- United States

- /

- Interactive Media and Services

- /

- NasdaqGS:BILI

Exploring Three High Growth Tech Stocks In The United States

Reviewed by Simply Wall St

In the last week, the United States market has been flat, although it is up 22% over the past year with earnings expected to grow by 15% per annum over the next few years. In this environment, identifying high growth tech stocks can be particularly appealing as they often have strong potential for innovation and expansion in a dynamic market landscape.

Top 10 High Growth Tech Companies In The United States

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| Super Micro Computer | 29.07% | 27.57% | ★★★★★★ |

| Ardelyx | 21.09% | 55.29% | ★★★★★★ |

| AVITA Medical | 29.48% | 53.36% | ★★★★★★ |

| TG Therapeutics | 29.48% | 45.20% | ★★★★★★ |

| Alkami Technology | 21.99% | 102.65% | ★★★★★★ |

| Travere Therapeutics | 30.33% | 61.73% | ★★★★★★ |

| Clene | 61.16% | 59.11% | ★★★★★★ |

| Alnylam Pharmaceuticals | 21.80% | 58.78% | ★★★★★★ |

| Lumentum Holdings | 21.25% | 118.58% | ★★★★★★ |

| Alvotech | 31.17% | 100.18% | ★★★★★★ |

Click here to see the full list of 229 stocks from our US High Growth Tech and AI Stocks screener.

Underneath we present a selection of stocks filtered out by our screen.

