- United States

- /

- Software

- /

- NasdaqGS:CRWD

Assessing CrowdStrike After Its 49% 2025 Surge and AI Security Momentum

Reviewed by Bailey Pemberton

- If you are wondering whether CrowdStrike Holdings is still worth buying after its huge run, or if the best days are already priced in, you are not alone. That is exactly what this breakdown will tackle.

- The stock has cooled off a bit in the last month, down about 7.0%, but it is still up 49.0% year to date and 350.2% over three years. This naturally raises the question of whether the current price fairly reflects its growth story.

- Recent headlines have focused on CrowdStrike's expanding role in enterprise cybersecurity and high profile partnerships, reinforcing its reputation as a go to platform for cloud native threat protection. At the same time, sector wide optimism around AI powered security tools has added extra momentum and volatility to names like CrowdStrike.

- Despite that strength, our valuation framework gives CrowdStrike a score of 0/6, suggesting it screens as expensive on traditional checks. Next, we will walk through the main valuation approaches that lead to that verdict, and then finish with a more nuanced way to think about what the stock might really be worth.

CrowdStrike Holdings scores just 0/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: CrowdStrike Holdings Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model estimates what a business is worth today by projecting the cash it can generate in the future and then discounting those cash flows back to their value in today’s dollars.

For CrowdStrike Holdings, the model starts with last twelve months free cash flow of about $1.1 billion and projects strong growth over the next decade. On Simply Wall St’s two stage Free Cash Flow to Equity framework, analyst forecasts cover the next few years. Beyond that, the cash flows are extrapolated, reaching an estimated free cash flow of roughly $9.2 billion by 2035. These future cash flows are then discounted back to present value using an appropriate required return.

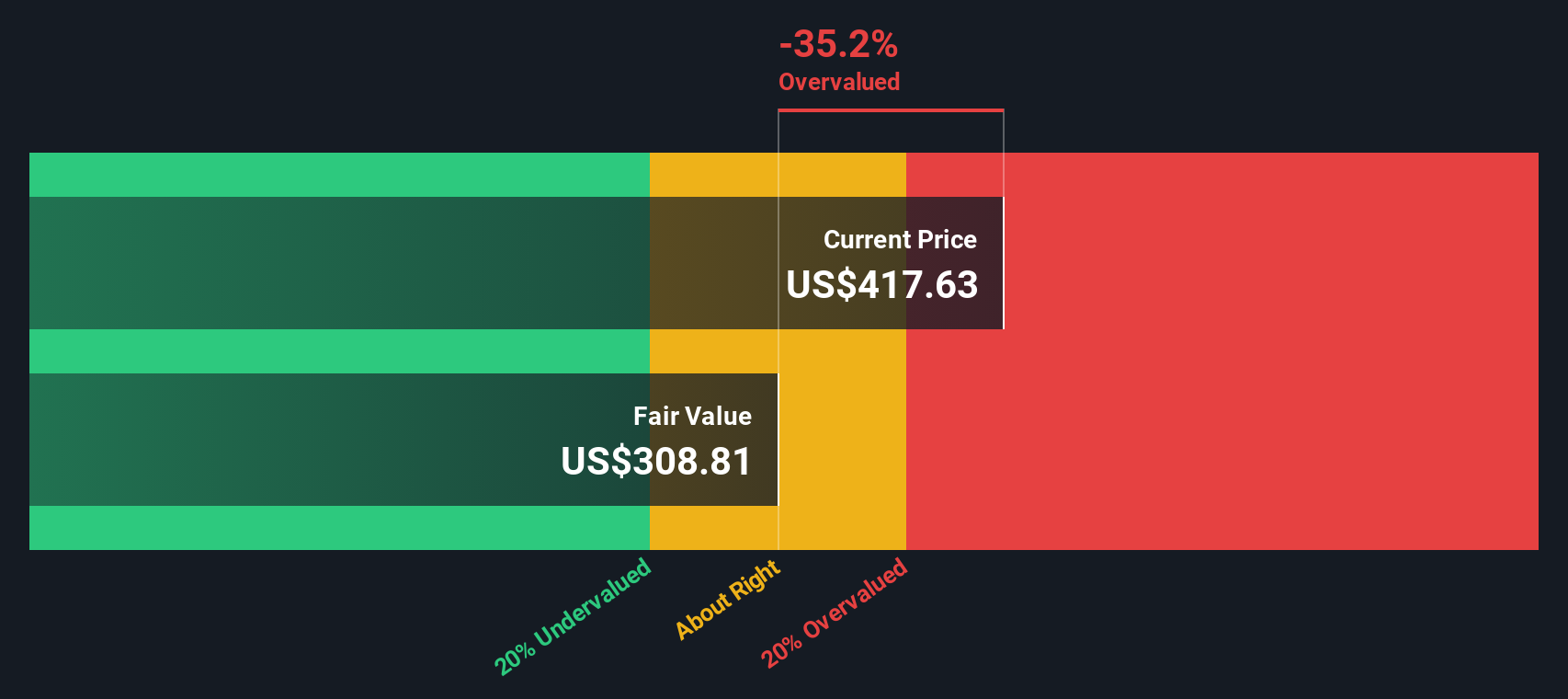

Bringing all those discounted cash flows together gives an estimated intrinsic value of about $438.59 per share. Based on current market pricing, this implies the stock is around 18.0% overvalued, suggesting investors are paying a premium for growth that may already be largely reflected in the price.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests CrowdStrike Holdings may be overvalued by 18.0%. Discover 905 undervalued stocks or create your own screener to find better value opportunities.

Approach 2: CrowdStrike Holdings Price vs Sales

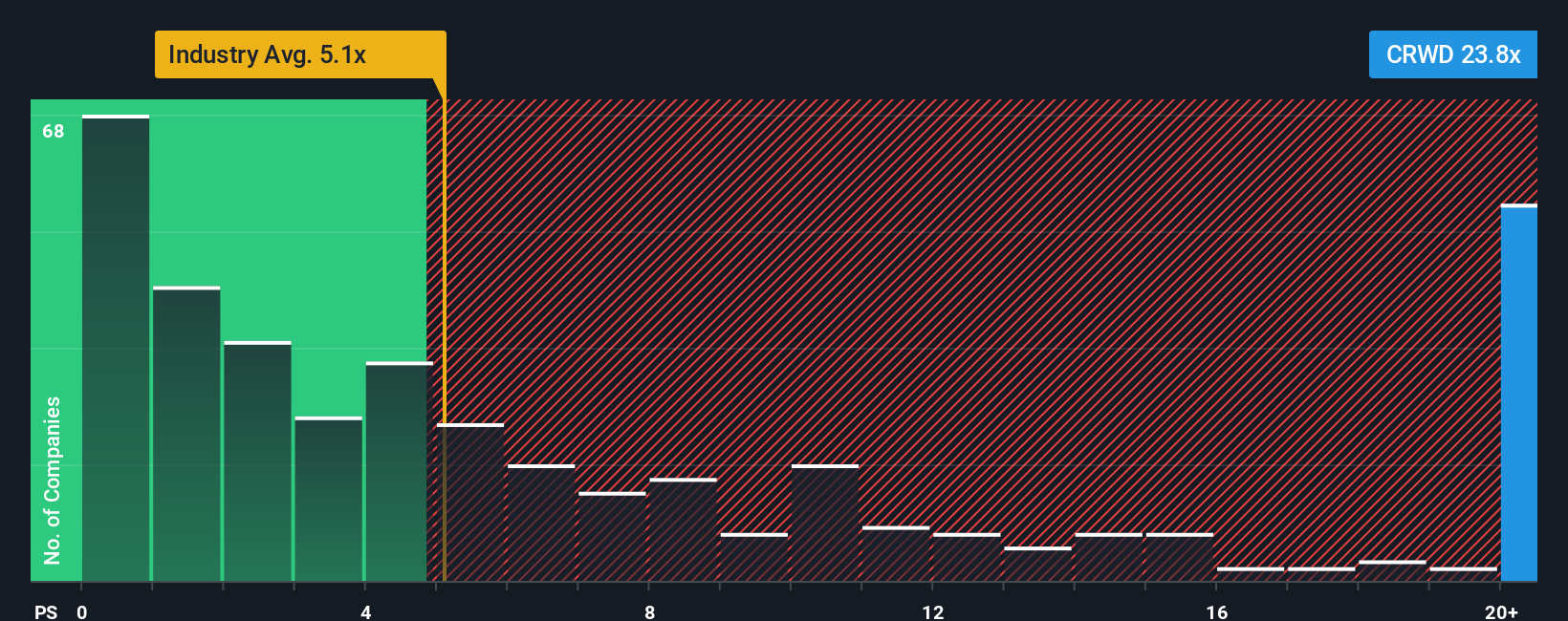

For a fast growing software business like CrowdStrike that is still prioritizing scale, the price to sales multiple is a practical way to compare what investors are paying for each dollar of revenue. It ties directly to the company’s ability to grow its top line, which is the main driver of long term value while margins are still evolving.

In general, higher growth and lower perceived risk justify a richer sales multiple, while slower growth or higher risk warrant a discount. CrowdStrike currently trades on a price to sales ratio of about 28.6x, far above the broader Software industry average of roughly 5.1x and even well ahead of its high growth peer group at around 12.8x.

Simply Wall St’s Fair Ratio framework estimates what a reasonable price to sales multiple should be once you factor in CrowdStrike’s growth outlook, profitability profile, industry, market cap and risk. This bespoke Fair Ratio of 15.8x is more informative than simple peer or industry comparisons because it explicitly adjusts for those fundamentals rather than assuming all software names deserve similar multiples. Against that yardstick, CrowdStrike’s current 28.6x looks stretched and points to a stock that is richly valued for its prospects.

Result: OVERVALUED

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1446 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your CrowdStrike Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to attach your own story about CrowdStrike Holdings to the numbers by linking what you believe about its products, growth, margins and risks to a specific financial forecast and fair value estimate. On Simply Wall St’s Community page, Narratives are an easy, accessible tool used by millions of investors to translate their view of a company into assumptions for future revenue, earnings and margins, then compare the resulting Fair Value to today’s share price to decide whether to buy, hold or sell. Because Narratives are updated dynamically when new information such as earnings releases, product launches or major news hits the market, they help you keep your investment thesis current rather than static. For example, one CrowdStrike Narrative currently implies a fair value around $431 per share while another points closer to $533, neatly illustrating how different investors, looking at the same business, can reach very different but clearly quantified views of what the stock is actually worth.

For CrowdStrike Holdings, however, we will make it really easy for you with previews of two leading CrowdStrike Holdings Narratives:

🐂 CrowdStrike Holdings Bull Case

Fair value: $533.26 per share

Implied undervaluation vs last close: -3.0%

Revenue growth assumption: 21.55%

- Expects AI driven features like Charlotte, Falcon Flex subscriptions and automation tools to deepen customer relationships, support higher pricing and lift margins over time.

- Sees strong momentum from cloud marketplaces and large technology partners, with expanding product breadth driving ARR growth as customers consolidate security tools on Falcon.

- Assumes execution on new modules and acquisitions will outweigh risks from integration, competition and reliance on non GAAP metrics, in line with analyst targets modestly above the current share price.

🐻 CrowdStrike Holdings Bear Case

Fair value: $431.24 per share

Implied overvaluation vs last close: 20.0%

Revenue growth assumption: 18.0%

- Recognizes Falcon as a highly attractive, cloud native subscription platform with strong ARR growth and expanding module adoption, but anchored by a more conservative fair value estimate.

- Highlights solid fundamentals, including a healthy balance sheet and improving returns on equity, while still treating current market expectations as aggressive relative to underlying cash flows.

- Describes the stock as offering roughly 10% annual return at fair value assumptions, indicating that today’s price reflects a richer outlook than this more cautious growth and FCF scenario supports.

Do you think there's more to the story for CrowdStrike Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CRWD

CrowdStrike Holdings

Provides cybersecurity solutions in the United States and internationally.

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Cheap if able to sustain revenue, and a potential bargain if able to turn store openings into revenue growth

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)