Last week’s newsletter focused on the difference between an enduring brand and passing fad. Today, we explore further the concept of a ‘strong brand’ and how it evolves over time.

A strong brand is a tremendous asset for a company. But strong brands aren’t necessarily permanent. The pricing power that often comes with an established brand can gradually begin to fade. Today, we are taking a look at how a strong brand can lose value, and how you can tell the difference between temporary cyclical weakness and more permanent structural weakness. But first:

What happened in markets this week

Here’s a quick summary of what’s been going on:

⚡ Morgan Stanley caps off strong bank earnings with a record quarter (CNBC)

- What happened: Morgan Stanley reported record quarterly profit, up 58% from a year ago. The increase in profits was supported by record stock trading revenue and strong investment banking activity. This included a 70% increase in equity underwriting business.

- How it impacts investors: Wall Street investment banks are benefitting from the increase in IPOs, mergers and acquisitions, and capital raising, as well as trading volumes. Much of this is driven by the AI sector. Whether it's a bubble or not, investment banks are making hay while the sun shines.

- Next steps: Use the stock screener to compare banks benefiting from increased investment banking deal flow.

💥 IBM tumbles after weaker-than-expected preliminary results (Yahoo Finance)

- What happened: An unexpected profit warning from IBM led to a 25% drop in the stock price, its biggest one-day decline in decades. The company said some customers shifted spending toward AI servers and memory infrastructure late in the quarter. IBM said both revenue and earnings for the second quarter will be below consensus estimates.

- How it impacts investors: The broader implication is that companies are reallocating IT budgets to fund AI-related infrastructure spending. In particular, software and non-AI related infrastructure budgets are being cut.

- Next steps: Review IBM's Company Report to see how these results affect IBM’s longer term trajectory.

🔧 ASML raises outlook as AI chip demand drives record orders (Yahoo Finance)

- What happened: ASML beat second-quarter expectations and raised its 2026 sales guidance as demand for its EUV lithography machines continued to accelerate. The company said customer orders now extend through 2028, providing unusually strong revenue visibility.

- How it impacts investors: ASML is the first major AI related company to report. These results might restore some confidence in the ‘ AI trade’ which has been under pressure over the last few weeks. However, this is just one company, and a very specialized one at that. It’s probably worth looking at a broader sample over the next few weeks.

- Next steps: Explore the Top High Growth Tech & AI Stocks with Spotless Financials to find quality AI related companies to follow during earnings season.

📦 Stripe and Advent bid to take PayPal private at a 28% premium (CNBC)

- What happened: Stripe and private equity firm Advent International have jointly offered to acquire PayPal for US$60.50 per share, valuing the company at more than US$53 billion. PayPal’s board is expected to review the proposal as early as next week. The offer is reportedly backed by roughly US$50 billion in financing.

- How it impacts investors: If successful, this deal could create a fintech powerhouse, and add new catalysts to PayPal’s business. It could also shake up the fintech space as other companies consider their options.

- Next steps: Explore our Fintech investment ideas to compare companies across the digital payments space and see which businesses still trade below their estimated fair value.

A strong brand might not be a permanent one

In last week's newsletter, we explored the difference between a lasting brand and a passing fad. That’s the first step in assessing a brand, but the work isn’t finished upon identifying it.

The reality is even strong brands are susceptible to being unseated. Whether it is 5 or 150 years old, it can lose relevance (and value) for a number of reasons.

Once you’ve identified a strong brand, you need to keep assessing its strength, and the strength of competitors. This becomes particularly relevant when a company is going through a period of weakness.

Cyclical vs secular weakness

Many of the most recognizable brands operate in cyclical industries, so even the best brands are affected by economic factors. This is actually good news for investors, as it creates buying opportunities when a company’s revenue and earning growth numbers take a knock.

If weakness is purely due to cyclical factors, there’s a good chance investors are looking at a bargain.

However, weakness can also be structural, which is more permanent. This can be the result of major changes in a company’s competitive position, or its product category or industry.

