Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:FRO

3 Insider-Favored Growth Stocks To Watch

Simply Wall St

Reviewed by Simply Wall St

Over the last 7 days, the United States market has dropped 2.6%, yet over the past year, it has risen by 9.1%, with earnings forecasted to grow by 14% annually. In such a fluctuating environment, growth companies with high insider ownership can be particularly appealing as they often indicate strong confidence from those closest to the business in its future potential.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Atour Lifestyle Holdings (NasdaqGS:ATAT) | 22.7% | 24.2% |

| Super Micro Computer (NasdaqGS:SMCI) | 25.2% | 39.1% |

| Duolingo (NasdaqGS:DUOL) | 14.3% | 39.9% |

| FTC Solar (NasdaqCM:FTCI) | 27.9% | 61.8% |

| AST SpaceMobile (NasdaqGS:ASTS) | 13.4% | 67.1% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 12.1% | 65.1% |

| Astera Labs (NasdaqGS:ALAB) | 15.2% | 44.3% |

| Enovix (NasdaqGS:ENVX) | 12.1% | 58.4% |

| Upstart Holdings (NasdaqGS:UPST) | 12.6% | 102.6% |

| BBB Foods (NYSE:TBBB) | 16.2% | 30.2% |

Here's a peek at a few of the choices from the screener.

AerSale (NasdaqCM:ASLE)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: AerSale Corporation supplies aftermarket commercial aircraft, engines, and parts to a global clientele including airlines, leasing companies, OEMs, government and defense contractors, and MRO service providers with a market cap of $274.61 million.

Operations: The company's revenue segments include Tech Ops - MRO Services at $103.28 million, Tech Ops - Product Sales at $21.61 million, Asset Management Solutions - Engine at $162.66 million, and Asset Management Solutions - Aircraft at $32.76 million.

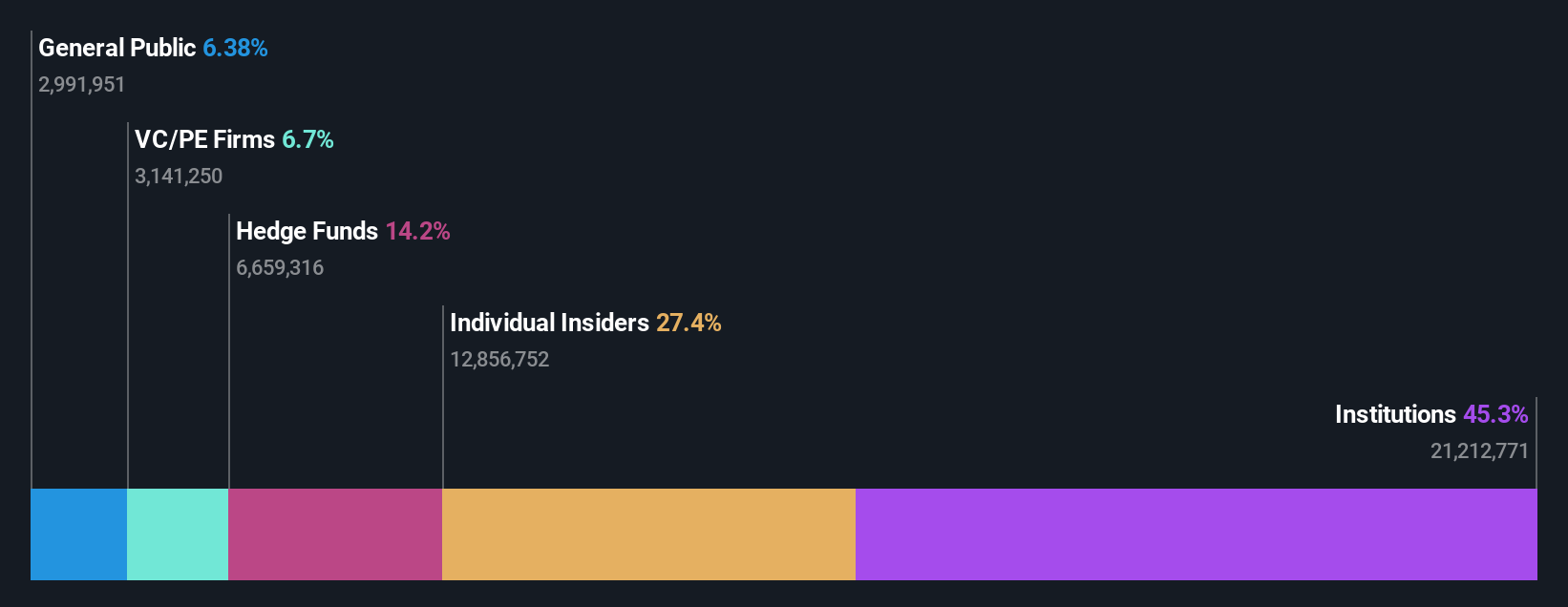

Insider Ownership: 27.4%

Earnings Growth Forecast: 140.9% p.a.

AerSale demonstrates potential as a growth company with high insider ownership, despite recent financial challenges. The company's revenue is forecast to grow at 13.4% annually, outpacing the broader US market. Although it reported a net loss of US$5.28 million in Q1 2025, AerSale is expected to achieve profitability within three years and offers good relative value compared to peers. Recent board changes may enhance strategic oversight and operational efficiency moving forward.

- Get an in-depth perspective on AerSale's performance by reading our analyst estimates report here.

- Upon reviewing our latest valuation report, AerSale's share price might be too pessimistic.

Frontline (NYSE:FRO)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Frontline plc is a shipping company that owns and operates oil and product tankers globally, with a market cap of approximately $4.08 billion.

Operations: The company generates revenue primarily through its tanker operations, amounting to approximately $1.90 billion.

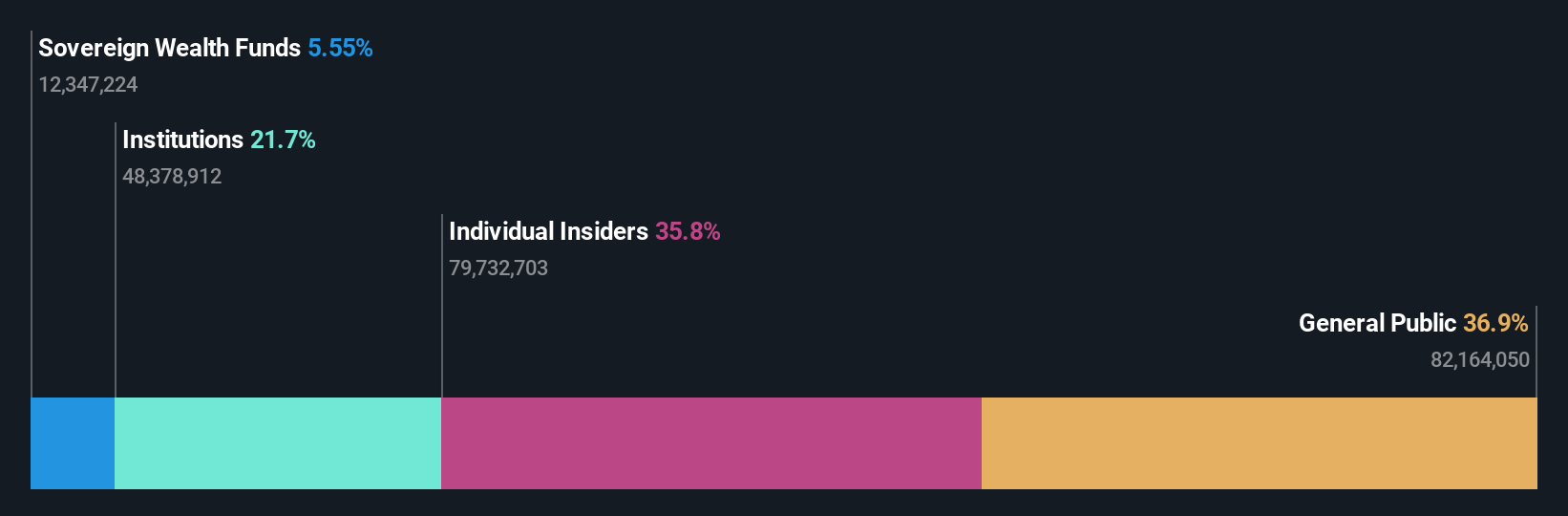

Insider Ownership: 35.8%

Earnings Growth Forecast: 26.6% p.a.

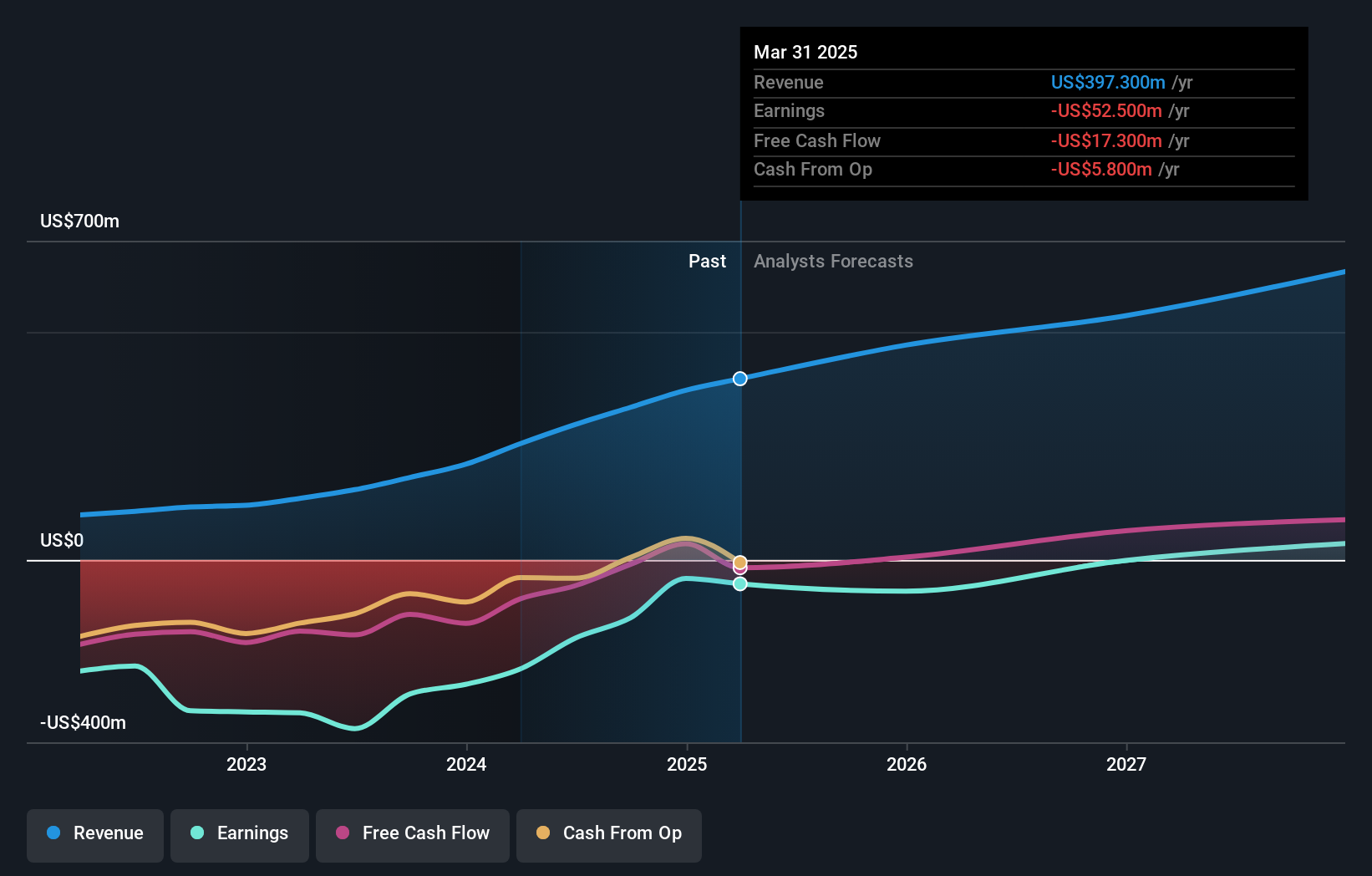

Frontline's insider ownership aligns with its potential for growth, though recent earnings show a decline in revenue to US$428.09 million and net income to US$33.29 million compared to the previous year. Despite this, its forecasted annual earnings growth of 26.6% surpasses the US market average, indicating strong future prospects. Trading below fair value and analyst price targets suggests good relative value, yet unstable dividends and high interest payments warrant caution.

- Click here and access our complete growth analysis report to understand the dynamics of Frontline.

- The analysis detailed in our Frontline valuation report hints at an deflated share price compared to its estimated value.

Hippo Holdings (NYSE:HIPO)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Hippo Holdings Inc. offers property and casualty insurance products to individuals and businesses in the United States, with a market cap of approximately $562 million.

Operations: Hippo Holdings Inc.'s revenue segments include $48.50 million from Services, $118 million from Insurance-As-A-Service, and $243.20 million from the Hippo Home Insurance Program.

Insider Ownership: 12.6%

Earnings Growth Forecast: 83.8% p.a.

Hippo Holdings demonstrates potential for growth with its forecasted revenue increase of 13.6% annually, surpassing the US market average. Despite a net loss of US$47.7 million in Q1 2025, the company aims to achieve profitability by late 2025, supported by raised revenue guidance to US$465 million for the year. The resignation of co-founder Assaf Wand from the board may impact strategic direction, while recent leadership changes could influence future performance positively.

- Take a closer look at Hippo Holdings' potential here in our earnings growth report.

- Our valuation report here indicates Hippo Holdings may be overvalued.

Next Steps

- Get an in-depth perspective on all 193 Fast Growing US Companies With High Insider Ownership by using our screener here.

- Looking For Alternative Opportunities? Uncover the next big thing with financially sound penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:FRO

Frontline

A shipping company, engages in the ownership and operation of oil and product tankers worldwide.

Very undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.7% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|28.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor