Advertisement

- United States

- /

- Personal Products

- /

- NasdaqCM:NATR

Earnings Miss: Nature's Sunshine Products, Inc. Missed EPS By 38% And Analysts Are Revising Their Forecasts

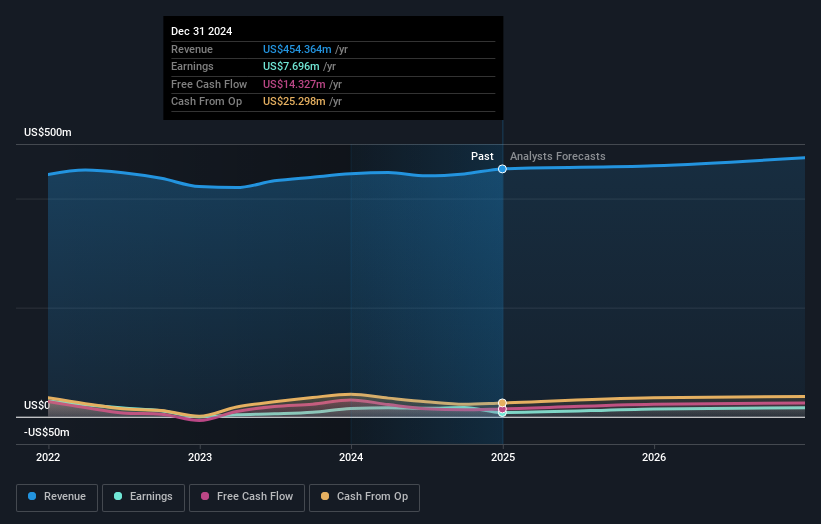

Shareholders might have noticed that Nature's Sunshine Products, Inc. (NASDAQ:NATR) filed its yearly result this time last week. The early response was not positive, with shares down 7.3% to US$13.46 in the past week. Statutory earnings per share fell badly short of expectations, coming in at US$0.40, some 38% below analyst forecasts, although revenues were okay, approximately in line with analyst estimates at US$454m. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

See our latest analysis for Nature's Sunshine Products

Following last week's earnings report, Nature's Sunshine Products' two analysts are forecasting 2025 revenues to be US$460.0m, approximately in line with the last 12 months. Per-share earnings are expected to surge 84% to US$0.77. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$457.3m and earnings per share (EPS) of US$0.81 in 2025. So it looks like there's been a small decline in overall sentiment after the recent results - there's been no major change to revenue estimates, but the analysts did make a small dip in their earnings per share forecasts.

It might be a surprise to learn that the consensus price target was broadly unchanged at US$22.25, with the analysts clearly implying that the forecast decline in earnings is not expected to have much of an impact on valuation.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. We would highlight that Nature's Sunshine Products' revenue growth is expected to slow, with the forecast 1.2% annualised growth rate until the end of 2025 being well below the historical 4.1% p.a. growth over the last five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 3.6% annually. Factoring in the forecast slowdown in growth, it seems obvious that Nature's Sunshine Products is also expected to grow slower than other industry participants.

The Bottom Line

The most important thing to take away is that the analysts downgraded their earnings per share estimates, showing that there has been a clear decline in sentiment following these results. Fortunately, the analysts also reconfirmed their revenue estimates, suggesting that it's tracking in line with expectations. Although our data does suggest that Nature's Sunshine Products' revenue is expected to perform worse than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At least one analyst has provided forecasts out to 2026, which can be seen for free on our platform here.

Even so, be aware that Nature's Sunshine Products is showing 1 warning sign in our investment analysis , you should know about...

Valuation is complex, but we're here to simplify it.

Discover if Nature's Sunshine Products might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:NATR

Nature's Sunshine Products

A natural health and wellness company, manufactures and sells nutritional and personal care products in Asia, Europe, North America, Latin America, and internationally.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|24.5% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|24.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.2% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|97.7% undervalued

RO

Community Contributor