Advertisement

- United States

- /

- Software

- /

- NasdaqGS:DBX

Dropbox (DBX) Valuation Check After Recent Share Price Momentum Reignites Investor Interest

Recent share performance and why Dropbox is back on investors’ radar

Dropbox (DBX) has drawn fresh attention after the stock gained about 7% over the past month and around 4% over the past 3 months, prompting investors to reassess the company’s current valuation and financial profile.

See our latest analysis for Dropbox.

At a share price of $27.20, Dropbox’s 7.04% 1 month share price return and 3.86% 7 day share price return suggest momentum has picked up recently, even though the 1 year total shareholder return declined 7.83% and the 5 year total shareholder return declined 8.57%.

If this shift in sentiment has you looking beyond a single stock, it could be a good moment to scan other opportunities and see which AI related platforms are gaining traction through the 31 AI small caps

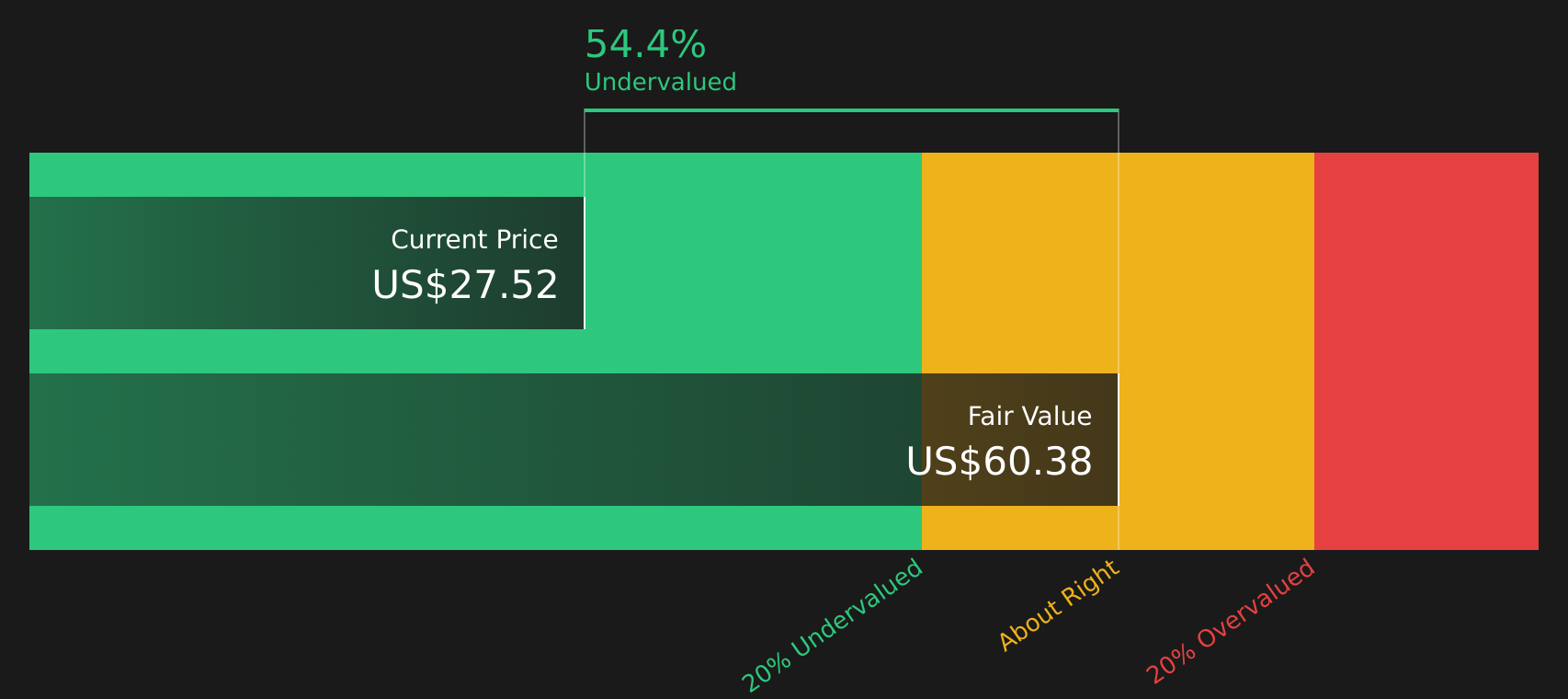

With Dropbox trading at $27.20, sitting close to analysts’ average price target but with an intrinsic value model suggesting a large discount, you have to ask: is this a genuine mispricing, or is the market already banking on future growth?

