Advertisement

- United Kingdom

- /

- Consumer Finance

- /

- LSE:SUS

3 UK Stocks That Could Be Trading Below Estimated Value

Simply Wall St

Reviewed by Simply Wall St

The United Kingdom market has experienced a flat performance over the last week, yet it has achieved a 7.5% rise over the past year, with earnings anticipated to grow by 14% annually in the coming years. In this context, identifying stocks that are potentially trading below their estimated value can be an attractive opportunity for investors seeking to capitalize on future growth prospects while navigating current market conditions.

Top 10 Undervalued Stocks Based On Cash Flows In The United Kingdom

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| GlobalData (AIM:DATA) | £1.985 | £3.72 | 46.6% |

| S&U (LSE:SUS) | £18.45 | £36.65 | 49.7% |

| Marks Electrical Group (AIM:MRK) | £0.62 | £1.22 | 49.3% |

| Informa (LSE:INF) | £8.248 | £16.14 | 48.9% |

| Redcentric (AIM:RCN) | £1.2375 | £2.41 | 48.6% |

| Mpac Group (AIM:MPAC) | £4.525 | £8.99 | 49.7% |

| BATM Advanced Communications (LSE:BVC) | £0.19075 | £0.37 | 48.3% |

| Foxtons Group (LSE:FOXT) | £0.646 | £1.20 | 46.4% |

| SysGroup (AIM:SYS) | £0.325 | £0.65 | 50% |

| Genel Energy (LSE:GENL) | £0.775 | £1.50 | 48.4% |

We'll examine a selection from our screener results.

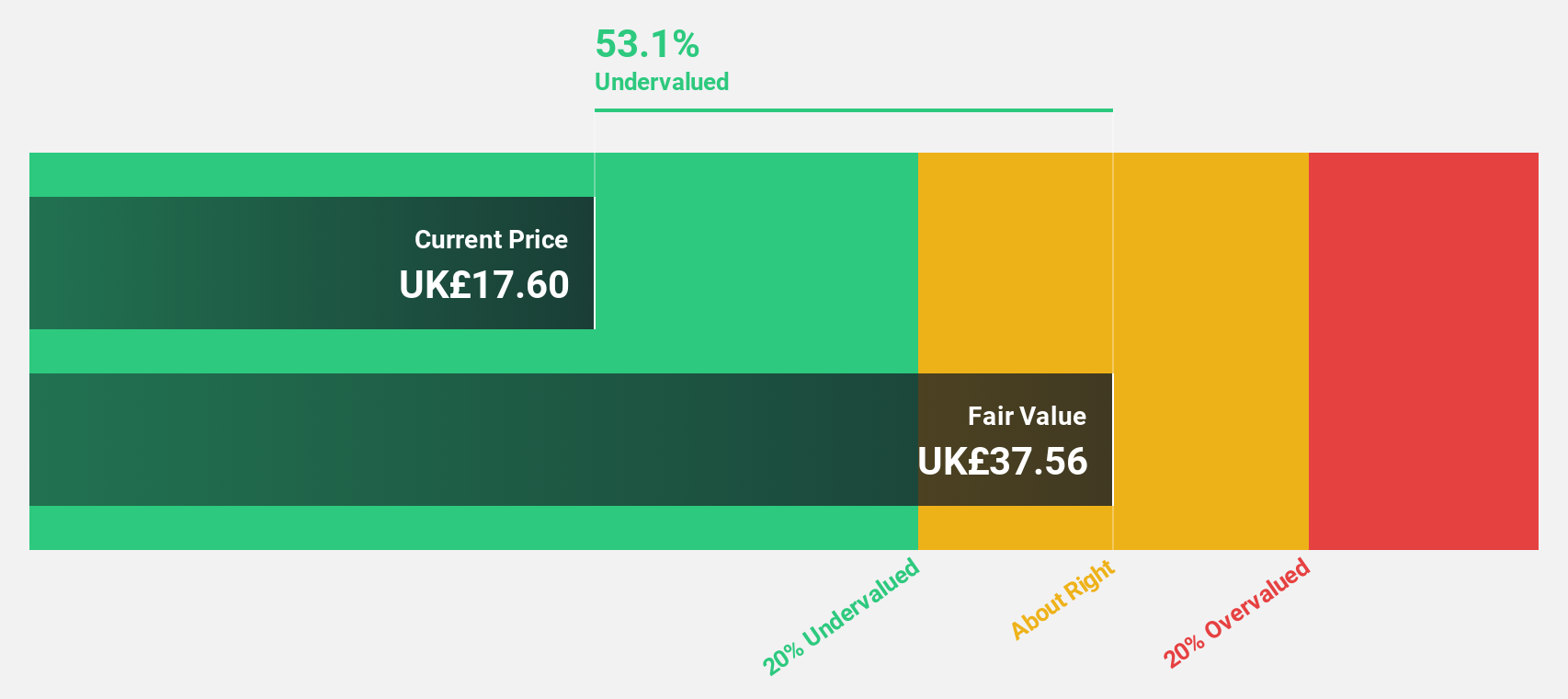

ConvaTec Group (LSE:CTEC)

Overview: ConvaTec Group PLC develops, manufactures, and sells medical products, services, and technologies across Europe, North America, and internationally with a market cap of £4.64 billion.

