- United States

- /

- Insurance

- /

- NasdaqGS:PLMR

US Value Stocks Trading Below Estimated Worth In November 2024

Reviewed by Simply Wall St

As the U.S. stock market shows signs of recovery, with the S&P 500 and Nasdaq rebounding from recent declines, investors are keenly observing opportunities that may arise in this fluctuating environment. In such a climate, identifying undervalued stocks becomes crucial for those looking to capitalize on potential discrepancies between a company's intrinsic value and its current market price.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| First National (NasdaqCM:FXNC) | $23.30 | $46.25 | 49.6% |

| Capital Bancorp (NasdaqGS:CBNK) | $27.37 | $53.44 | 48.8% |

| West Bancorporation (NasdaqGS:WTBA) | $23.58 | $46.82 | 49.6% |

| Business First Bancshares (NasdaqGS:BFST) | $28.12 | $55.07 | 48.9% |

| Five Star Bancorp (NasdaqGS:FSBC) | $32.35 | $63.87 | 49.4% |

| Afya (NasdaqGS:AFYA) | $16.43 | $31.50 | 47.8% |

| Datadog (NasdaqGS:DDOG) | $125.97 | $243.25 | 48.2% |

| Advanced Energy Industries (NasdaqGS:AEIS) | $109.84 | $219.25 | 49.9% |

| WEX (NYSE:WEX) | $178.01 | $345.87 | 48.5% |

| Marcus & Millichap (NYSE:MMI) | $40.84 | $78.74 | 48.1% |

Here we highlight a subset of our preferred stocks from the screener.

Atlanticus Holdings (NasdaqGS:ATLC)

Overview: Atlanticus Holdings Corporation is a financial technology company that offers credit and related financial services in the United States, with a market cap of approximately $716.01 million.

Operations: The company generates revenue through its segments in Auto Finance, which accounts for $28.63 million, and Credit as a Service, contributing $345.46 million.

Estimated Discount To Fair Value: 19.4%

Atlanticus Holdings is trading at US$49.59, below its estimated fair value of US$61.51, indicating it may be undervalued based on cash flows. Despite a high debt level and recent insider selling, the company's earnings grew by 7.5% last year and are forecast to grow significantly at 28.9% annually over the next three years, outpacing the market average of 15.3%. Revenue growth is also expected to exceed market rates substantially.

- Our growth report here indicates Atlanticus Holdings may be poised for an improving outlook.

- Get an in-depth perspective on Atlanticus Holdings' balance sheet by reading our health report here.

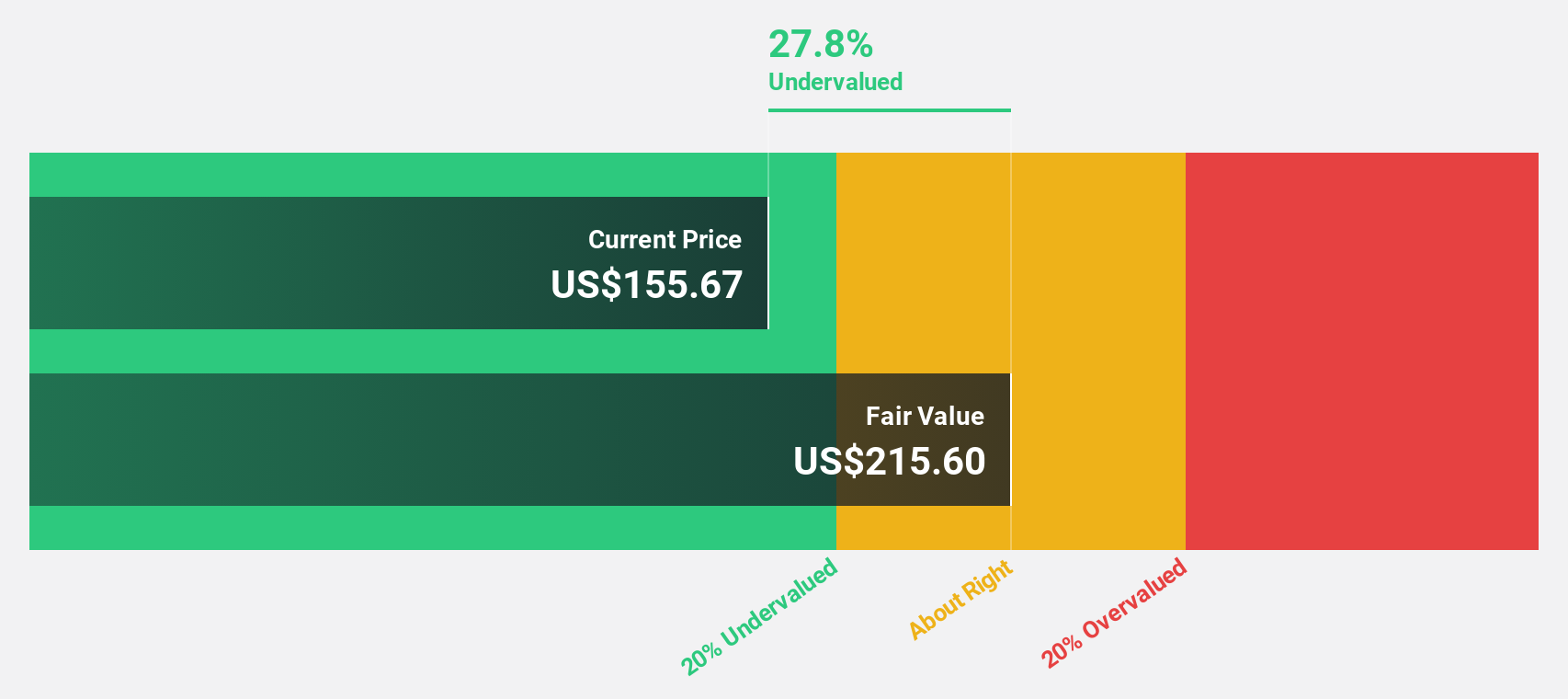

Palomar Holdings (NasdaqGS:PLMR)

Overview: Palomar Holdings, Inc. is a specialty insurance company offering property and casualty insurance to residential and business clients in the United States, with a market cap of approximately $2.74 billion.

Operations: The company's revenue primarily comes from its Earthquake, Wind, and Flood Insurance Products segment, which generated $503.50 million.

Estimated Discount To Fair Value: 35.8%

Palomar Holdings is trading at US$108.48, significantly below its estimated fair value of US$168.9, suggesting undervaluation based on cash flows. Despite recent insider selling and shareholder dilution, Palomar's earnings grew by 50.6% last year and are projected to increase by 23.4% annually, surpassing the market average of 15.3%. The company's revenue growth is also expected to exceed market rates substantially, supported by strategic executive appointments in key divisions.

- Our expertly prepared growth report on Palomar Holdings implies its future financial outlook may be stronger than recent results.

- Take a closer look at Palomar Holdings' balance sheet health here in our report.

Hess Midstream (NYSE:HESM)

Overview: Hess Midstream LP owns, develops, operates, and acquires midstream assets to provide fee-based services to Hess and third-party customers in the United States, with a market cap of $7.80 billion.

Operations: The company's revenue is derived from three main segments: Gathering ($780.40 million), Processing and Storage ($555 million), and Terminaling and Export ($120.70 million).

Estimated Discount To Fair Value: 31.8%

Hess Midstream is trading at US$35.9, significantly below its estimated fair value of US$52.64, indicating undervaluation based on cash flows. The company reported robust earnings growth of 84.8% over the past year and forecasts a 54% annual profit increase, outpacing the market average of 15.3%. Recent strategic moves include seeking bolt-on acquisitions supported by US$1.25 billion in financial flexibility, despite a high debt level and unsustainable dividend coverage from earnings or free cash flow.

- In light of our recent growth report, it seems possible that Hess Midstream's financial performance will exceed current levels.

- Dive into the specifics of Hess Midstream here with our thorough financial health report.

Taking Advantage

- Take a closer look at our Undervalued US Stocks Based On Cash Flows list of 197 companies by clicking here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PLMR

Palomar Holdings

A specialty insurance company, provides property and casualty insurance to individuals and businesses in the United States.

Solid track record with excellent balance sheet.