- United States

- /

- Hospitality

- /

- NYSE:CAVA

Cava (CAVA): Valuation Check After Fresh Buy Ratings and Ongoing Expansion Challenges

Reviewed by Simply Wall St

CAVA Group (CAVA) is back in focus after several Wall Street firms reiterated Buy ratings, even as the chain works through softer same store sales and squeezed margins tied to rapid expansion.

See our latest analysis for CAVA Group.

All of this comes against a backdrop where CAVA’s share price has slid sharply year to date, with a steep negative total shareholder return over the last year, even as recent 1 month share price gains hint that sentiment may be stabilizing rather than breaking down further.

If CAVA’s story has you watching the broader restaurant and consumer space, it could be a good moment to widen the lens and explore fast growing stocks with high insider ownership.

With the stock down sharply this year but still trading at a hefty implied growth premium, the key question now is simple: are investors staring at a mispriced Mediterranean growth story, or is the market already baking in tomorrow’s expansion?

Most Popular Narrative Narrative: 24% Undervalued

With the narrative fair value of $67.89 sitting above CAVA Group’s last close at $51.92, the story hinges on whether its growth runway truly merits a premium.

The analysts have a consensus price target of $92.214 for CAVA Group based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $125.0, and the most bearish reporting a price target of just $72.0.

Want to see why a maturing profit profile still commands a sky high earnings multiple, even as margins compress and growth expectations cool? The full narrative breaks down the bold revenue ramp, shrinking profitability, and surprisingly rich future earnings multiple that together underpin this fair value call.

Result: Fair Value of $67.89 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, slowing same restaurant sales and the risk of over expansion into saturated markets could quickly undermine the bullish long term growth narrative.

Find out about the key risks to this CAVA Group narrative.

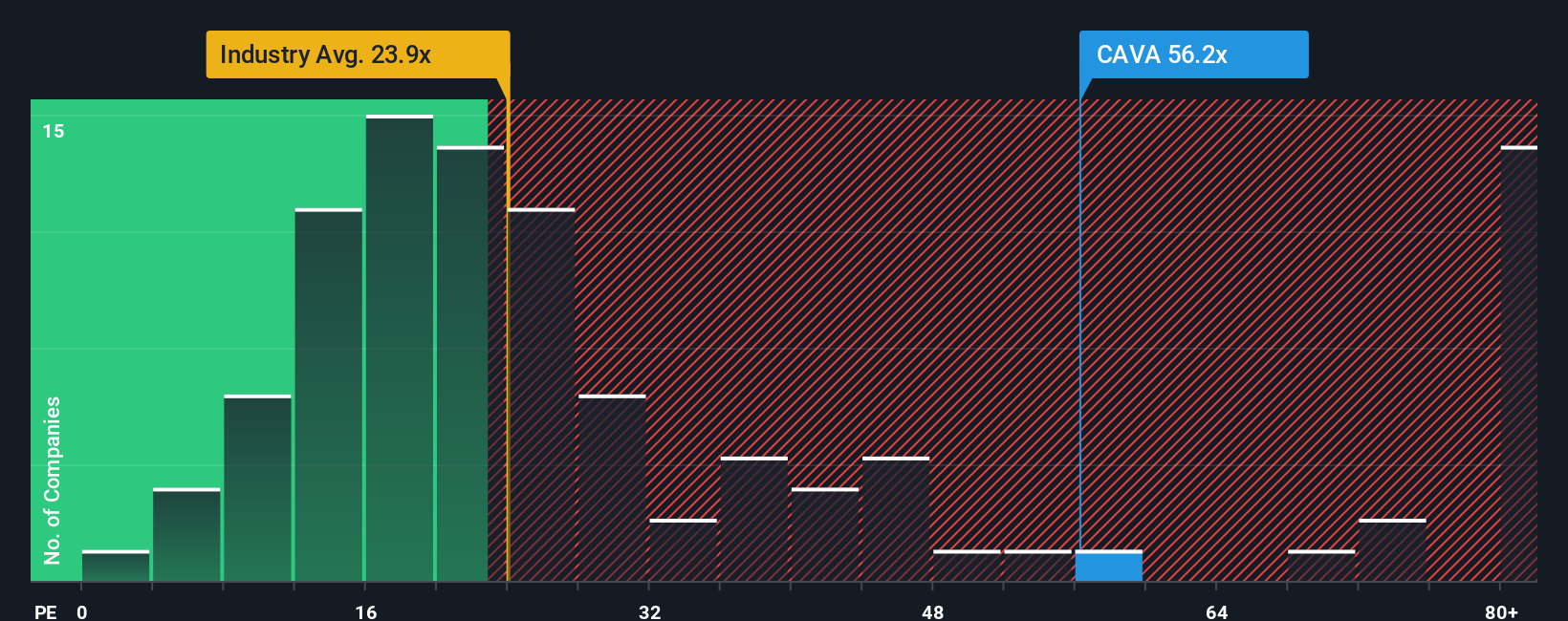

Another View, Market Multiple Sends a Harsher Message

While the narrative fair value suggests upside, CAVA’s current price to earnings of 43.8 times stands far above both the US Hospitality average of 23.1 times and its own fair ratio of 15.9 times. This spread implies investors could face real downside if sentiment normalizes.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own CAVA Group Narrative

If you see the story differently or want to test your own assumptions against the numbers, build a personalized view in just minutes: Do it your way.

A great starting point for your CAVA Group research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Ready for more high conviction ideas?

Before you move on, lock in your next opportunity by using the Simply Wall St Screener to surface focused, data driven ideas that match your strategy.

- Capture potentially mispriced opportunities early by running through these 903 undervalued stocks based on cash flows that may offer strong upside based on their cash flow prospects.

- Ride powerful innovation trends by scanning these 26 AI penny stocks positioned at the forefront of artificial intelligence breakthroughs and adoption.

- Strengthen your income stream by reviewing these 13 dividend stocks with yields > 3% that balance yield with sustainable business foundations.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CAVA

CAVA Group

Owns and operates a chain of restaurants under the CAVA brand in the United States.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)