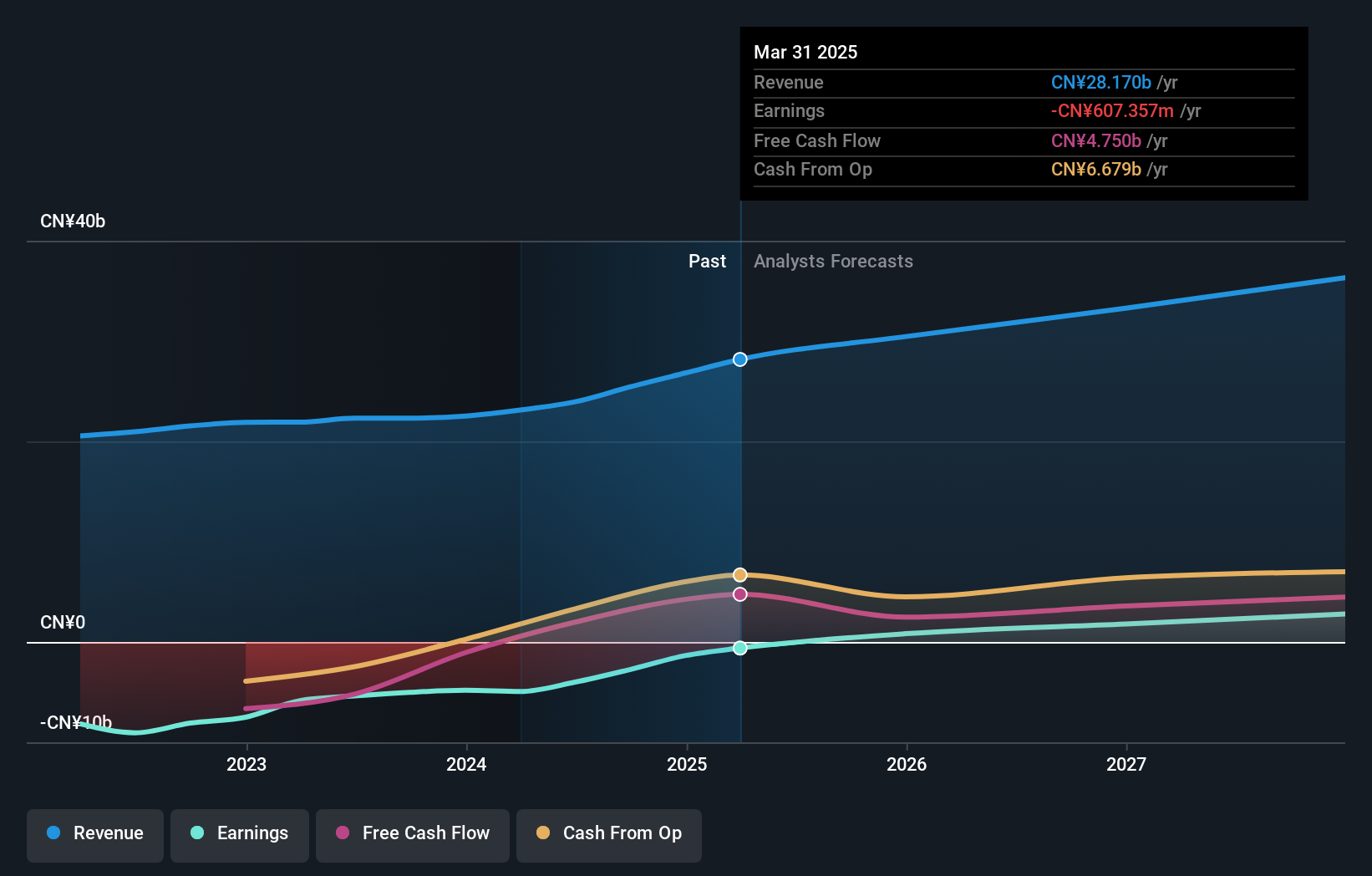

Bilibili (NasdaqGS:BILI)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Bilibili Inc. offers online entertainment services targeting young generations in China, with a market cap of $9.14 billion.

Operations: The company generates revenue primarily through its Internet Information Providers segment, amounting to CN¥25.45 billion.

Bilibili, navigating through the competitive Interactive Media and Services sector, showcases a promising trajectory with its revenue expected to increase by 10.2% annually, outpacing the US market's average of 8.9%. Despite current unprofitability, BILI is on a path to profitability within three years, bolstered by an anticipated annual earnings growth of 65%. This growth is supported by significant investment in R&D, crucial for staying ahead in innovation and content delivery. However, recent significant insider selling could suggest caution among those closest to company operations. With strategic shifts likely required to enhance its Return on Equity—projected at a modest 12.1% in three years—the firm must leverage its robust revenue growth and upcoming profitability to solidify its standing in a rapidly evolving industry landscape.

- Click here to discover the nuances of Bilibili with our detailed analytical health report.

Evaluate Bilibili's historical performance by accessing our past performance report.

Netflix (NasdaqGS:NFLX)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Netflix, Inc. operates as a leading provider of entertainment services with a market capitalization of approximately $452.82 billion.

Operations: The company generates revenue primarily through its streaming entertainment service, which accounted for $39 billion. The focus on streaming services is a key component of its business model.

Netflix's recent performance underscores its robust position in the streaming industry, with a significant 61.1% earnings growth over the past year, surpassing the broader Entertainment sector's decline of 3.2%. This growth trajectory is supported by a forward-looking revenue forecast increase of 10.2% annually, reflecting strong subscriber and ad revenue expansions. Notably, Netflix has committed heavily to innovation and content enhancement through R&D investments and strategic partnerships like the one with EverPass Media for NFL game distributions, ensuring it remains at the forefront of digital entertainment evolution. Additionally, its proactive approach in shareholder returns is evident from its recent share repurchase activity totaling $12.86 billion under the ongoing buyback plan.

- Navigate through the intricacies of Netflix with our comprehensive health report here.

Understand Netflix's track record by examining our Past report.