Differentiating between a bargain and a value trap can come down to being able to tell the difference between cyclical weakness and more permanent structural weakness.

How do brands lose their power?

A brand can lose value for a number of reasons, which broadly fall within four categories:

- Entire categories get disrupted by changes in technology.

- Shifting consumer tastes and behavior.

- New entrants rewrite the rules for a category or industry.

- Legacy brands fall victim to their own organizational inertia.

From a brand and product perspective these four factors are most important. There are other risks that can ultimately hurt a brand too: regulatory changes, dependency on a single channel or platform, or financial stress are all examples.

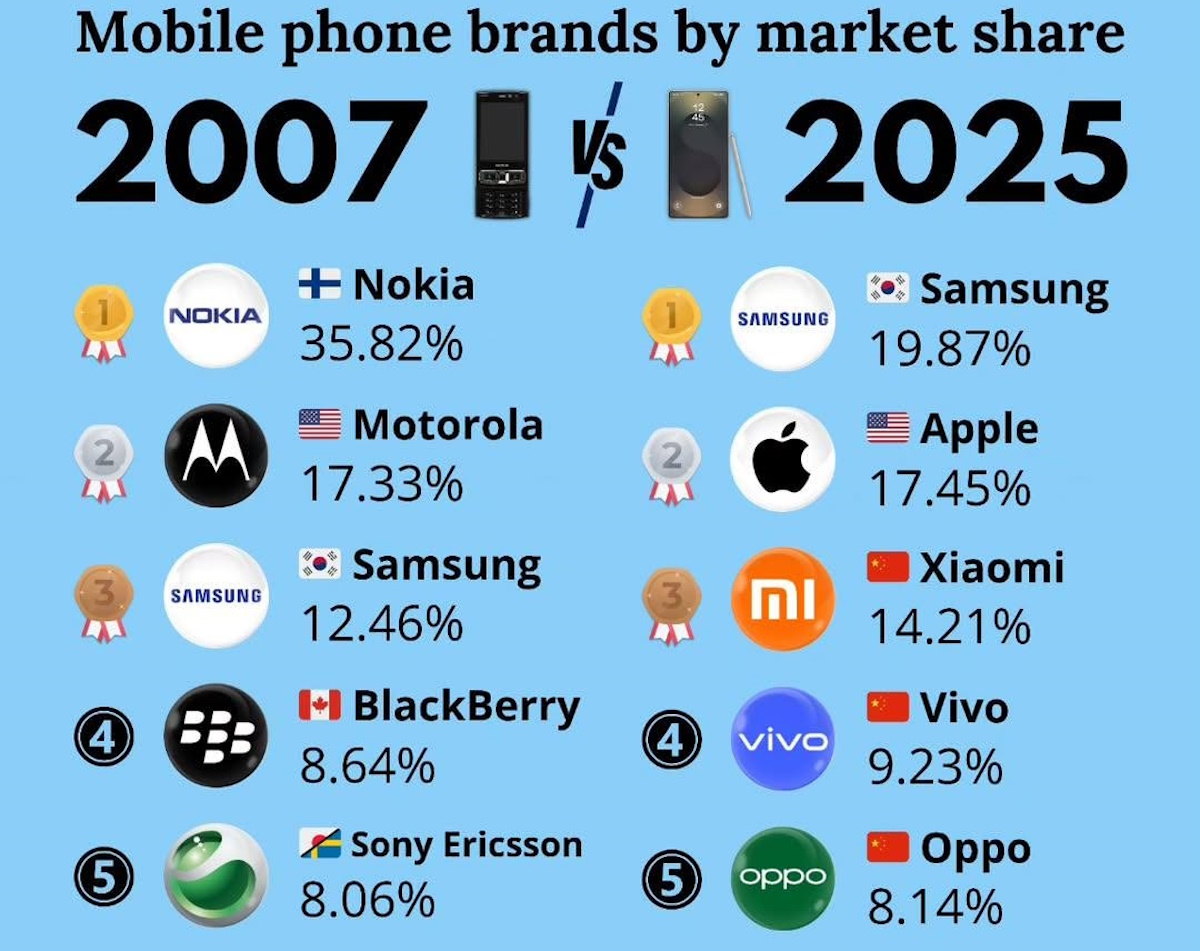

One of the biggest examples of category disruption has occurred in the mobile phone market since 2007 when Apple introduced the iPhone. The upheaval in the mobile phone market has featured tech disruption, a new entrant rewriting the rules, and inertia by legacy brands.

Source: Global mobile phone market share: 2007 to Q2 2025 - Civixplorer.com

Since the iPhone’s launch, four of the five market leaders (including Nokia with 35%) drifted into obscurity. Yet Samsung managed to navigate its way to the top of the list, along with Apple, an entirely new player.

Samsung’s success had a lot to do with embracing an open-source operating system (Android) while others tried to persevere with their own software. The company managed to build a reputation for offering phones with features that were essentially very similar to an iPhone (including an app platform, the Play Store), at a much lower price point.

This story is still evolving though. Over time, the differences between the Android models sold by various brands have narrowed. Newer brands like Xiaomi are able to offer similar products at a cheaper price point. Without a unique differentiator, Samsung’s edge could also be vulnerable.

Assessing a brand’s future strength

Assessing the outlook for a brand is both a quantitative and a qualitative process. It’s also a two way process:

- Is this brand showing strength over time?

- Are its competitors gaining strength?

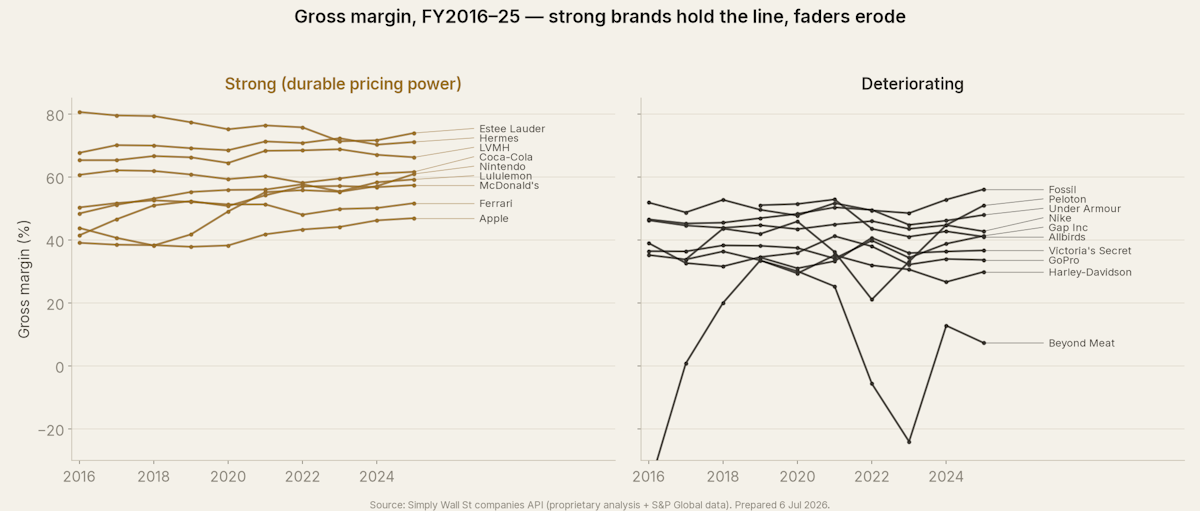

Gross Margin Trends

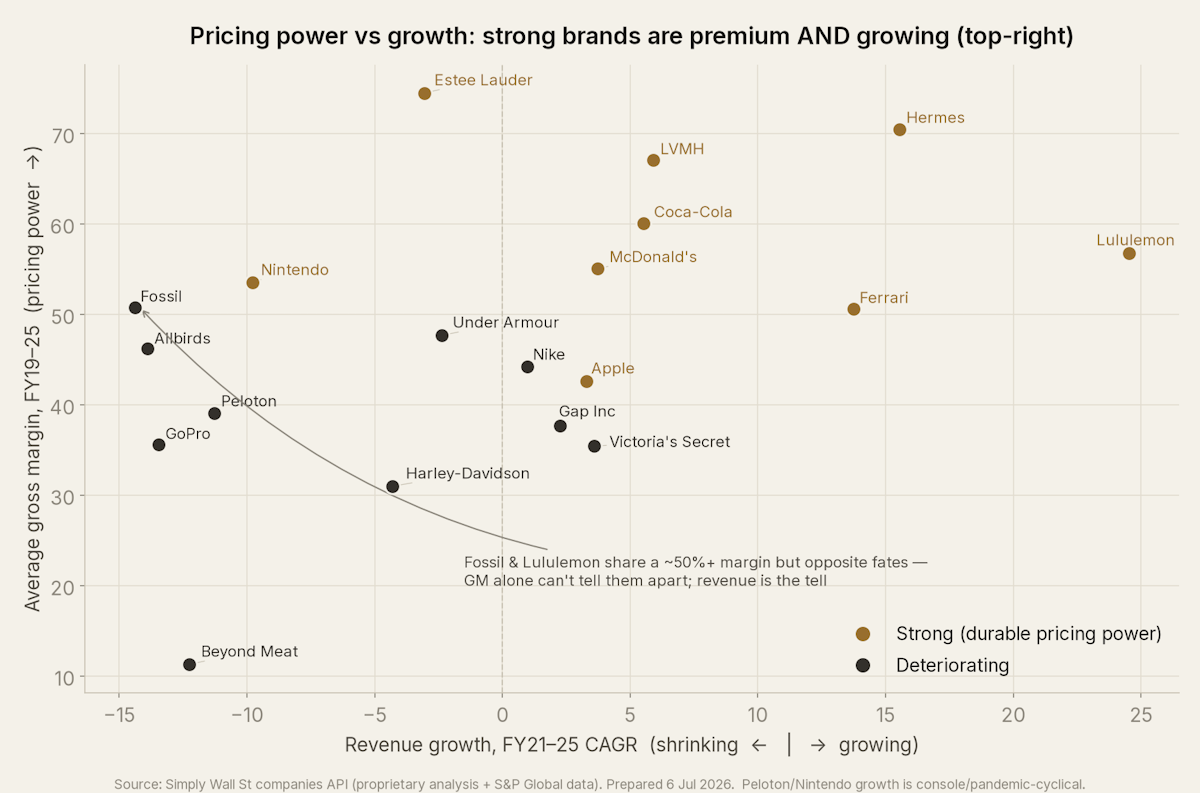

When a company loses margin, it’s very difficult to get it back. Companies with durable brands are very reluctant to lower their margin, and doing so is often a sign of weakness. Keep in mind that margins should also increase with growing revenue due to economies of scale.

By looking at long term gross margin and revenue growth trends, we can get an idea of a company’s ability to maintain pricing power, while increasing sales.

The chart below shows the strongest brands maintaining 50%+ gross margins AND positive revenue growth over a five-year period.

It’s important to track these metrics over the course of economic cycles. Even the strongest brands will experience temporary weakness, but they should be able to bounce back and record new gains when the cycle turns.

The opposite can also be true. A brand that doesn’t necessarily have enduring strength might capitalize on temporary consumer strength or a passing fad. That can result in higher margins and/or a spike in revenue. If those trends don’t last, the brand probably isn’t the asset it may appear to be.

