One of the first terms an investor learns is “dividend yield.”

Graham, Buffett, and Lynch built reputations partly on income-focused strategies, and a tidy rule of thumb followed them into popular wisdom: higher yield, better stock.

It's intuitive, it's measurable, and… it's often wrong.

Today, we’ll be walking through how investors can avoid “yield traps,” and instead spot “dividend aristocrats.” Similarly, we’ll walk through how a balance of income and capital growth could be achievable.

What happened in the markets this week?

🤖 AI rivalry puts Alibaba under fresh regulatory pressure (CNBC)

- What happened: Anthropic accused Alibaba of using thousands of proxy accounts to make 28.8 million queries to its Claude AI model in an alleged attempt to replicate its capabilities. Alibaba shares fell to a 16-month low after the news.

- How it impacts investors: The dispute highlights rising geopolitical and regulatory risks across the AI sector, particularly for Chinese tech companies. Investors may see increased volatility as governments tighten oversight of AI development and cross-border technology access.

- Next steps: Review Alibaba’s company report to determine whether this news impacts its fundamentals.

💾 AI chip optimism returns after strong outlooks from Micron and Qualcomm (Reuters)

- What happened: Micron forecast quarterly earnings above expectations, while Qualcomm projected US$15 billion in annual data center revenue by 2029. The updates sparked a broad rally in semiconductor stocks, adding more than US$400 billion in market value across the sector.

- How it impacts investors: The forecasts suggest demand for AI infrastructure remains strong despite recent concerns about stretched valuations.

- Next steps: Use our AI chips screener to compare companies benefiting from AI infrastructure demand.

🚗 Volkswagen unlocks cash with major engine business sale (Reuters)

- What happened: Volkswagen agreed to sell a 51% stake in its Everllence diesel engine business to Bain Capital in a deal expected to generate about €7.4 billion in proceeds. Volkswagen will retain a 49% stake while using the transaction to sharpen its focus on its core automotive business.

- How it impacts investors: The sale reflects how traditional automakers are reshaping their portfolios and raising capital to support strategic priorities.

- Next steps: Review Volkswagen's fundamentals and track how the transaction could affect its long-term outlook.

💾 SK Hynix targets blockbuster US listing to fund AI expansion (Finance News Network)

- What happened: SK Hynix announced plans to raise up to US$29.4B through a US listing of American Depositary Receipts. The company said it plans to use the proceeds to build new chip factories in South Korea and purchase advanced chipmaking equipment to support growing AI demand.

- How it impacts investors: The planned listing reinforces strong investor appetite for AI infrastructure and semiconductor companies. It also signals that leading chipmakers are continuing to invest heavily to meet long-term AI demand.

- Next steps: Explore our High Growth Tech & AI investing ideas to discover companies benefiting from the AI infrastructure buildout.

📱 Meta’s prediction markets plans shake betting stocks (CNBC)

- What happened: Meta is developing a “prediction markets app” for virtual betting and stock trading. Following reports of the project, shares of DraftKings (NASDAQ:DKNG), Flutter Entertainment (NYSE:FLUT), and Robinhood (NASDAQ:HOOD) declined as investors assessed the potential competitive impact.

- How it impacts investors: The announcement highlights how new platform entrants can quickly reshape expectations in adjacent industries. Investors may see increased volatility across sports betting and prediction market-related stocks as competition evolves.

- Next steps: Use our Stock Screener to scan for companies across online betting, fintech, and digital platform industries to identify opportunities and risks.

Why “dividend yield” is not an all-rounded metric for success

Dividend yield is calculated by dividing a company's annual dividend by its current share price.

Put simply, it tells investors how much annual dividend income they're receiving for every dollar invested at today's share price. And yes, a higher dividend yield generally means a higher income return.

But there are a few challenges that come from solely relying on this metric.

Firstly, the dividend yield is a ratio. A high yield can reflect a generous dividend, but it can also simply mean the company's share price has fallen sharply.

Imagine a company pays a $1 annual dividend. If its share price is $20, the dividend yield is 5%. But if the share price falls to $10, the yield suddenly doubles to 10%. The investor is not receiving any extra cash, the yield has risen simply because the market value of the business has fallen.

Secondly, a company may have an enticing yield, but what if that company burns through its cash and is unable to sustain its payouts?

That is how yield traps happen.

What a yield trap actually looks like

A “yield trap” is a company that looks like an opportunity at first glance; a high yield drawing investors toward a business that is, in fact, deteriorating.

The good news? The warning signs aren't hard to spot.

Payout ratio above 80 to 90%. Research has shown that companies with a high payout ratio have underperformed in the long run. This generally happens because the company is paying out most of what it earns - or worse, more than it earns - to attract investors. As a reference point, the S&P 500’s average payout ratio is approximately 38%.

Dividends paid from earnings that aren't converting to cash. A company can report accounting profits while actually burning cash. Free cash flow is a metric that can point to whether a dividend can be sustainable.

High debt levels. A highly leveraged company paying a generous dividend is, in effect, prioritising its shareholder income over its own balance sheet health. When interest rates rise, as they did since the years following Covid-19, that trade-off becomes painful.

Volatile or deteriorating earnings. Predictable, recurring revenue is what makes a dividend sustainable. Companies in structurally challenged industries or with lumpy earnings from project-based revenues, often cannot sustain a high payout through a rough patch.

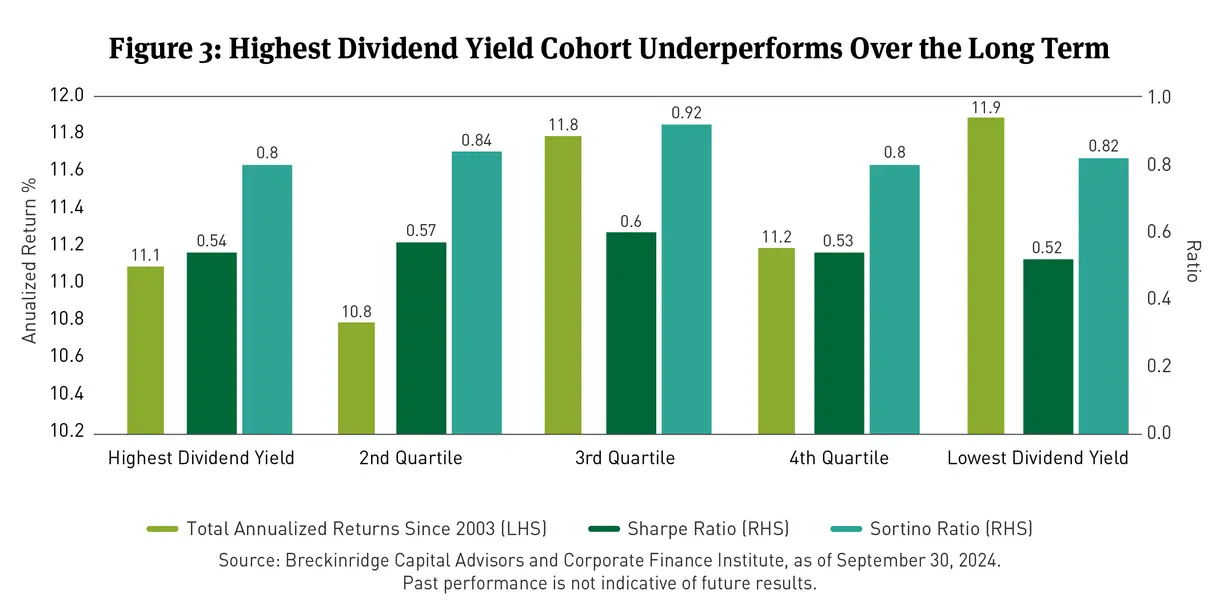

One study running across nine decades sorted dividend payers into quintiles and raced each against the S&P 500.

The result is the whole point of this piece: the second-highest quintile beat the index in 6 out of 10 decades. Every other group, the very highest yielders included, only managed it half the time.

That said, dividends matter enormously. Since 1960, ~85% of the S&P 500's cumulative total return has come from reinvested dividends and compounding.

To illustrate, that means $10,000 invested and reinvested back then, means you'd have around $7.58 million today. If we only looked at price return, that would’ve amounted to just $1.14 million.

What a compounder looks like instead

If the highest yield tends to be a trap, the “dividend grower” is its opposite.

Stocks sorted by dividend policy since 1973 show the gap clearly:

- Growers and initiators: +10.2% a year, at roughly 16% volatility and a beta of 0.89. That means more return for less risk than the market itself.

- Cutters and eliminators: -1% a year, at nearly 25% volatility and a beta of 1.22. In other words, more risk taken only to lose money.

In growth-of-$100 terms over that period, the growers reached about $17,375. The cutters fell to $60.

This shows that yield itself isn't the driver. What matters is what a long record of raising one signals about the business: earnings that hold up through recessions, a balance sheet that isn't stretched, and management disciplined enough to keep the streak alive rather than borrow to fund it.

The S&P 500 Dividend Aristocrats, companies that have raised their dividend for 25 years straight, are the cleanest example of that profile, and these are the traits they have in common:

Wide moats and recurring revenue. The names that clear the bar tend to be the same breed: consumer staples with market leadership and almost boring, consistent demand. Names such as Coca-Cola, Procter & Gamble, McDonald's, Walmart, Caterpillar are some examples. These businesses endured recessions while others were forced to cut.

A balance sheet built to defend the payout. A 25-year record needs both the free cash flow to fund a rising dividend and the financial strength to protect it when earnings wobble. It's why dividend-quality portfolios lean so heavily on investment-grade names; in one such strategy, 90% of holdings carried an S&P credit rating of A- or better.

Disciplined management. Management focused on prudent accounting - funding the dividend rather than spending the cash on empire-building acquisitions. Quality, durability and restraint, in that order.

And the aggregate yield of the Dividend Aristocrats index is unremarkable, around 2.5% versus the S&P 500's 1.8%. But these companies remained consistent.

The floor also held when it mattered. Since 1990, the index has beaten the S&P 500 in about two-thirds of its down months, carrying a beta of 0.8 and a worst drawdown of -44% against the market's -51%.

And over those three decades, it compounded ahead of the index at 11.6% a year versus 10.6%.

Strong fundamentals, robust balance sheet, less volatily, lower drawdowns: that's the compounder's signature, and almost none of it shows up if you sort only by yield.

👉 Check out this custom-built screener that scans specifically for US Growing Dividend Payers (~3-5% yield) to give you a starting point for your research.

Balancing income and capital growth

But the lesson isn't to buy low-yield stocks. It's that the level of the yield tells you little while the direction tells you a whole lot more.

A stock yielding 2% today but growing its dividend 8% a year will, within a decade, pay more on your original investment than a flat 6% yielder, while being far less likely to cut along the way.

So as the numbers show, income and growth aren't opposing goals. The businesses that compound one tend to compound the other.

It's also worth noting that the place to hunt for growers has widened. Income was known to come from large, mature, slow-moving businesses. That's now changing as software becomes an everyday need. Five of the "Magnificent Seven," including Microsoft, Apple and Alphabet, now pay a dividend.

And the income opportunity increasingly reaches into smaller companies, emerging markets and higher-growth sectors despite history showing differently, investors just need to remain flexible and open-minded.

Two caveats:

1. Exceptions exist. A few high-yielders like Altria, KeyCorp and Citigroup have delivered both a high yield and strong returns in the last three years. But they're exceptions, and separating them from the traps takes the fundamental work above.

2. The logic extends past dividends entirely. Berkshire Hathaway has never paid one, on the view that capital reinvested well beats capital paid out. It has compounded at roughly 19.9% a year since 1965, against 10.4% for the S&P 500.

👉 We’ve also built a screener for Dividend Powerhouses, which scans for stocks with both strong fundamentals and higher dividend yields (over 5%), which can be contenders for both future capital growth and sustainable income.

💡 The Insight: Yield is the question, not the answer

A high dividend yield looks like proof a company is sharing its success with you. More often, it's the market signalling a payout it expects to be cut, and chasing it risks losing the income and the capital at once.

The evidence is consistent: the highest-yielding stocks have rarely been the best performers, while steady dividend growers have delivered higher returns with lower volatility for decades. What separates the two isn't the size of the yield but the strength of the business behind it.

So the yield is only the starting question. The answers sit one layer beneath it:

- Is the payout ratio sustainable? A 30-50% range is the sweet spot. Low enough to survive a bad year, high enough to keep raising the dividend ahead of inflation, and ideally it's covered by free cash flow, not just accounting earnings.

- Has the dividend grown steadily for five to 10 years? A consistent record is a sign of financial discipline.

- Can the balance sheet support it?

- Are earnings stable and recurring?

A high yield propped up by a stretched payout ratio and heavy debt is one profile. A lower yield with steady dividend-per-share growth and a clean balance sheet is the other.

That's the difference between a yield trap and a compounder.

Ultimate Guide to Dividend Investing

Simply Wall St’s CEO, Al Bentley, goes through how you can use the platform to enhance your dividend investing strategy through this video.

Key events next week

Tuesday

- 🇨🇳 China Manufacturing PMI (June)

- Previous: 50.0

- Why it matters: As the world's second largest economy, China's manufacturing activity is a key gauge of global demand. A stronger reading could boost sentiment toward commodities and mining stocks.

Wednesday

- 🇪🇺 Euro Area Inflation Rate (Flash, June)

- Previous: 3.2%

- Why it matters: Inflation remains the ECB's biggest focus. A surprise could shift expectations for future interest rate cuts across Europe.

Thursday

- 🇺🇸 Unemployment Rate (June)

- Previous: 4.3%

- Why it matters: Investors will watch whether unemployment continues to rise. A weaker labour market could increase expectations for Fed rate cuts, while a stronger-than-expected reading may delay further easing.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Mitch Lawler and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. Any comments below from SWS employees are their opinions only, should not be taken as financial advice and may not represent the views of Simply Wall St. Unless otherwise advised, SWS employees providing commentary do not own a position in any company mentioned in the article or in their comments.We provide analysis based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.