Advertisement

- United States

- /

- Food and Staples Retail

- /

- NYSE:TBBB

3 Prominent Stocks Estimated To Be Trading Below Intrinsic Value By Up To 46.9%

Simply Wall St

Reviewed by Simply Wall St

As the U.S. stock market navigates mixed performance amid rising Treasury yields and a recent credit rating downgrade, investors are keenly observing opportunities that may have been overlooked. In this environment, identifying stocks trading below their intrinsic value can be particularly appealing, as these investments might offer potential upside when market sentiment stabilizes.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Quaker Chemical (NYSE:KWR) | $106.86 | $210.36 | 49.2% |

| Super Group (SGHC) (NYSE:SGHC) | $8.38 | $16.52 | 49.3% |

| Valley National Bancorp (NasdaqGS:VLY) | $9.16 | $18.14 | 49.5% |

| Flowco Holdings (NYSE:FLOC) | $19.08 | $37.91 | 49.7% |

| First Reliance Bancshares (OTCPK:FSRL) | $9.35 | $18.49 | 49.4% |

| Curbline Properties (NYSE:CURB) | $23.74 | $47.17 | 49.7% |

| Carvana (NYSE:CVNA) | $299.89 | $587.44 | 48.9% |

| Constellation Brands (NYSE:STZ) | $195.62 | $385.37 | 49.2% |

| ZEEKR Intelligent Technology Holding (NYSE:ZK) | $29.34 | $58.09 | 49.5% |

| Mobileye Global (NasdaqGS:MBLY) | $15.96 | $31.08 | 48.6% |

We'll examine a selection from our screener results.

DexCom (NasdaqGS:DXCM)

Overview: DexCom, Inc. is a medical device company that specializes in the design, development, and commercialization of continuous glucose monitoring systems both in the United States and internationally, with a market cap of approximately $33.52 billion.

Operations: The company's revenue is primarily derived from its Patient Monitoring Equipment segment, which generated $4.15 billion.