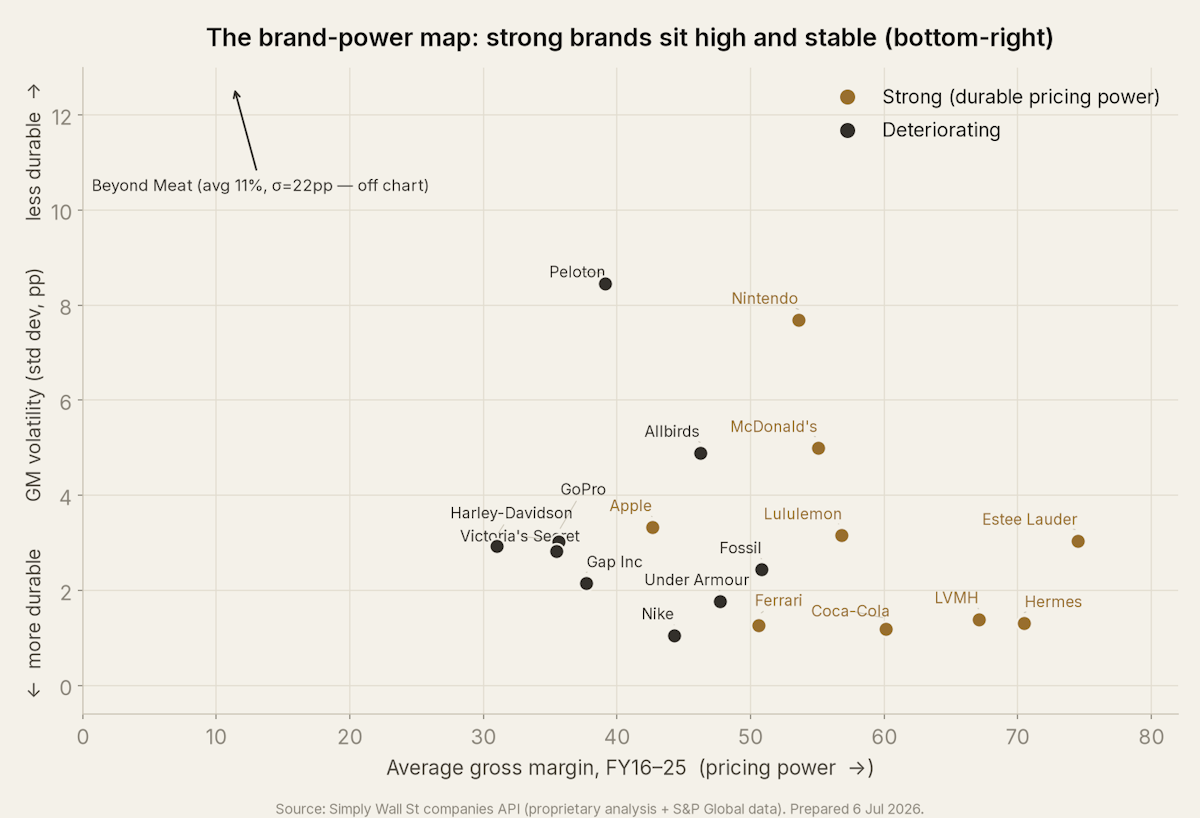

Gross margin volatility is the signal to look out for. Strong brands have lower margin volatility, while maintaining higher margins over time.

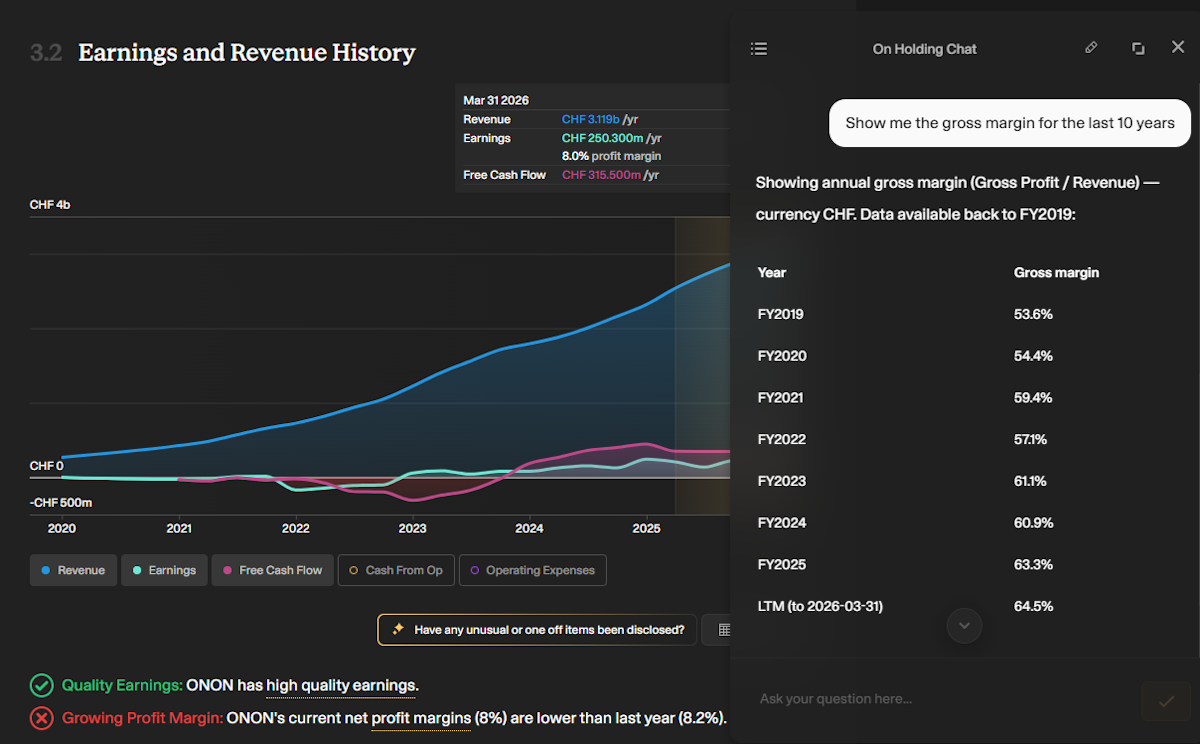

Want more detail on the gross margin trend? You can ask the chatbot below the Earnings and Revenue chart (section 3.2) of the Company Report:

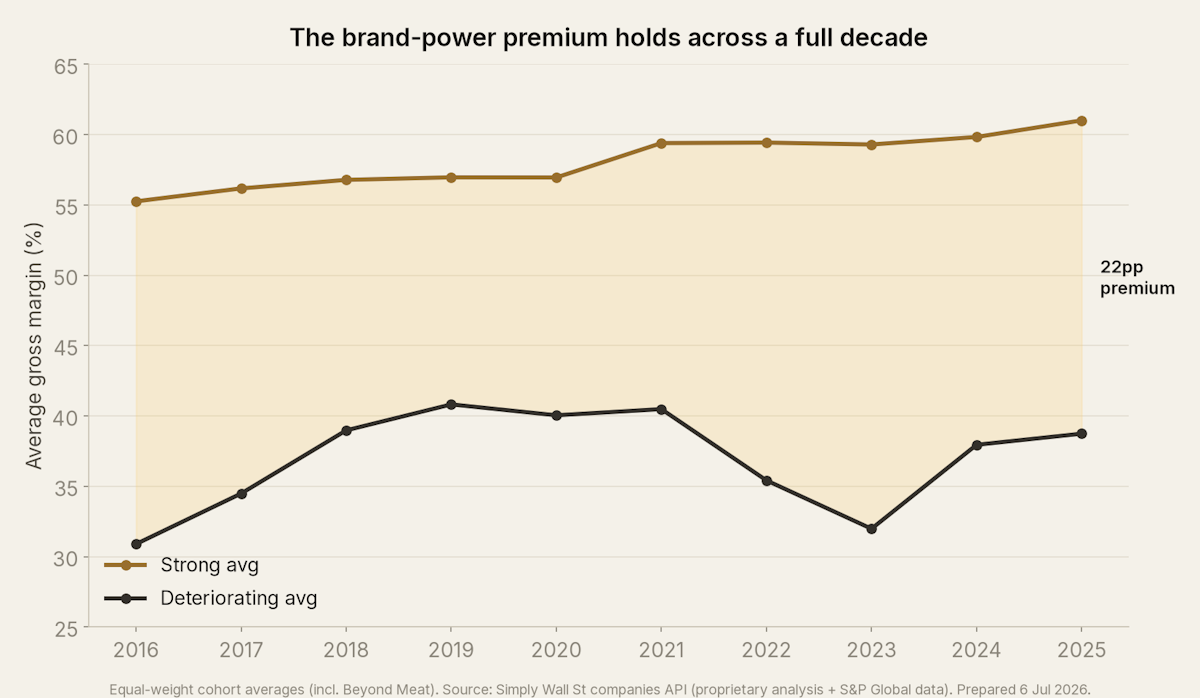

This chart demonstrates the difference over a decade between stable and strong brands, and weaker brands with bigger swings in volatility.