Operations: The company's revenue segment focuses on the development, manufacture, and sale of medical products and technologies, generating $2.20 billion.

Estimated Discount To Fair Value: 41.7%

ConvaTec Group appears undervalued based on cash flows, trading at £2.27 while estimated fair value stands at £3.89, suggesting a significant discount. Analysts forecast earnings growth of 21% annually, outpacing the UK market's 14%. Despite high debt levels and modest revenue growth projections of 5.8%, recent results show improved profitability with net income rising to US$78.6 million for H1 2024 from US$55.7 million last year, supporting its undervaluation thesis.

- Our expertly prepared growth report on ConvaTec Group implies its future financial outlook may be stronger than recent results.

- Click here to discover the nuances of ConvaTec Group with our detailed financial health report.

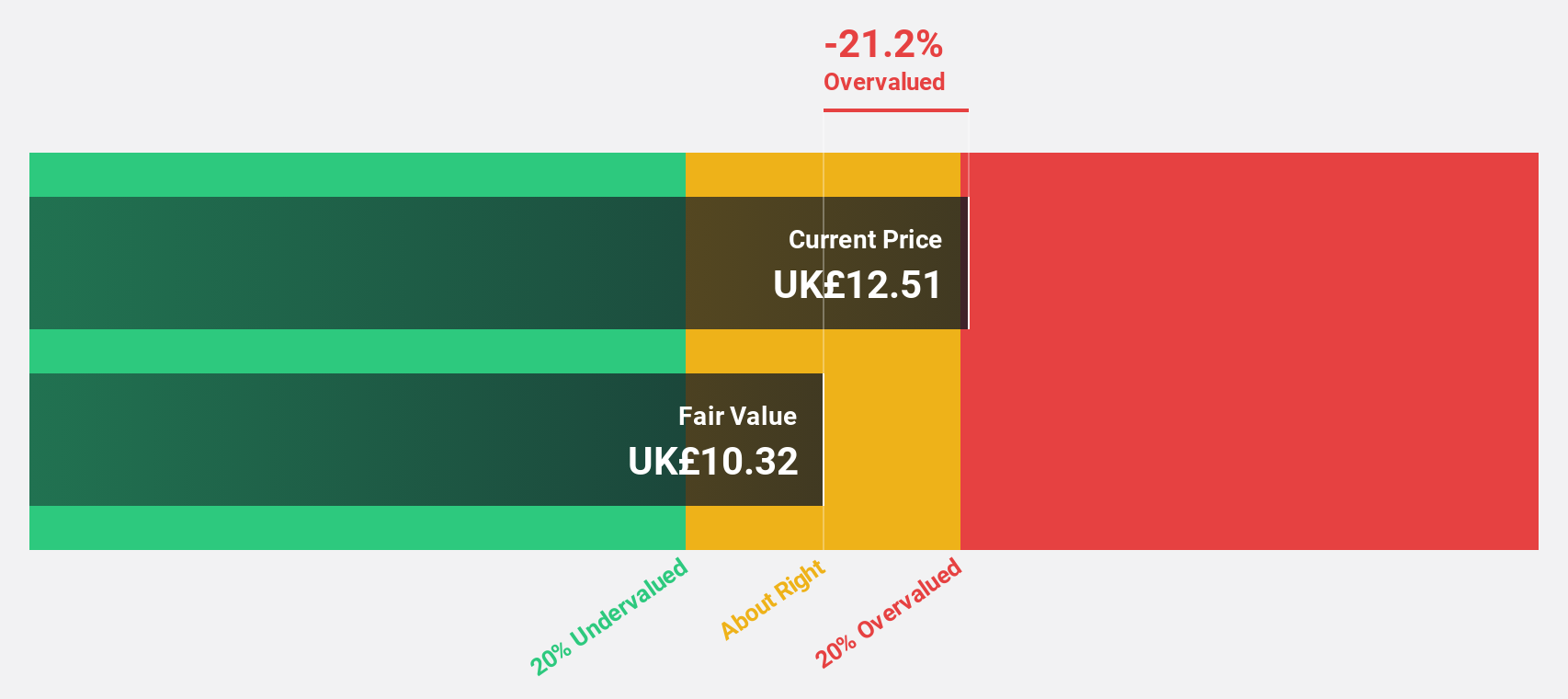

Sage Group (LSE:SGE)

Overview: The Sage Group plc, along with its subsidiaries, offers technology solutions and services for small and medium businesses across the United States, the United Kingdom, France, and internationally, with a market cap of £10.22 billion.

Operations: Revenue segments are distributed as follows: Europe generates £595 million, North America contributes £1.01 billion, and the United Kingdom & Ireland accounts for £488 million.

Estimated Discount To Fair Value: 21.4%

Sage Group is trading at £10.26, below its estimated fair value of £13.05, highlighting potential undervaluation based on cash flows. Revenue growth is forecasted at 7.7% annually, surpassing the UK market's 3.5%, while earnings are expected to grow by 15.1%. Despite high debt levels and recent insider selling, Sage's strategic partnership with VoPay enhances its business cloud offerings, supporting revenue growth and operational efficiency amidst a backdrop of consistent financial performance improvements.

- Our growth report here indicates Sage Group may be poised for an improving outlook.

- Delve into the full analysis health report here for a deeper understanding of Sage Group.

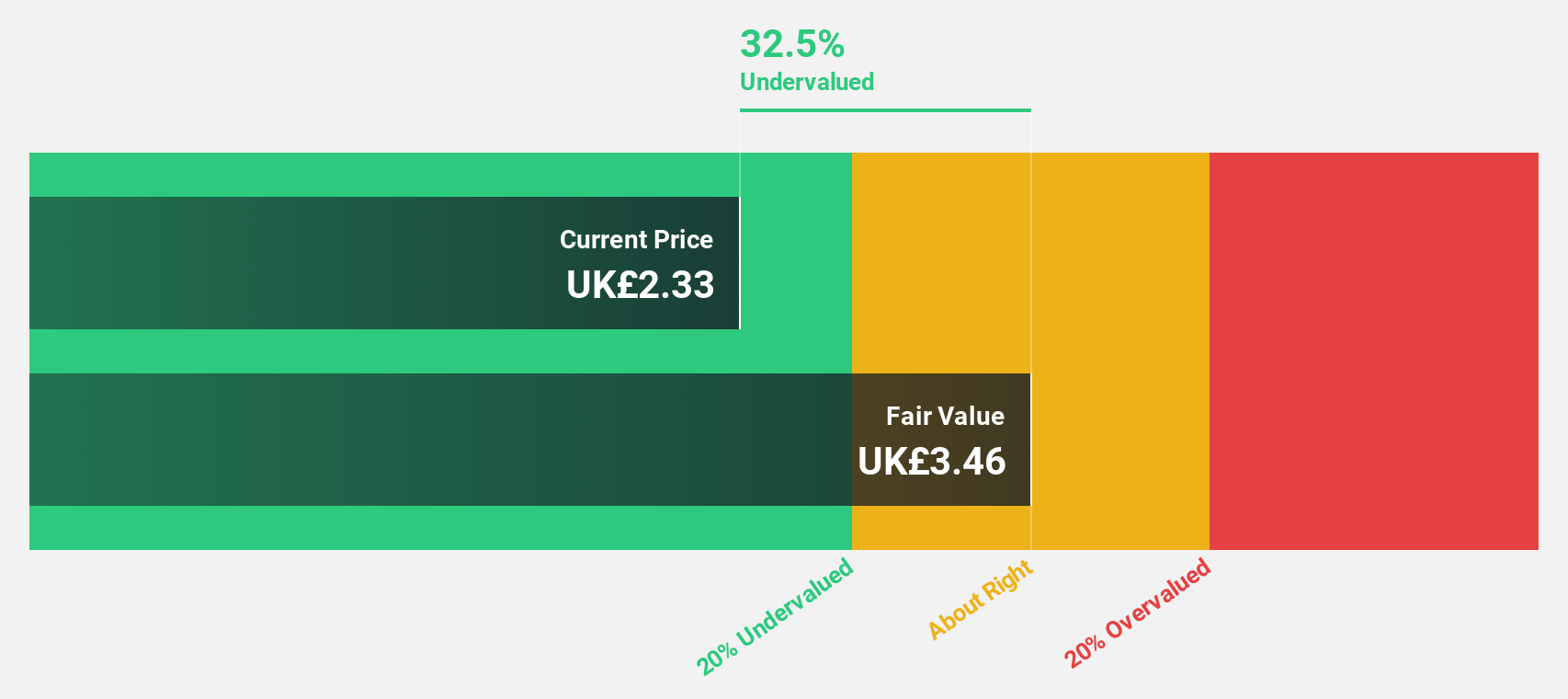

S&U (LSE:SUS)

Overview: S&U plc operates in the United Kingdom, offering motor, property bridging, and specialist finance services, with a market cap of £224.18 million.

Operations: The company generates revenue from motor finance (£88.80 million) and property bridging finance (£13.69 million) in the United Kingdom.

Estimated Discount To Fair Value: 49.7%

S&U is trading at £18.45, significantly below its estimated fair value of £36.65, indicating potential undervaluation based on cash flows. Despite a recent drop in net income to £9.56 million and a dividend reduction, earnings are expected to grow 23.8% annually over the next three years, outpacing the UK market's growth rate of 14%. However, debt coverage by operating cash flow remains a concern for financial stability.

- Upon reviewing our latest growth report, S&U's projected financial performance appears quite optimistic.

- Get an in-depth perspective on S&U's balance sheet by reading our health report here.

Turning Ideas Into Actions

- Reveal the 63 hidden gems among our Undervalued UK Stocks Based On Cash Flows screener with a single click here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:SUS

S&U

Provides motor, property bridging, and specialist finance services in the United Kingdom.

High growth potential established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.1% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|22.0% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.6% undervalued

RO

Community Contributor