Most Popular Narrative: 4% Overvalued

At $27.20, Dropbox trades slightly above the most followed narrative fair value of $26.17, setting up a tight debate around what really drives that figure.

The planned expansion and deeper integration of AI-driven productivity tools (Dash), including upcoming self-serve offerings and seamless bundling with Dropbox's existing file sync-and-share product, position the company to capture higher ARPU and accelerate recurring revenue growth as digital transformation and hybrid work drive demand for intelligent, collaborative cloud platforms.

Want to see what sits behind that AI push and the higher recurring revenue focus? The narrative leans on specific margin, growth and valuation assumptions that are not obvious from the headline numbers. The key moving parts are already mapped out. The only way to judge if they stack up is to see them in full.

Result: Fair Value of $26.17 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the narrative still faces pressure from falling revenue and paying users, as well as intense competition from bundled suites that can squeeze pricing and margins.

Wall Street's queuing for one rocket. While SpaceX counts down to its IPO, other companies tied to the new space race are already in orbit. → 20 Compelling Space Companies watchlist · Global Space Race Investing Ideas screener · Scan the sector by valuation on Rocket Lab's valuation page.

Another view on Dropbox’s valuation

While the most followed narrative suggests Dropbox is slightly overvalued at $27.20 versus a fair value of $26.17, the SWS DCF model presents a different picture. It shows an estimated future cash flow value of $60.59, with the stock trading about 55.1% below that figure. Which story do you think is closer to reality?

Look into how the SWS DCF model arrives at its fair value.

Next Steps

With sentiment clearly split between opportunity and caution, it makes sense to move quickly, review the underlying data, and weigh both sides for yourself using the 3 key rewards and 2 important warning signs.

Looking for more investment ideas?

If Dropbox has you thinking differently about your portfolio, do not stop here. Use this moment to scan for other stocks that could sharpen your edge.

- Spot potential standouts trading below their estimated value by running your filters through the 47 high quality undervalued stocks.

- Anchor your portfolio with companies that pair income with resilience by checking out the 10 dividend fortresses.

- Hunt for lesser known opportunities with strong fundamentals by scanning the screener containing 22 high quality undiscovered gems.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DBX

Dropbox

Provides a content collaboration platform in the United States and internationally.

Undervalued with acceptable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2552.0% undervalued

130 followersusers have followed this narrative

0 commentsusers have commented on this narrative

25 likesusers have liked this narrative

BL

BlackGoat on IREN ·

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value:US$71.4848.5% undervalued

227 followersusers have followed this narrative

9 commentsusers have commented on this narrative

33 likesusers have liked this narrative

HE

HedgeY on Arm Holdings ·

The Architecture Layer of AI Computing - But Priced Like the Future Already Arrived?

Fair Value:US$43044.3% undervalued

27 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

HI

Hidden_Rock_Capital on Fiserv ·

Temporary "perfect storm" leads to opportunity to buy financial services leader for less than 5x long-term earnings

Fair Value:US$119.9955.0% undervalued

36 followersusers have followed this narrative

1 commentusers have commented on this narrative

10 likesusers have liked this narrative

Recently Updated Narratives

CH

ChuckN on XPLR Infrastructure ·

Investor Thesis: Why XPLR Infrastructure Could Be Deeply Undervalued in an AI Power Cycle

Fair Value:US$209.0294.3% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

andre_santos on Netflix ·

Netflix - A Fundamental Valuation

Fair Value:US$98.7127.4% undervalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

John_Eric on Reddit ·

Reddit's Discount Is Big Enough to Make Me Suspicious. Here's What I Found When I Went Looking for the Reason.

Fair Value:US$423.6866.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28028.3% undervalued

229 followersusers have followed this narrative

9 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9110.7% overvalued

109 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23054.8% overvalued

122 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

GR

greg_xasak on Fiserv ·

As someone who has dealt directly with them as a CTO for a credit union, I have 8 years of horror stories about doing business with them. If there was any other competitor than could deliver 80% of Fiserv services, there would be a mad rush to migrate to them. They should thank their lucky stars they are a near monopoly. this industry is so ripe for a well funded competitor. Their integration of technology is awful, their ability to fix their own implementation screwups is sadly tragic. Sometimes they just silently kill support tickets without resolution and you never find out until you do a follow up inquiry. Why, because sometimes no one you are dealing with knows how to fix it and knows no one to ask for help. They can not meet their own implementation deadlines and sometimes there is no one on a technical team dealing with you that has any banking or credit union experience. The is an industry insider phrase when you meet other Fiserv customers called being "Fiserved". It means telling others of your worst stories of dealing with them. Ask around, all CTO's have some doozies.

1

|0