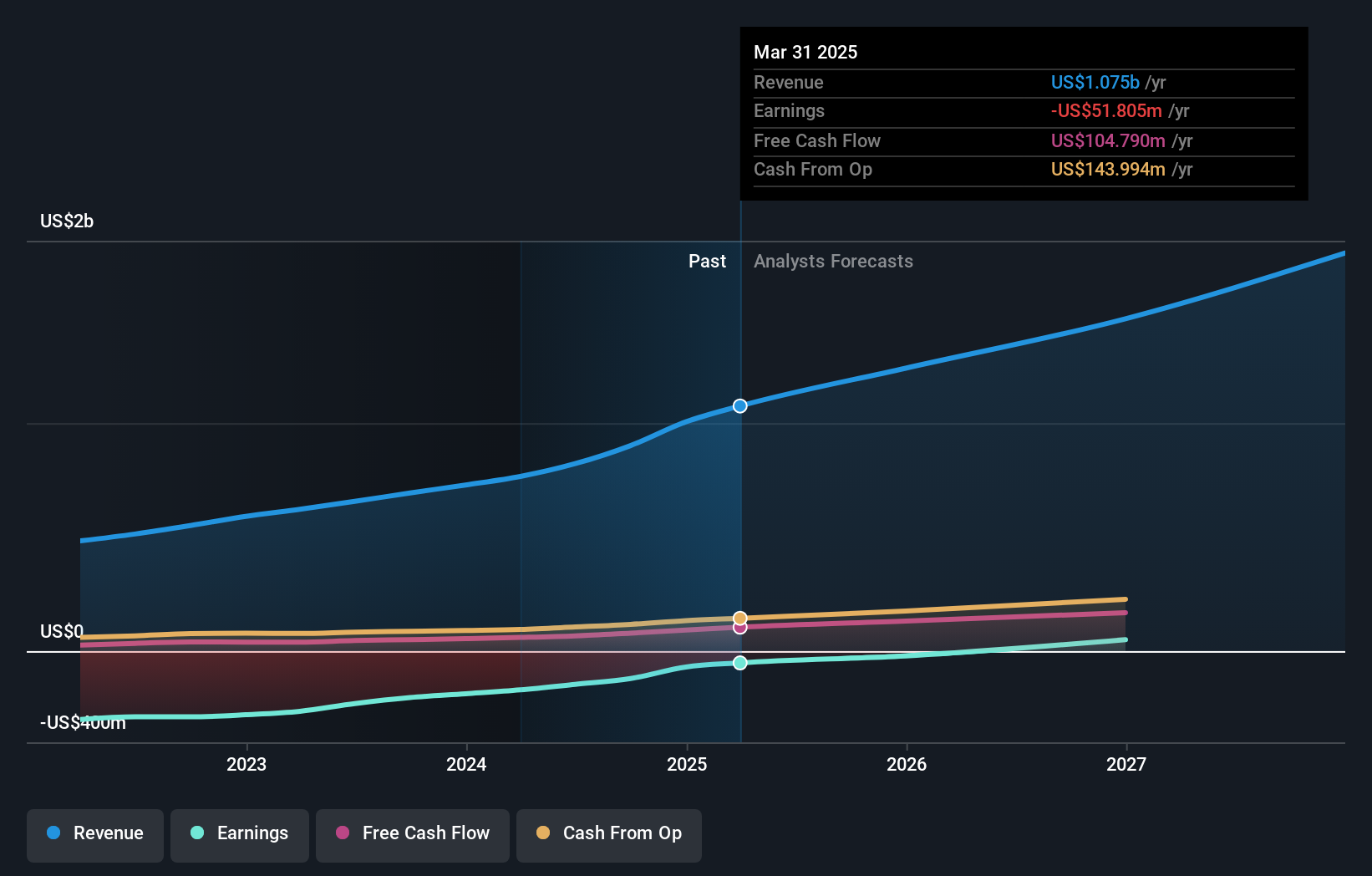

Zeta Global Holdings (NYSE:ZETA)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Zeta Global Holdings Corp. operates an omnichannel data-driven cloud platform offering consumer intelligence and marketing automation software to enterprises globally, with a market cap of $5.58 billion.

Operations: The company generates revenue primarily from its Internet Software & Services segment, amounting to $901.40 million. It offers a data-driven cloud platform that enhances consumer intelligence and marketing automation for enterprises both in the U.S. and internationally.

Zeta Global Holdings, navigating through a dynamic tech landscape, has demonstrated promising growth metrics with an expected revenue increase of 15.8% annually. The company's strategic focus on AI-driven marketing solutions is further underscored by the recent appointment of Ed See as Chief Growth Officer, signaling a deeper push into innovative marketing strategies. Despite current unprofitability, Zeta is poised for significant shifts with projected earnings growth of 125.6% annually and an ambitious R&D investment strategy that aligns with its forward-looking growth trajectory in the competitive software industry. This approach not only enhances its market position but also sets the stage for robust future profitability and industry leadership in leveraging technology for marketing success.

- Get an in-depth perspective on Zeta Global Holdings' performance by reading our health report here.

Gain insights into Zeta Global Holdings' past trends and performance with our Past report.

Taking Advantage

- Investigate our full lineup of 229 US High Growth Tech and AI Stocks right here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bilibili might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:BILI

Bilibili

Provides online entertainment services for the young generations in the People’s Republic of China.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Community Narratives