The cohort of stronger brands (shown above) yielded a 22% return premium over a ten-year span compared to the deteriorating brand cohorts.

Market share

Changes in relative market share can sometimes be an indication of brands within an industry gaining or losing strength. But, keep in mind that new entrants often attempt to buy market share with massive spend on marketing. The risk is that a company spends $2 to make $1, and doesn’t hold on to the market share it gains. Any market share gains should be compared to Sales and Marketing spend (section 3.1 of the Company Report on Simply Wall St).

Premium alcohol brands are being tested

The alcoholic drinks market is facing one of its biggest tests ever. There’s plenty of evidence to suggest that consumption patterns are changing. Younger consumers are drinking less, consumers in general are becoming more health conscious, and discretionary budgets are being reallocated.

On the other hand, alcohol is one of the oldest product categories around. Is this a temporary dip, or a structural change? This is a question that has yet to be answered.

This is where a combination of qualitative and quantitative analysis is required. A structural reset may well be occurring for the industry, but that doesn’t mean it will affect every brand equally.

Pernod Ricard owns a broad portfolio of alcohol brands, many in premium categories. Over the last 10 years, its gross margin has fallen from 62% to 59%, but remained within a relatively tight range.

On the other hand, gross margins for mass market brands like Anheuser-Busch and Heineken have bounced around in a wider range. Heineken’s margins have fallen from around 40% to 35%.

From a qualitative perspective, a decline in consumption might affect the “every day” brands a lot more than the “special occasion” brands.”

A fork in the road for luxury brands

Luxury brands, some of which overlap with alcohol (LVMH for example), are also being tested. True luxury brands may be more durable, while the aspirational brands will need to prove themselves.

Aspirational brands, which are accessible to upper-middle-income consumers, can prove themselves very valuable at times, but they can also be subject to temporary trends and consumer tastes. Check the LVMH Narratives page to see what community members are saying about the company.

