- United States

- /

- Capital Markets

- /

- NYSE:EVR

3 Stocks Estimated To Be Trading At Discounts Of Up To 47%

Reviewed by Simply Wall St

As the U.S. equities market works to extend its rebound rally, with the S&P 500 and Nasdaq showing slight gains, investors remain cautious amid ongoing concerns about tariffs and economic uncertainty. In this environment, identifying undervalued stocks can be a strategic move for investors looking to capitalize on potential discounts in the market.

Top 10 Undervalued Stocks Based On Cash Flows In The United States

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Provident Financial Services (NYSE:PFS) | $17.39 | $34.68 | 49.8% |

| Dime Community Bancshares (NasdaqGS:DCOM) | $28.66 | $56.79 | 49.5% |

| ACNB (NasdaqCM:ACNB) | $42.07 | $82.45 | 49% |

| KBR (NYSE:KBR) | $51.34 | $101.08 | 49.2% |

| Smurfit Westrock (NYSE:SW) | $45.02 | $89.93 | 49.9% |

| Midland States Bancorp (NasdaqGS:MSBI) | $18.10 | $35.67 | 49.3% |

| HealthEquity (NasdaqGS:HQY) | $90.32 | $179.14 | 49.6% |

| Ligand Pharmaceuticals (NasdaqGM:LGND) | $111.67 | $220.76 | 49.4% |

| Constellium (NYSE:CSTM) | $11.38 | $22.45 | 49.3% |

| Albemarle (NYSE:ALB) | $77.55 | $152.79 | 49.2% |

Let's dive into some prime choices out of the screener.

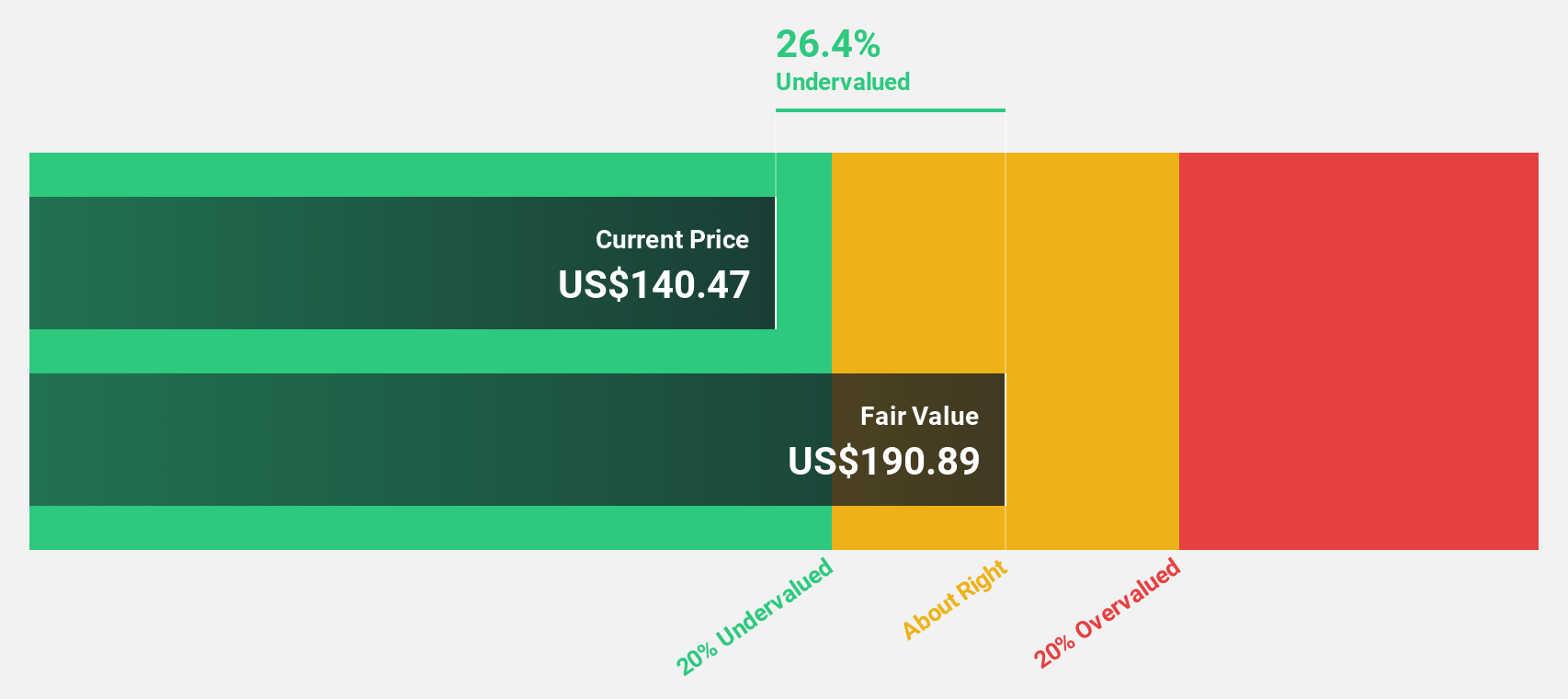

Rocket Lab USA (NasdaqCM:RKLB)

Overview: Rocket Lab USA, Inc. is a space company offering launch services and space systems solutions globally, with a market cap of approximately $8.59 billion.

Operations: The company generates revenue through its Space Systems segment, which accounts for $310.84 million, and its Launch Services segment, contributing $125.38 million.

Estimated Discount To Fair Value: 47%

Rocket Lab USA is trading at US$20.21, significantly below its estimated fair value of US$38.17, suggesting it may be undervalued based on cash flows. Despite a volatile share price and recent insider selling, the company has demonstrated robust revenue growth with a forecasted annual increase of 28.3%, outpacing the broader market's 8.4%. Recent successful launches and strategic contracts bolster its position in the space industry, potentially enhancing future profitability prospects.

- Our comprehensive growth report raises the possibility that Rocket Lab USA is poised for substantial financial growth.

- Take a closer look at Rocket Lab USA's balance sheet health here in our report.

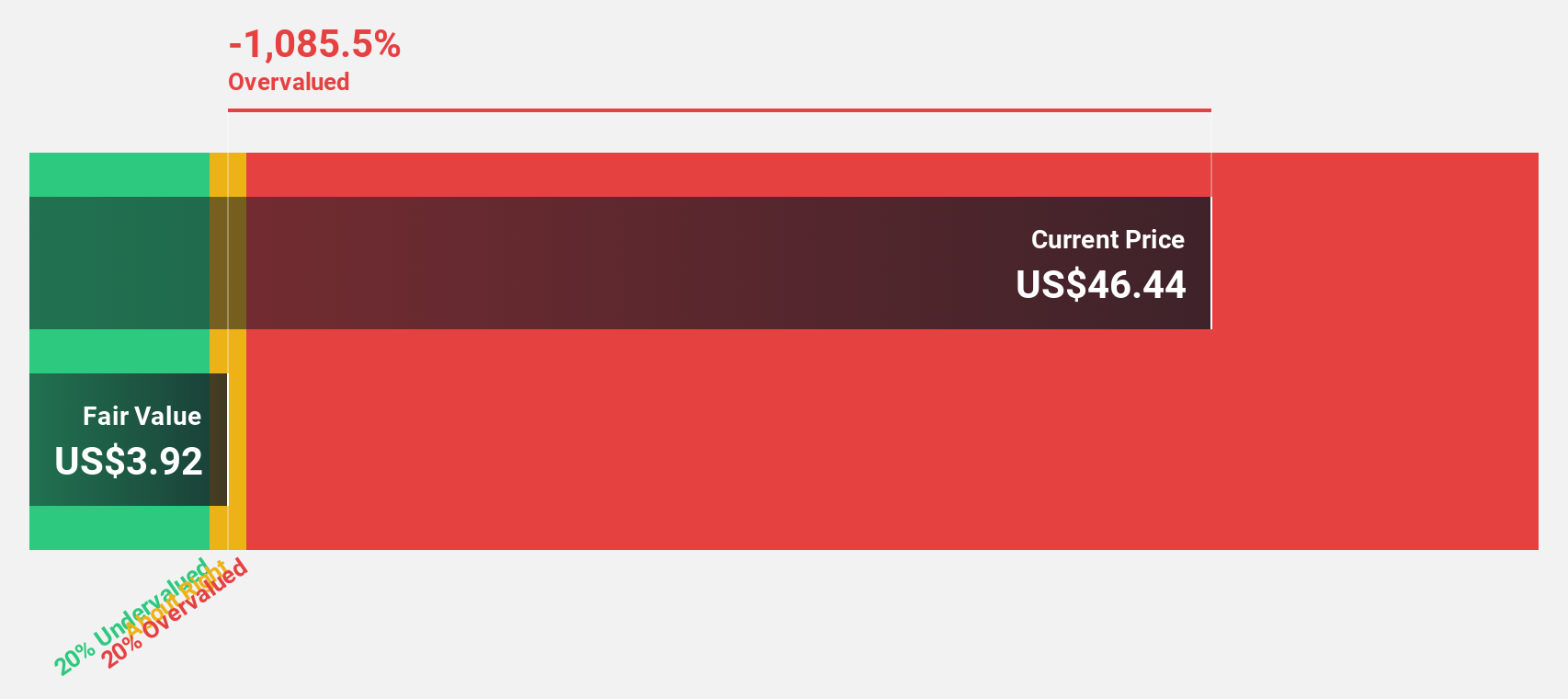

Evercore (NYSE:EVR)

Overview: Evercore Inc. is an independent investment banking firm providing advisory services across the Americas, Europe, Middle East, Africa, and Asia-Pacific with a market cap of approximately $8.58 billion.

Operations: The company's revenue is primarily derived from Investment Banking & Equities, which accounts for $2.90 billion, while Investment Management contributes $81.10 million.

Estimated Discount To Fair Value: 23.3%

Evercore is currently trading at US$216.84, which is 23.3% below its estimated fair value of US$282.53, highlighting potential undervaluation based on cash flows. The firm has reported strong earnings growth of 48.1% over the past year and is expected to continue with an annual profit increase of 22.3%, surpassing the market average of 13.9%. Recent strategic hires and advisory roles in key sectors may further support its financial performance trajectory.

- In light of our recent growth report, it seems possible that Evercore's financial performance will exceed current levels.

- Dive into the specifics of Evercore here with our thorough financial health report.

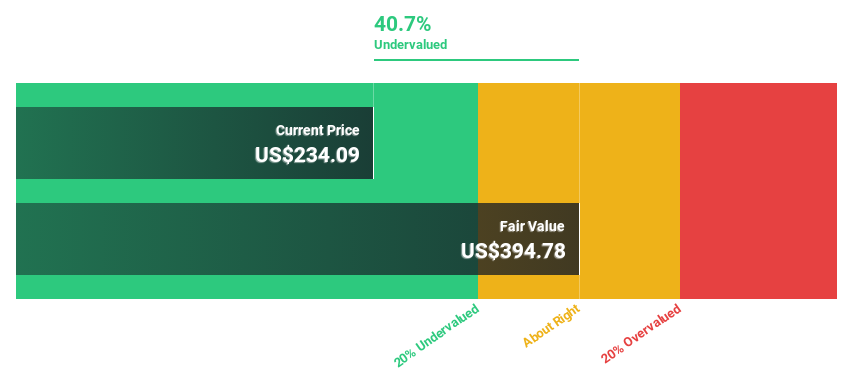

Owens Corning (NYSE:OC)

Overview: Owens Corning is a company that offers residential and commercial building products across the United States, Europe, the Asia Pacific, and internationally, with a market cap of approximately $12.36 billion.

Operations: The company's revenue is primarily derived from its Roofing segment at $4.05 billion, followed by Insulation at $3.69 billion, Composites at $2.12 billion, and Doors contributing $1.45 billion.

Estimated Discount To Fair Value: 43.6%

Owens Corning is trading at US$151.18, significantly below its estimated fair value of US$268.22, indicating potential undervaluation based on cash flows. Despite a recent decline in profit margins and insider selling, the company's earnings are projected to grow substantially at 26.7% annually, outpacing the market average. Recent debt financing increases liquidity with an additional US$500 million revolving commitment, while strategic expansions in shingle manufacturing may bolster future revenue streams despite current slower growth forecasts.

- Insights from our recent growth report point to a promising forecast for Owens Corning's business outlook.

- Click here and access our complete balance sheet health report to understand the dynamics of Owens Corning.

Seize The Opportunity

- Take a closer look at our Undervalued US Stocks Based On Cash Flows list of 195 companies by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

If you're looking to trade Evercore, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Evercore might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:EVR

Evercore

Operates as an independent investment banking firm in the Americas, Europe, Middle East, Africa, and Asia-Pacific.

High growth potential with solid track record and pays a dividend.

Similar Companies

Market Insights

Community Narratives