- United States

- /

- Software

- /

- NYSE:YOU

Is It Too Late To Consider Clear Secure After Its Strong 2025 Share Price Run?

Reviewed by Bailey Pemberton

- Wondering if Clear Secure is still a smart idea after its big run, or if the easy money has already been made? Here is a closer look at what the current price may be indicating about potential growth and risk.

- The stock has climbed 10.3% over the last week, 6.1% over the past month, and is up 43.8% year to date and 49.8% over the last year, putting it firmly on many investors' radar.

- Recent headlines have focused on Clear Secure expanding its airport footprint and broadening its identity verification partnerships. This reinforces the idea that its platform is becoming more embedded in everyday travel. At the same time, market commentary has highlighted growing interest in security and identity-tech names, which helps explain why some investors have been willing to pay up for perceived growth and recurring revenue potential.

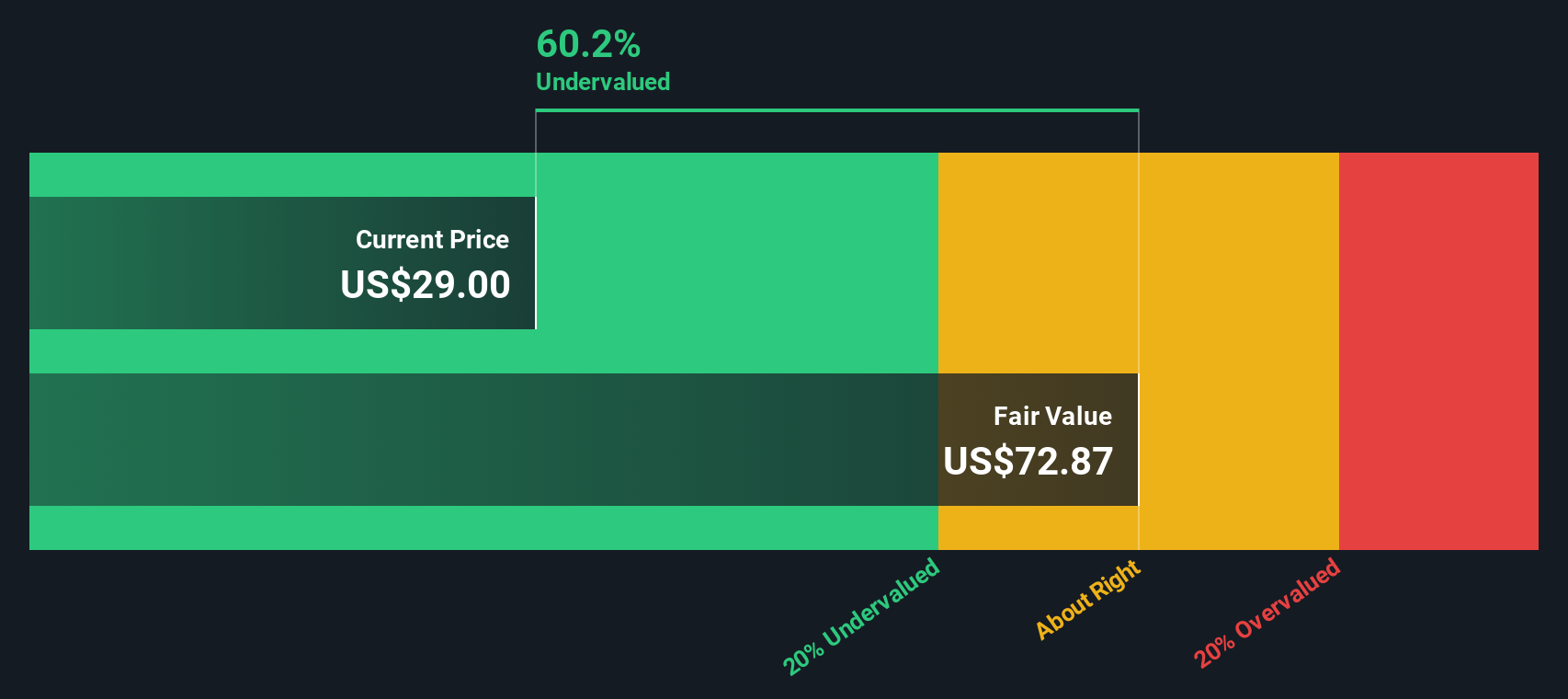

- On our valuation checks, Clear Secure scores a 5/6 for being undervalued, which is a notable starting point but not the whole story. Next, we break down what different valuation approaches suggest about the stock, and then return to a broader way to think about its potential value over the long term.

Approach 1: Clear Secure Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth today by projecting its future cash flows and then discounting those back into current dollars.

For Clear Secure, the latest twelve month Free Cash Flow is about $284.6 Million. Analysts and extrapolated estimates see this rising steadily, with Simply Wall St’s two stage Free Cash Flow to Equity model projecting Free Cash Flow reaching roughly $676.2 Million by 2035, based on a mix of analyst forecasts through 2027 and gradually moderating growth assumptions thereafter.

Rolling these projections together and discounting them back to today yields an estimated intrinsic value of about $70.11 per share. Compared with the current share price, this implies the stock is trading at a 44.6% discount, which suggests the market is pricing in significantly slower growth or higher risk than this model assumes.

On this view, the risk is that expectations are too optimistic, while the potential upside from current levels may appear compelling.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Clear Secure is undervalued by 44.6%. Track this in your watchlist or portfolio, or discover 907 more undervalued stocks based on cash flows.

Approach 2: Clear Secure Price vs Earnings

For companies that are already profitable, the price to earnings, or PE, ratio is a useful way to gauge how much investors are willing to pay for each dollar of current earnings. A higher PE usually reflects stronger growth expectations or lower perceived risk, while a lower PE often signals slower growth, higher risk, or simply a stock that is out of favor.

Clear Secure currently trades on a PE of around 20.9x. That sits below the broader Software industry average of about 32.4x and also below the peer group average of roughly 23.6x, suggesting the market is assigning a modest discount to Clear Secure relative to similar names.

Simply Wall St’s proprietary Fair Ratio aims to refine this picture by estimating what PE multiple a company should trade on, given its earnings growth outlook, profitability, industry, market cap, and specific risks. Because it blends these company specific factors, it can be more informative than a simple comparison with peers or the industry, which may not share the same growth profile or risk mix. For Clear Secure, the Fair Ratio is 26.2x, notably above the current 20.9x, indicating the shares appear undervalued on this metric.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1448 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Clear Secure Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce Narratives, a simple way to attach your own story about a company to the numbers behind its fair value, including your assumptions about future revenue, earnings and margins.

A Narrative on Simply Wall St links three things together: the business story, a forward looking financial forecast, and a resulting Fair Value estimate, so you can clearly see how your view of Clear Secure translates into a price you would be willing to pay.

These Narratives live on the Community page used by millions of investors, are easy to explore or create, and can support your decision making by continually comparing your Fair Value to the current share price.

Because they update dynamically when new information such as earnings, news, or guidance is released, your Clear Secure Narrative stays current without you needing to rebuild your model from scratch.

For example, one Clear Secure Narrative might see international expansion and biometric adoption supporting a Fair Value around $46, while a more cautious Narrative focused on slower growth and margin pressure might point to a Fair Value closer to $20. This gives you a clear sense of how different perspectives translate into very different price expectations.

For Clear Secure, however, we will make it really easy for you with previews of two leading Clear Secure narratives:

Fair Value: $46.66

Undervalued by: 16.7%

Forecast Revenue Growth: 12.58%

- Sees Clear Secure evolving from an airport-centric service into a broader digital identity platform across retail, healthcare, online services, and international markets.

- Builds in rising enrollments, revenue nearly doubling to about $1.5B by 2030, improving margins to 16%, and a future price-to-earnings ratio of 35x to support a bullish Fair Value.

- Flags meaningful risks around high pricing, airport bargaining power, scalability, and cybersecurity or privacy incidents, but concludes that execution success could unlock substantial upside.

Fair Value: $20.05

Overvalued by: 93.8%

Forecast Revenue Growth: 1.82%

- Frames Clear Secure as a mid-cap, travel-linked biometric identity provider whose fortunes are tightly tied to air travel volumes and discretionary spending.

- Assumes only low to mid single-digit growth as competition, privacy concerns, and heavy dependence on U.S. airports curb the upside from diversification and international expansion.

- Warns that if growth slows or macro conditions weaken, valuation multiples could compress sharply, turning today’s optimism into downside for shareholders.

Do you think there's more to the story for Clear Secure? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:YOU

Clear Secure

Operates a secure identity platform under the CLEAR brand name primarily in the United States.

Outstanding track record and undervalued.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)