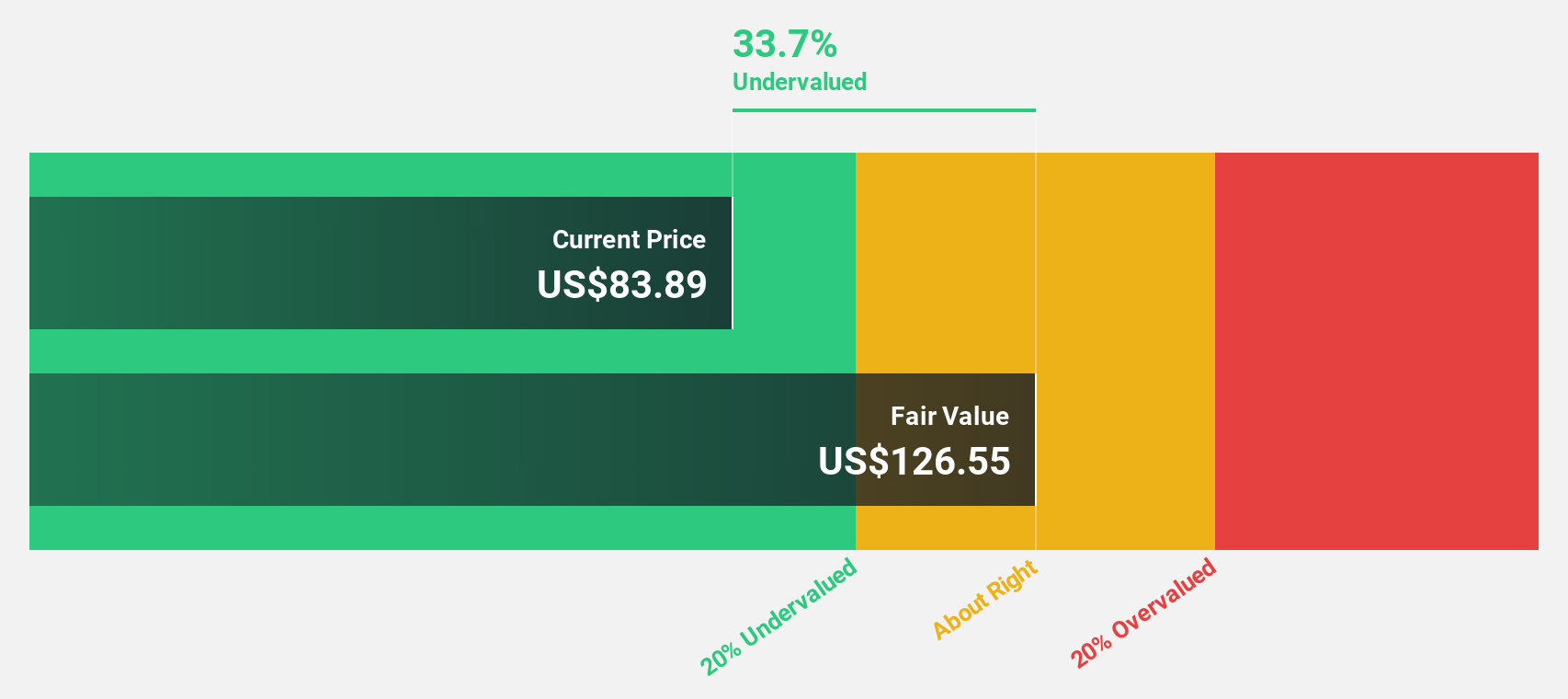

Estimated Discount To Fair Value: 24.6%

DexCom is trading at US$85.48, significantly below its estimated fair value of US$113.33, indicating potential undervaluation based on discounted cash flows. Despite recent executive changes and a share repurchase program up to US$750 million, the company faces challenges such as an FDA warning letter regarding manufacturing processes. However, with revenue expected to grow faster than the U.S. market and earnings forecasted to rise significantly at 23.2% annually, DexCom presents a compelling case for investors focusing on cash flow valuation metrics amidst operational hurdles.

- Our earnings growth report unveils the potential for significant increases in DexCom's future results.

- Dive into the specifics of DexCom here with our thorough financial health report.

Excelerate Energy (NYSE:EE)

Overview: Excelerate Energy, Inc. offers liquefied natural gas (LNG) solutions globally and has a market cap of approximately $3.52 billion.

Operations: The company's revenue is primarily derived from its Utilities - Gas segment, which generated $966.41 million.

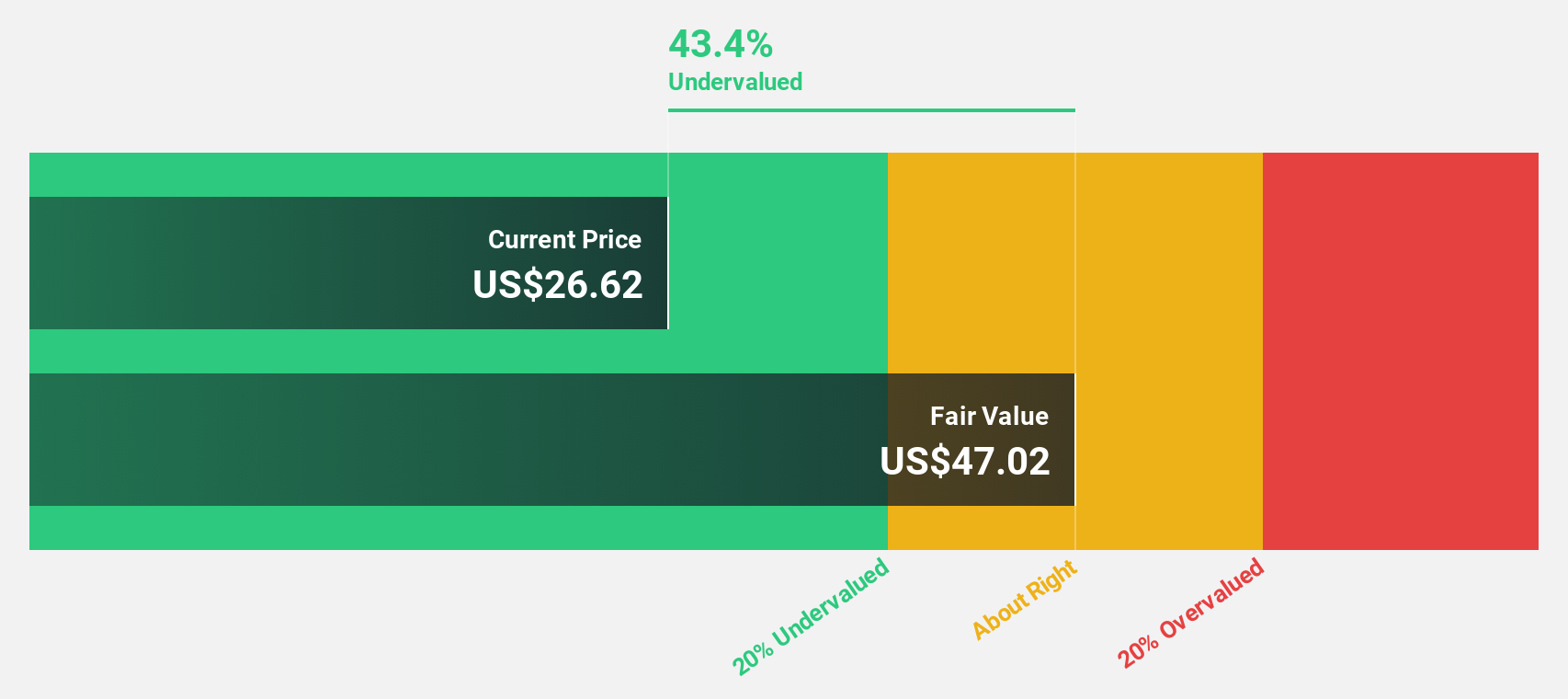

Estimated Discount To Fair Value: 46.9%

Excelerate Energy, trading at US$28.86, is significantly below its estimated fair value of US$54.34, highlighting potential undervaluation based on cash flows. The company reported strong Q1 2025 results with revenue jumping to US$315.09 million from US$200.11 million year-over-year and earnings per share doubling to US$0.48. While earnings are forecasted to grow at 17.9% annually, faster than the U.S market average, a low return on equity forecast of 12.5% could be a concern for investors focusing on profitability metrics amidst its expansion efforts such as M&A activities and strategic partnerships in LNG supply.

- Our comprehensive growth report raises the possibility that Excelerate Energy is poised for substantial financial growth.

- Click to explore a detailed breakdown of our findings in Excelerate Energy's balance sheet health report.

BBB Foods (NYSE:TBBB)

Overview: BBB Foods Inc. operates a chain of grocery retail stores in Mexico and has a market cap of $3.45 billion.

Operations: The company's revenue primarily comes from the sale, acquisition, and distribution of various products and consumer goods, totaling MX$61.89 billion.

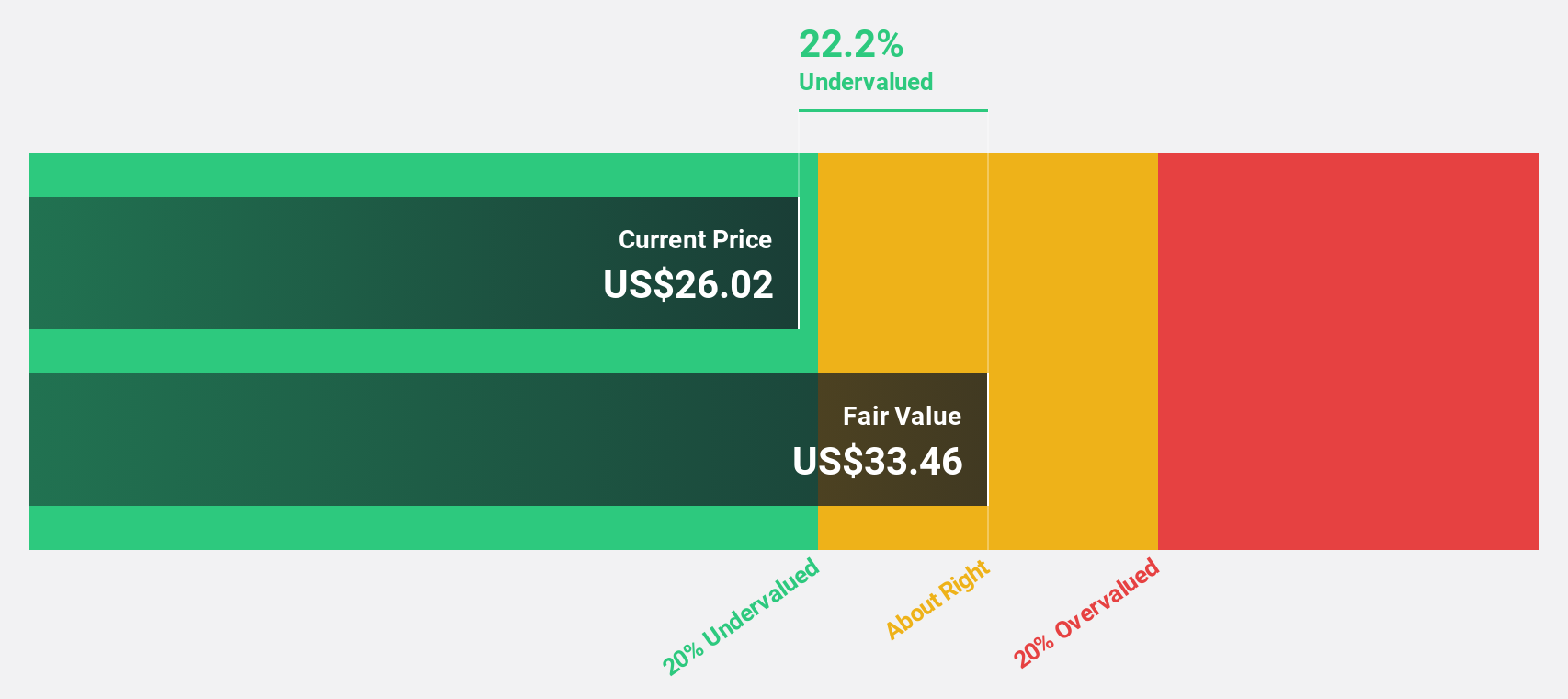

Estimated Discount To Fair Value: 16.7%

BBB Foods, priced at $30.25, trades below its fair value estimate of $36.32, suggesting undervaluation based on cash flows. The company recently turned profitable and forecasts indicate significant earnings growth of 30.2% annually over the next three years, outpacing the U.S market average. Despite a net loss in Q1 2025, revenue surged to MXN 17.13 billion from MXN 12.68 billion year-over-year, reflecting strong operational performance amidst leadership changes.

- Insights from our recent growth report point to a promising forecast for BBB Foods' business outlook.

- Click here to discover the nuances of BBB Foods with our detailed financial health report.

Summing It All Up

- Gain an insight into the universe of 173 Undervalued US Stocks Based On Cash Flows by clicking here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if BBB Foods might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TBBB

BBB Foods

Through its subsidiaries, operates a chain of grocery retail stores in Mexico.

High growth potential and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|33.3% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|23.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|8.5% overvalued

DA

Community Contributor