Advertisement

- United States

- /

- Banks

- /

- NYSE:FBK

FB Financial Corporation Just Beat Analyst Forecasts, And Analysts Have Been Updating Their Predictions

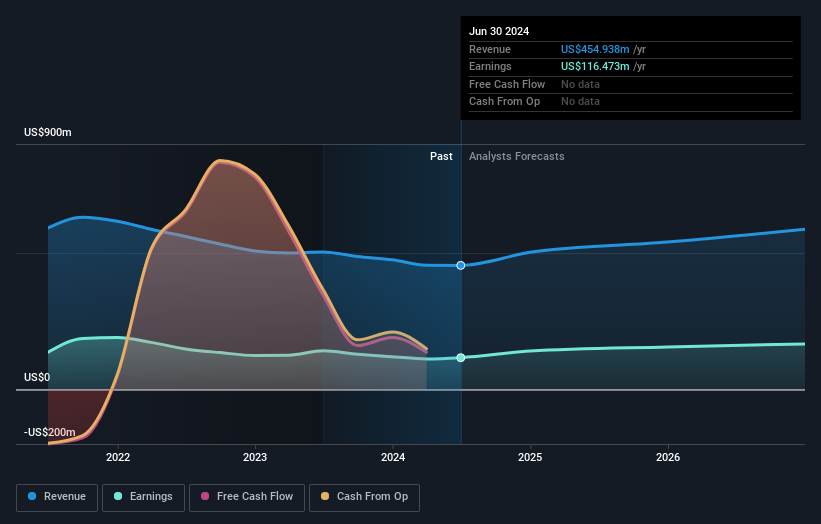

As you might know, FB Financial Corporation (NYSE:FBK) just kicked off its latest second-quarter results with some very strong numbers. FB Financial beat earnings, with revenues hitting US$128m, ahead of expectations, and statutory earnings per share outperforming analyst reckonings by a solid 13%. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

View our latest analysis for FB Financial

Taking into account the latest results, the current consensus from FB Financial's seven analysts is for revenues of US$502.9m in 2024. This would reflect a decent 11% increase on its revenue over the past 12 months. Per-share earnings are expected to surge 20% to US$3.00. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$492.9m and earnings per share (EPS) of US$2.87 in 2024. It looks like there's been a modest increase in sentiment following the latest results, withthe analysts becoming a bit more optimistic in their predictions for both revenues and earnings.

With these upgrades, we're not surprised to see that the analysts have lifted their price target 13% to US$47.08per share. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic FB Financial analyst has a price target of US$52.50 per share, while the most pessimistic values it at US$43.00. Even so, with a relatively close grouping of estimates, it looks like the analysts are quite confident in their valuations, suggesting FB Financial is an easy business to forecast or the the analysts are all using similar assumptions.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the FB Financial's past performance and to peers in the same industry. The analysts are definitely expecting FB Financial's growth to accelerate, with the forecast 22% annualised growth to the end of 2024 ranking favourably alongside historical growth of 6.2% per annum over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 5.6% per year. Factoring in the forecast acceleration in revenue, it's pretty clear that FB Financial is expected to grow much faster than its industry.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around FB Financial's earnings potential next year. Pleasantly, they also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow faster than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple FB Financial analysts - going out to 2026, and you can see them free on our platform here.

That said, it's still necessary to consider the ever-present spectre of investment risk. We've identified 1 warning sign with FB Financial , and understanding this should be part of your investment process.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:FBK

FB Financial

Operates as a bank holding company for FirstBank that provides a suite of commercial and consumer banking services.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.3% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor