- United States

- /

- Consumer Finance

- /

- NasdaqGS:NAVI

Assessing Navient’s Valuation After Recent Regulatory Headlines and Modest Share Price Rebound

Reviewed by Bailey Pemberton

- If you are wondering whether Navient is quietly turning into a value opportunity or just another value trap, you are not alone. That is exactly what we are going to unpack.

- Despite being down about 10.9% over the last year and 13.1% over three years, the stock has recently shown some life, with a 3.1% gain over the past week and an 8.9% move over the last month. This hints that market sentiment might be shifting.

- Recent headlines around federal student loan policies, shifting repayment rules, and ongoing debates about loan forgiveness have kept Navient in the spotlight, as investors try to gauge how regulatory changes could reshape its long term cash flows. At the same time, broader financial sector volatility has made investors more sensitive to balance sheet strength and business model resilience for lenders like Navient.

- On our framework, Navient scores just 2 out of 6 on undervaluation checks. This suggests there are pockets of value but also areas where the price looks less compelling. Next we will walk through those different valuation lenses, before finishing with a more holistic way to think about what the stock is really worth.

Navient scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Navient Excess Returns Analysis

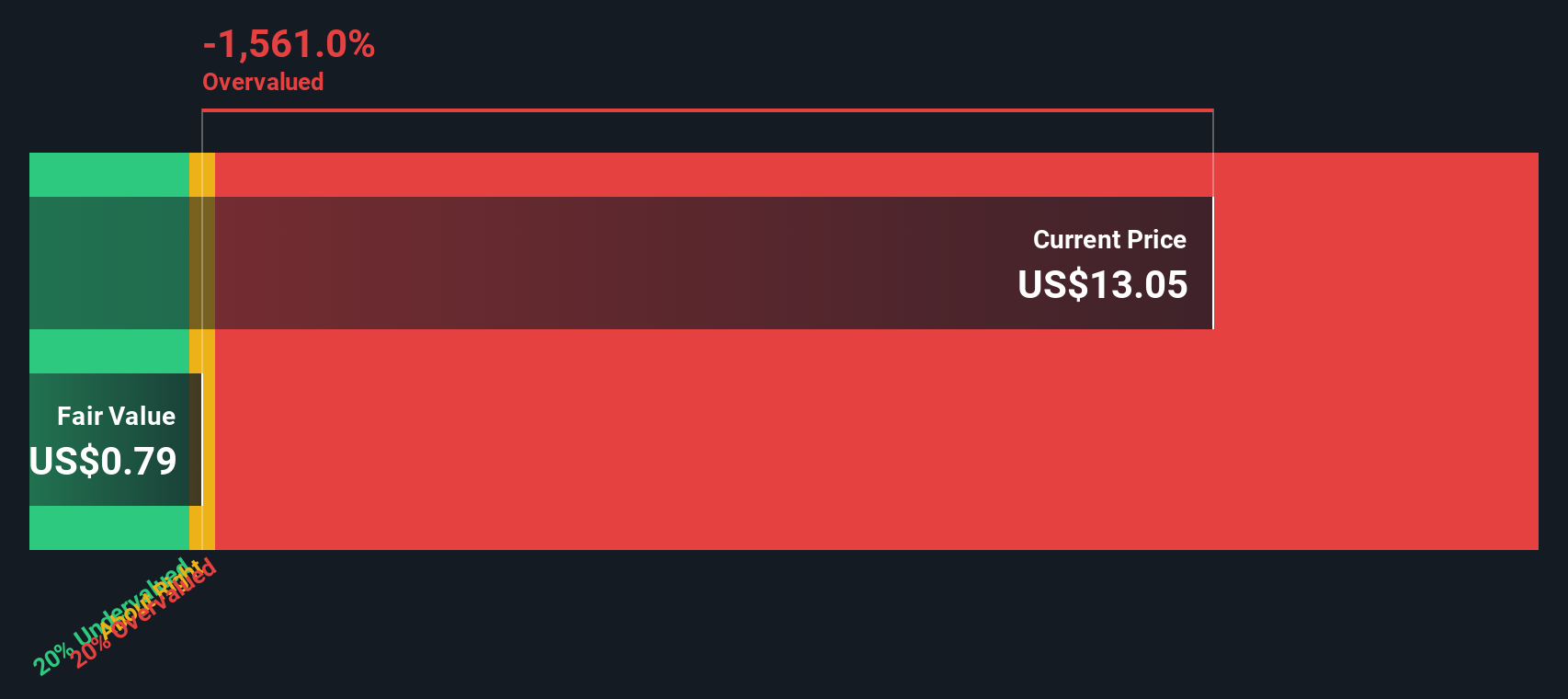

The Excess Returns model looks at how much profit Navient can generate on its equity above, or in this case below, the return that investors require. Instead of focusing on cash flows, it asks whether future returns on equity will justify the company’s current book value.

Navient has an average return on equity of just 3.53%, with a stable earnings estimate of $0.94 per share supported by four analysts. That is set against a cost of equity of $3.33 per share, implying an excess return of roughly negative $2.39 per share, meaning projected profitability does not clear the hurdle rate investors demand. Even though book value is relatively robust at $25.01 per share and expected to edge up to about $26.66 per share, the model suggests that incremental value creation will be weak.

When these excess returns are projected forward and discounted, the Excess Returns model implies Navient is about 1,527.5% overvalued relative to its current share price, which points to a large gap between the market’s optimism and the company’s economic earning power.

Result: OVERVALUED

Our Excess Returns analysis suggests Navient may be overvalued by 1527.5%. Discover 908 undervalued stocks or create your own screener to find better value opportunities.

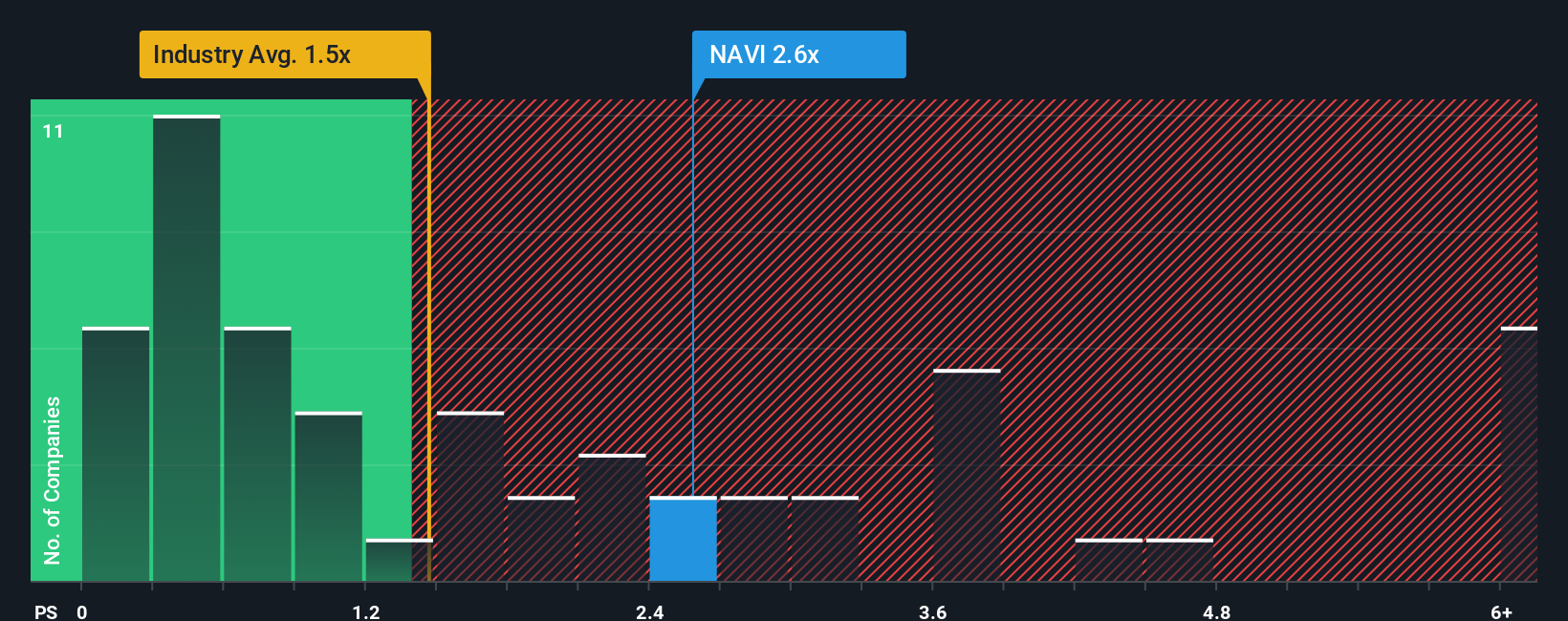

Approach 2: Navient Price vs Sales

For many profitable financial companies, the price to sales ratio is a useful yardstick because revenue tends to be more stable than earnings, which can swing around with credit costs, provisions, and one off items. It helps investors see how much the market is paying for each dollar of ongoing business activity.

In general, higher expected growth and lower perceived risk justify a richer multiple. Slower growth or elevated risk usually pull a “normal” or “fair” price to sales down. Against that backdrop, Navient currently trades on a price to sales ratio of about 2.82x. That is well above the Consumer Finance industry average of roughly 1.70x, but far below the broader peer group average near 13.72x, highlighting how wide the valuation range can be in this space.

Simply Wall St’s Fair Ratio for Navient, at 2.86x, is designed to cut through that noise by estimating the multiple the stock should trade on given its specific growth profile, profit margins, risk factors, industry, and size. Because this company specific Fair Ratio is very close to the actual 2.82x multiple, the stock looks reasonably priced rather than clearly cheap or expensive.

Result: ABOUT RIGHT

PS ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1446 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Navient Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, a simple way to connect your view of Navient’s story with the numbers by turning your expectations for its future revenue, earnings, and margins into a financial forecast, linking that forecast to a Fair Value, and then comparing that to today’s share price to decide whether to buy or sell. Narratives on Simply Wall St, available to millions of investors via the Community page, are easy to use and update dynamically as new news or earnings emerge, so your Fair Value view is not static but evolves with the business. For Navient, one investor might build a bullish Narrative around faster graduate loan growth, improving margins near 40%, and a Fair Value above the current analyst high of 18 dollars. In contrast, a more cautious investor could focus on regulatory risk, credit losses, and slower growth, leading to a Fair Value closer to the 10 dollar bear case. Narratives allow you to see, compare, and refine these perspectives in one place.

Do you think there's more to the story for Navient? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Navient might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:NAVI

Navient

Provides technology-enabled education finance and business processing solutions for education, health care, and government clients in the United States.

Reasonable growth potential average dividend payer.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)