- United States

- /

- Insurance

- /

- NYSE:HCI

Evaluating HCI Group (HCI): Market Penetration and Book Value Drive Fresh Valuation Debate

Reviewed by Simply Wall St

HCI Group (HCI) is turning heads after recent reports underscored the company’s strong market penetration and substantial growth in book value. For investors sorting through a crowded insurance sector, this capital strength stands out, particularly as peers grapple with industry headwinds. The conversation is shifting, with many wondering if HCI's balanced growth profile signals that more upside could be in store for shareholders.

All this buzz follows an already impressive run for HCI. In the past year alone, the stock has jumped 76%, far outperforming both the broader market and its sector. Even after a brief dip in momentum over the past quarter, long-term investors have watched the company post double-digit annual growth in both revenue and net income, along with a 173% return over three years. A string of positive developments, including consistently rising book value and robust capital ratios, has reinforced the sense that investor sentiment is building.

So, after a year of standout gains and strengthening fundamentals, is HCI Group an undervalued opportunity, or is the market already factoring in its future growth?

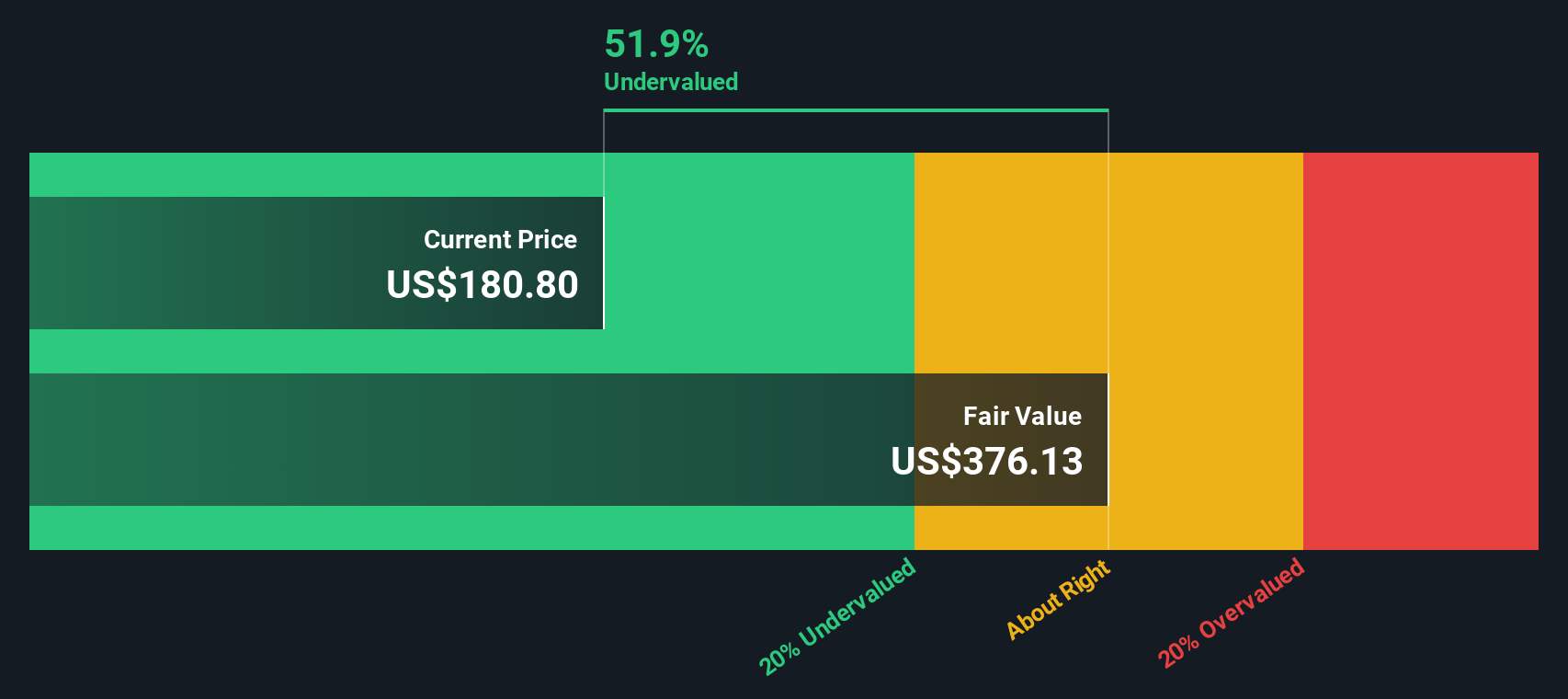

Most Popular Narrative: 17.7% Undervalued

According to community narrative, HCI Group is viewed as notably undervalued right now. Analysts see a sizable gap between the current share price and consensus fair value. This view is influenced by expectations around powerful technology drivers and future business expansion.

"Continued investment in proprietary technology (Exzeo) allows HCI to identify and select profitable policies more efficiently. This results in lower loss ratios and higher retention rates. This technology edge is well positioned to drive further net margin expansion and sustainable earnings growth."

Are you ready to uncover the factors fueling HCI Group’s potential re-rating? One key innovation is taking center stage, combined with a positive outlook for growth and margins. Interested in the main assumptions behind this undervaluation narrative? Explore the numbers and projections that support this perspective.

Result: Fair Value of $202.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, rising reinsurance costs and HCI's reliance on Florida remain potential hurdles that could challenge the company's path to sustained outperformance.

Find out about the key risks to this HCI Group narrative.Another View: Our DCF Model

Taking a different approach, our SWS DCF model analyzes HCI Group’s long-term cash flows and also indicates the stock is undervalued. However, can both methods be correct? The answer ultimately depends on the underlying assumptions.

Look into how the SWS DCF model arrives at its fair value.

Build Your Own HCI Group Narrative

If you are inclined to dig deeper or craft a unique view of HCI Group based on your own analysis, you can do so quickly and easily with the following option: Do it your way.

A great starting point for your HCI Group research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Winning Investment Ideas?

Smart investors stay ahead by exploring more than just a single stock, searching for promising moves across different sectors and trends. Don’t let prime opportunities pass by while others act. Enhance your next investment search with these standout strategies:

- Spot emerging opportunities with penny stocks with strong financials to find financially strong small companies with outsized growth potential before the rest of the market takes notice.

- Accelerate your portfolio with dividend stocks with yields > 3% to target companies offering attractive yields, which can be appealing for those seeking steady income and stability even in uncertain markets.

- Tap into the future by using healthcare AI stocks to uncover innovative businesses at the intersection of artificial intelligence and healthcare, making advances in medical technology and patient care.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if HCI Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NYSE:HCI

HCI Group

Engages in the property and casualty insurance, insurance management, reinsurance, real estate, and information technology businesses in the United States.

Very undervalued with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)