Advertisement

- United States

- /

- General Merchandise and Department Stores

- /

- NasdaqGM:DIBS

US$8.00 - That's What Analysts Think 1stdibs.Com, Inc. (NASDAQ:DIBS) Is Worth After These Results

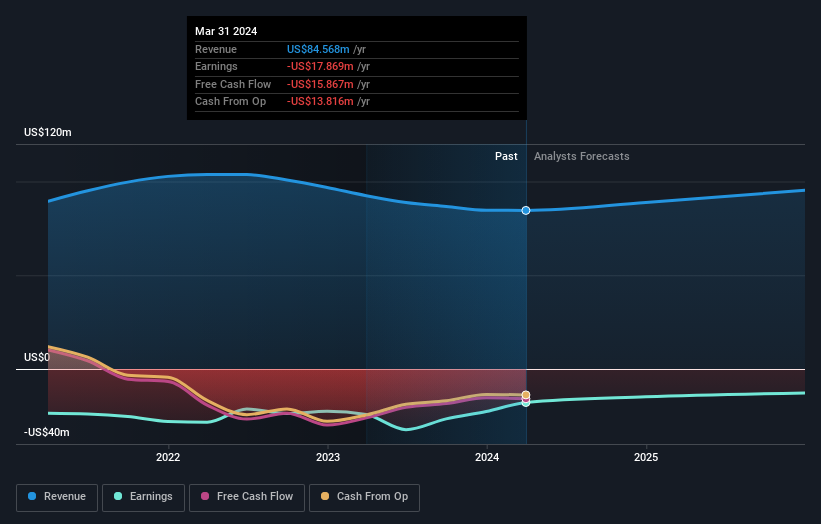

As you might know, 1stdibs.Com, Inc. (NASDAQ:DIBS) just kicked off its latest first-quarter results with some very strong numbers. It looks like a positive result overall, with revenues of US$22m beating forecasts by 3.6%. Statutory losses of US$0.08 per share were 3.6% smaller than the analysts expected, likely helped along by the higher revenues. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

Check out our latest analysis for 1stdibs.Com

After the latest results, the three analysts covering 1stdibs.Com are now predicting revenues of US$88.8m in 2024. If met, this would reflect a credible 5.0% improvement in revenue compared to the last 12 months. Losses are supposed to decline, shrinking 18% from last year to US$0.37. Before this latest report, the consensus had been expecting revenues of US$85.7m and US$0.39 per share in losses. So there seems to have been a moderate uplift in analyst sentiment with the latest consensus release, given the upgrades to both revenue and loss per share forecasts for this year.

The consensus price target rose 33% to US$8.00, with the analysts encouraged by the higher revenue and lower forecast losses for next year.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. One thing stands out from these estimates, which is that 1stdibs.Com is forecast to grow faster in the future than it has in the past, with revenues expected to display 6.7% annualised growth until the end of 2024. If achieved, this would be a much better result than the 4.8% annual decline over the past three years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenue grow 10% per year. Although 1stdibs.Com's revenues are expected to improve, it seems that the analysts are still bearish on the business, forecasting it to grow slower than the broader industry.

The Bottom Line

The most obvious conclusion is that the analysts made no changes to their forecasts for a loss next year. They also upgraded their revenue estimates for next year, even though it is expected to grow slower than the wider industry. We note an upgrade to the price target, suggesting that the analysts believes the intrinsic value of the business is likely to improve over time.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple 1stdibs.Com analysts - going out to 2025, and you can see them free on our platform here.

You still need to take note of risks, for example - 1stdibs.Com has 1 warning sign we think you should be aware of.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGM:DIBS

1stdibs.Com

Operates an online marketplace for luxury design products worldwide.

Flawless balance sheet and overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Giftify ·

Giftify ($GIFT): A Small-Cap Incentives Platform with More ScaleThan Its Valuation Suggests

Fair Value:US$2.561.6% undervalued

41 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on lululemon athletica ·

Quantifying the Transition: Why Lululemon’s Moat Remains Intact

Fair Value:US$161.829.8% undervalued

17 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

TR

tripledub on Alphabet ·

Warren Buffett Just Bet $10 Billion on Google. The Catch? You May Already Be Too Late.

Fair Value:US$23057.4% overvalued

48 followersusers have followed this narrative

1 commentusers have commented on this narrative

12 likesusers have liked this narrative

JO

John_Eric on Veeva Systems ·

AI-Powered Veeva Systems Poised for Solid Growth Amid Regulatory Stability

Fair Value:US$32041.2% undervalued

27 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

SI

Simplicity_Over_Noise on Aurinia Pharmaceuticals ·

Aurinia Pharmaceuticals: Focused Execution in a Narrow but Durable Niche

Fair Value:US$16.290.4% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ST

steffen_4h13a on Alzinova ·

Fair value 7.1B Sek

Fair Value:SEK 8598.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

AndyB72 on NNN REIT ·

NNN - National Retail Properties Inc. | I'm on 75% position and waiting to buy more.

Fair Value:US$46.421.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75030.7% undervalued

84 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5456.3% undervalued

61 followersusers have followed this narrative

3 commentsusers have commented on this narrative

10 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9630.9% undervalued

64 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative