.63 | $168.45 | 49.8% |

| Coupang (NYSE:CPNG) | $26.89 | $53.38 | 49.6% |

| Bank of Marin Bancorp (NasdaqCM:BMRC) | $22.49 | $44.47 | 49.4% |

| Range Resources (NYSE:RRC) | $30.78 | $60.26 | 48.9% |

| HealthEquity (NasdaqGS:HQY) | $89.23 | $175.93 | 49.3% |

| Alaska Air Group (NYSE:ALK) | $48.56 | $96.53 | 49.7% |

| WEX (NYSE:WEX) | $173.51 | $341.87 | 49.2% |

| Freshpet (NasdaqGM:FRPT) | $151.59 | $297.18 | 49% |

| Cytek Biosciences (NasdaqGS:CTKB) | $5.44 | $10.66 | 49% |

Here we highlight a subset of our preferred stocks from the screener.

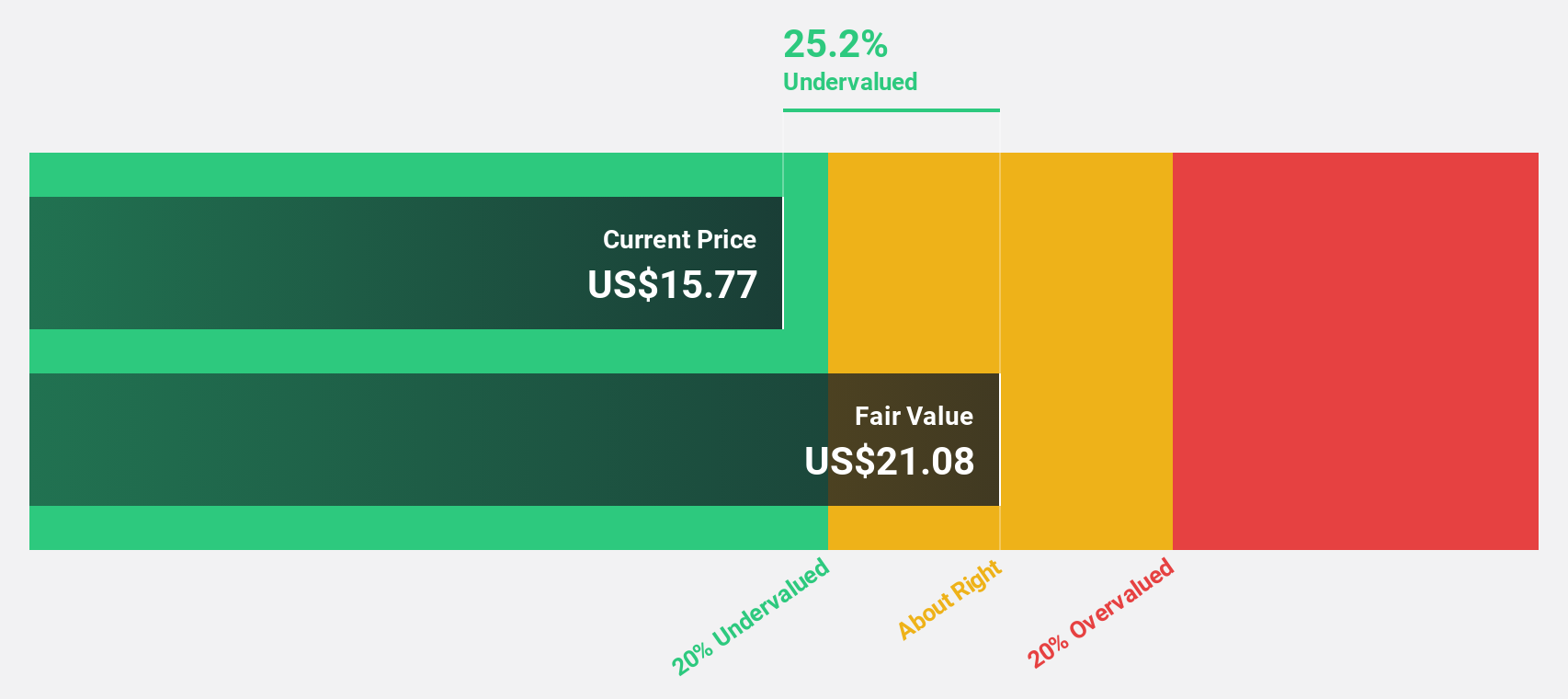

Bilibili (NasdaqGS:BILI)

Overview: Bilibili Inc. offers online entertainment services targeting young generations in the People’s Republic of China, with a market cap of $9.14 billion.

Operations: The company generates revenue of CN¥23.95 billion from its Internet Information Providers segment, focusing on online entertainment services for young audiences in China.

