- United States

- /

- Luxury

- /

- NYSE:ONON

On Holding (NYSE:ONON) Valuation Check After Recent Rebound in Share Price

Reviewed by Simply Wall St

On Holding (NYSE:ONON) has been catching traders attention after a strong month, with the stock climbing about 13% even as its year to date performance remains in the red. That divergence sets up an interesting reset in expectations.

See our latest analysis for On Holding.

That recent 12.7% one-month share price return looks more like a rebound than a breakout, given the share price is still down 13.7% year to date. At the same time, the three-year total shareholder return of 192.5% shows the longer-term growth story is still firmly intact and suggests momentum may be stabilising rather than accelerating at the current 47.79 dollar level.

If On Holding has reminded you how quickly sentiment can shift in growth names, it might be worth scanning fast growing stocks with high insider ownership for other under the radar opportunities with strong backers.

The key question now is whether that pullback, combined with double digit growth and a near 30 percent discount to analyst targets, signals undervaluation or if the market is already factoring in the next leg of expansion.

Most Popular Narrative Narrative: 22.2% Undervalued

With On Holding last closing at 47.79 dollars against a narrative fair value just above 61 dollars, the valuation story leans clearly in favor of upside if its growth path holds.

The acceleration in DTC (Direct to Consumer) and e commerce channels, with DTC reaching new highs (41.1% of sales in Q2 and up 54% YoY), gives On more control over brand, pricing, and customer data while increasing gross and EBITDA margins, an operational catalyst likely to further expand profitability as DTC continues its mix shift.

Want to see why this story backs rapid earnings expansion, richer margins and a still demanding future multiple, all at a higher discount rate? The growth, profitability and valuation puzzle only really clicks when you see how its future revenue curve, margin lift and earnings power are stitched together across the next several years.

Result: Fair Value of $61.40 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, sustained premium pricing and aggressive global expansion could squeeze margins if consumer demand cools or if new regions and categories scale more slowly than expected.

Find out about the key risks to this On Holding narrative.

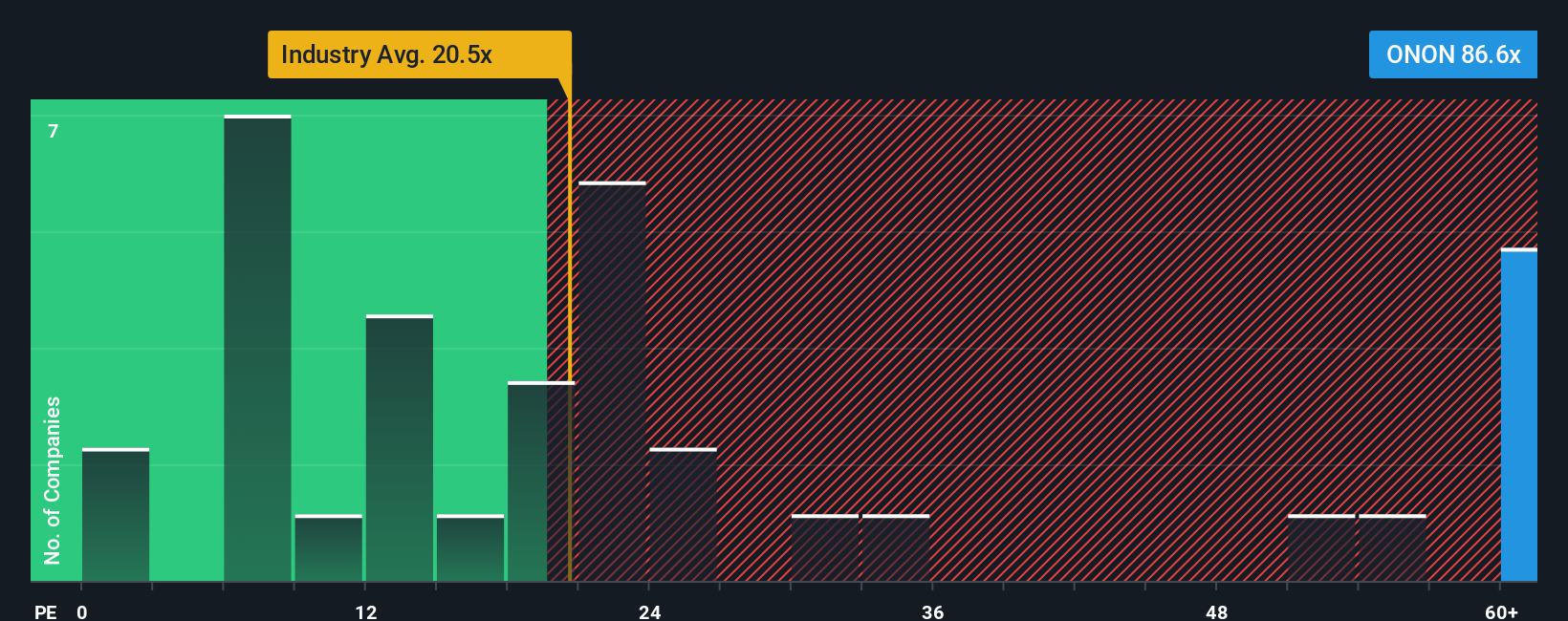

Another View On Valuation

While the narrative fair value suggests upside, the earnings multiple tells a tougher story. On Holding trades around 57.7 times earnings, more than double the Luxury industry at 22.4 times and well above a 28.9 times fair ratio. This raises the risk of a sharp rerating if growth stumbles.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own On Holding Narrative

If you are not convinced by this take or would rather rely on your own analysis, you can build a complete view in minutes: Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding On Holding.

Looking for more investment ideas?

Before markets move on without you, use the Simply Wall St screener to uncover fresh, data driven opportunities that match your strategy, not the crowd’s.

- Capitalize on mispriced quality by scanning these 909 undervalued stocks based on cash flows where strong cash flows and solid fundamentals may still be trading at a meaningful discount.

- Accelerate your growth focus by targeting innovation leaders through these 26 AI penny stocks positioned at the heart of the next wave of intelligent automation.

- Explore potential income streams by reviewing these 13 dividend stocks with yields > 3% that combine dividend yields with balance sheets built to sustain payouts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ONON

On Holding

Engages in the development and distribution of sports products worldwide.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)