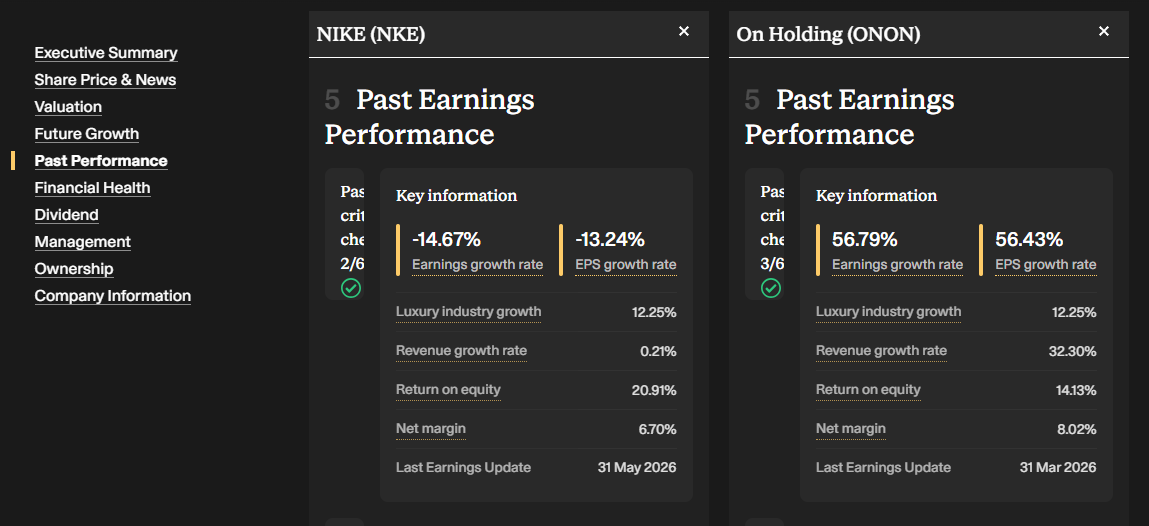

Further down the list are sports brands (which are sometimes classified as luxury brands too). In this segment the most well known incumbent ( Nike) is being challenged by the smaller, younger On Holding. The former is trading on a 20x P/E, while the latter trades at 40x. This is a great case study to test one of the world’s most well known brands against a challenger.

Is On Holding building a lasting brand, or is it a temporary winner in a competitive market. You can start by comparing the two companies with the stock comparison tool, then check the Narratives on Nike to see what community members think Nike needs to do to reclaim its leadership.

To search for, and compare company brands, you can use the stock screener. The key metrics worth testing within the screener:

- Gross margin: is it above 50% and is it rising, or at least stable?

- Revenue: Rising, stable, or falling?

- ROCE or ROE: Ideally higher than 15%. Look at the historical and expected trend too.

- You can also spot brands that might be deteriorating by screening for companies with metrics below these thresholds.

💡 The Insight: Broadening the Competitive Lens

Assessing a brand’s value is very much a two sided process. A brand needs to be tested against direct competitors, as well as the broader market environment. Sometimes competitors battle it out, only to be displaced by someone else entirely.

The classified business is a good example of this. Prior to the internet’s arrival, classified ads were amongst one of the most profitable parts of a newspaper.

The internet decimated that business as platforms like eBay emerged.

In local markets, platforms like Gumtree and OLX (owned by Prosus) battled to become THE trusted classified brand in each market. These platforms benefit from network effects, so ultimately only one tends to survive. After spending billions trying to dominate each market, both were displaced by Facebook Marketplace, which already had the audience, and just needed to launch the product.

When you’re testing a brand, it's crucial to consider direct competitors, as well as less obvious indirect competitors and substitutes.

Key events next week

Monday

- 🇨🇦 CAD Inflation Rate YoY

- 📉 Forecast: 3.0%, Previous 3.2%

- ➡️ Why it matters: Cooling inflation strengthens will give the BoC more flexibility.

Tuesday

- 🇬🇧 GBP Unemployment Rate

- ⏸️ Forecast: 4.9%, Previous 4.9%

- ➡️ Why it matters: A steady rate keeps the BoE on a cautious path.

Wednesday

- 🇯🇵 JPY Balance of Trade

- 📉 Forecast: -700.0B, Previous -378.7B

- ➡️ Why it matters: A widening deficit could weigh on the yen and Japan's growth outlook.

- 🇬🇧 GBP Inflation Rate YoY

- 📉 Forecast: 2.4%, Previous 2.8%

- ➡️ Why it matters: A sharp drop would give theBOE a stronger case for rate cuts.

Thursday

- 🇪🇺 ECB Interest Rate Decision

- ⏸️ Forecast: 2.4%, Previous 2.4%

- ➡️ Why it matters: A hold signals the ECB sees current policy as appropriately balanced.

Friday

- 🇯🇵 JPY Inflation Rate YoY

- 📈 Forecast: 1.7%, Previous 1.5%

- ➡️ Why it matters: Rising inflation strengthens the case for the BoJ to keep normalizing rates.

It’s the first big week of earnings season, with big tech names, and other widely followed companies due to report second quarter results:

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. Any comments below from SWS employees are their opinions only, should not be taken as financial advice and may not represent the views of Simply Wall St. Unless otherwise advised, SWS employees providing commentary do not own a position in any company mentioned in the article or in their comments.We provide analysis based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Richard Bowman

Richard is an analyst, writer and investor based in Cape Town, South Africa. He has written for several online investment publications and continues to do so. Richard is fascinated by economics, financial markets and behavioral finance. He is also passionate about tools and content that make investing accessible to everyone.