Estimated Discount To Fair Value: 35.4%

Bilibili is trading at US$23.22, below its estimated fair value of US$35.93, indicating potential undervaluation based on discounted cash flows. Despite a volatile share price recently, the company reported significant revenue growth in 2024 and reduced net losses compared to the previous year. Forecasts suggest Bilibili will achieve profitability within three years with earnings expected to grow rapidly at 79.53% annually, outpacing average market growth rates in the United States.

- Our comprehensive growth report raises the possibility that Bilibili is poised for substantial financial growth.

- Navigate through the intricacies of Bilibili with our comprehensive financial health report here.

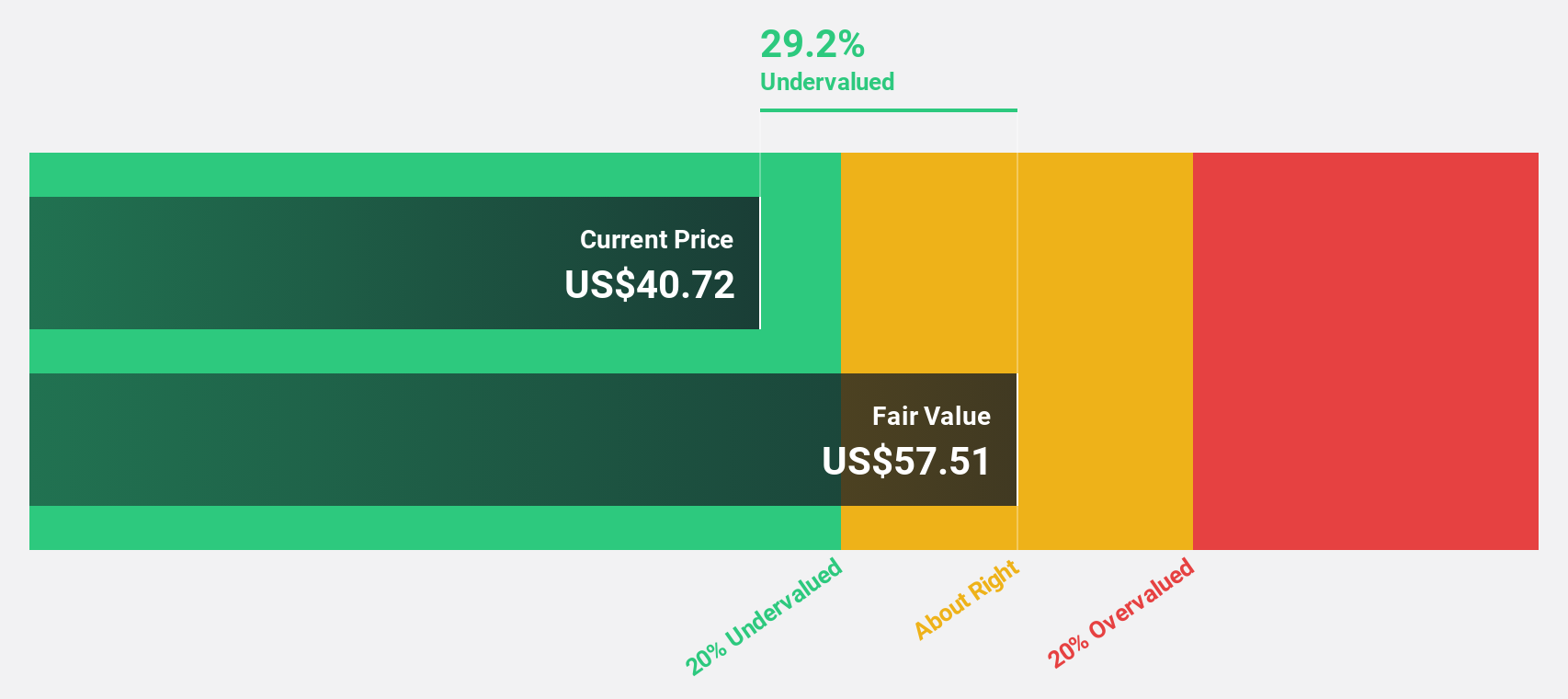

ExlService Holdings (NasdaqGS:EXLS)

Overview: ExlService Holdings, Inc. is a company that provides data analytics and digital operations solutions both in the United States and internationally, with a market cap of approximately $6.78 billion.

Operations: The company's revenue segments include Analytics ($770.51 million), Insurance ($591.10 million), Healthcare ($110.80 million), and Emerging Business ($298.59 million).

Estimated Discount To Fair Value: 28.1%

ExlService Holdings is trading at US$43.08, below its fair value estimate of US$59.90, highlighting an undervaluation based on cash flows. The company's revenue and earnings are growing faster than the U.S. market averages, with a forecasted earnings growth rate of 15.3% annually. Recent strategic moves include seeking acquisitions and launching a new AI platform to enhance client solutions, reflecting robust capital allocation strategies despite some insider selling activity recently observed.

- In light of our recent growth report, it seems possible that ExlService Holdings' financial performance will exceed current levels.

- Take a closer look at ExlService Holdings' balance sheet health here in our report.

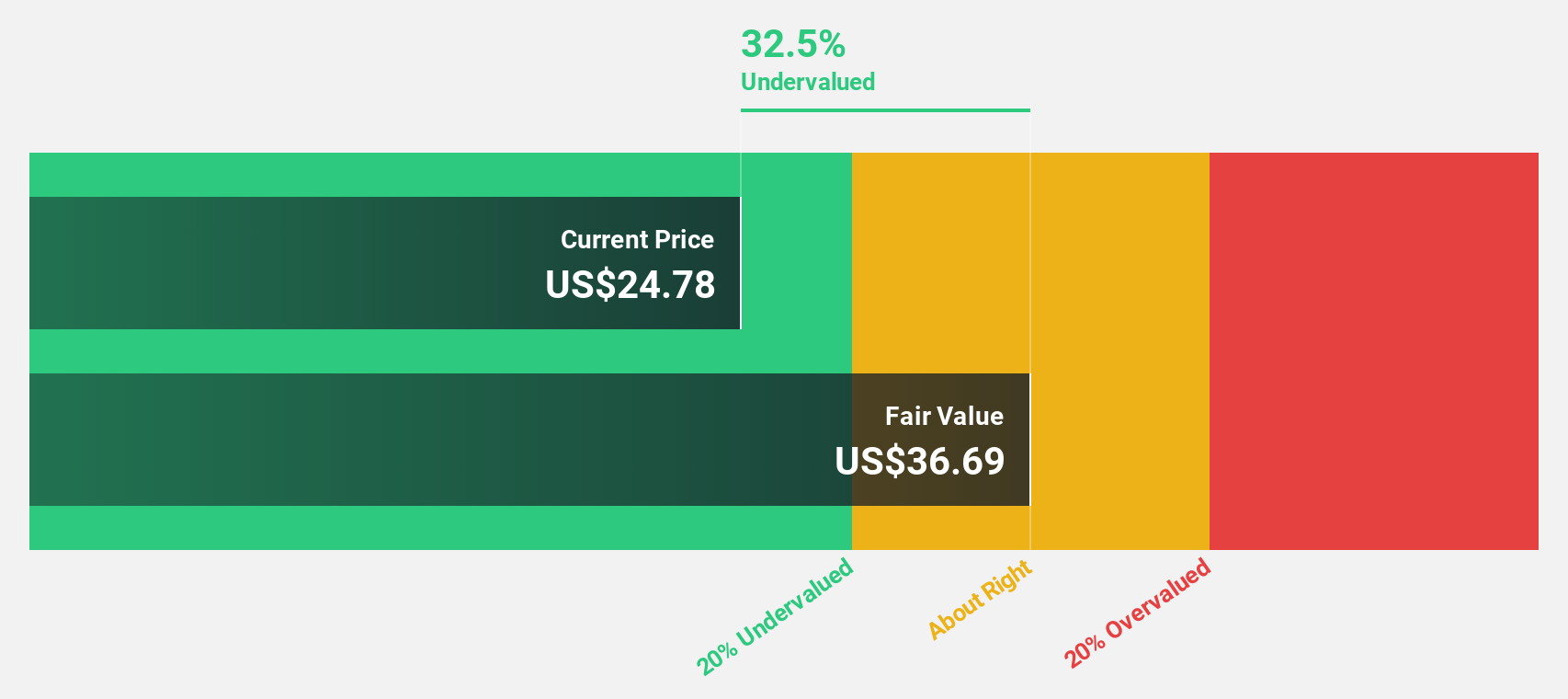

Cushman & Wakefield (NYSE:CWK)

Overview: Cushman & Wakefield plc, along with its subsidiaries, offers commercial real estate services globally under the Cushman & Wakefield brand and has a market cap of approximately $3.01 billion.

Operations: Cushman & Wakefield generates revenue through its commercial real estate services in the United States, Australia, the United Kingdom, and other international markets.

Estimated Discount To Fair Value: 12.1%

Cushman & Wakefield trades at US$15.17, below its fair value of US$17.26, suggesting undervaluation based on cash flows. The company became profitable this year with earnings expected to grow significantly, outpacing the U.S. market average. Recent financial results show improved net income and strategic debt management through repricing and prepayment efforts, enhancing financial stability despite interest coverage challenges and large one-off items affecting earnings quality.

- Our earnings growth report unveils the potential for significant increases in Cushman & Wakefield's future results.

- Get an in-depth perspective on Cushman & Wakefield's balance sheet by reading our health report here.

Taking Advantage

- Embark on your investment journey to our 203 Undervalued US Stocks Based On Cash Flows selection here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CWK

Cushman & Wakefield

Provides commercial real estate services under the Cushman & Wakefield brand in the Americas, Europe, Middle East, Africa, and Asia Pacific.

Undervalued with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor