- United States

- /

- Banks

- /

- NYSE:BY

Three Top Undervalued Small Caps With Insider Buying In US

Reviewed by Simply Wall St

The United States market has been flat in the last week but is up 23% over the past year, with earnings forecasted to grow by 15% annually. In this environment, identifying stocks that are potentially undervalued can offer opportunities for investors looking to capitalize on growth prospects, especially when there is notable insider buying activity.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| McEwen Mining | 3.8x | 2.0x | 47.20% | ★★★★★☆ |

| OptimizeRx | NA | 1.2x | 37.42% | ★★★★★☆ |

| German American Bancorp | 14.5x | 4.8x | 43.95% | ★★★★☆☆ |

| Quanex Building Products | 31.8x | 0.8x | 36.74% | ★★★★☆☆ |

| Arrow Financial | 15.3x | 3.4x | 37.75% | ★★★☆☆☆ |

| First United | 13.1x | 3.5x | 30.22% | ★★★☆☆☆ |

| West Bancorporation | 15.8x | 4.8x | 38.81% | ★★★☆☆☆ |

| Limbach Holdings | 40.3x | 2.0x | 41.10% | ★★★☆☆☆ |

| ChromaDex | 283.5x | 4.6x | 30.78% | ★★★☆☆☆ |

| Franklin Financial Services | 14.9x | 2.4x | 22.15% | ★★★☆☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

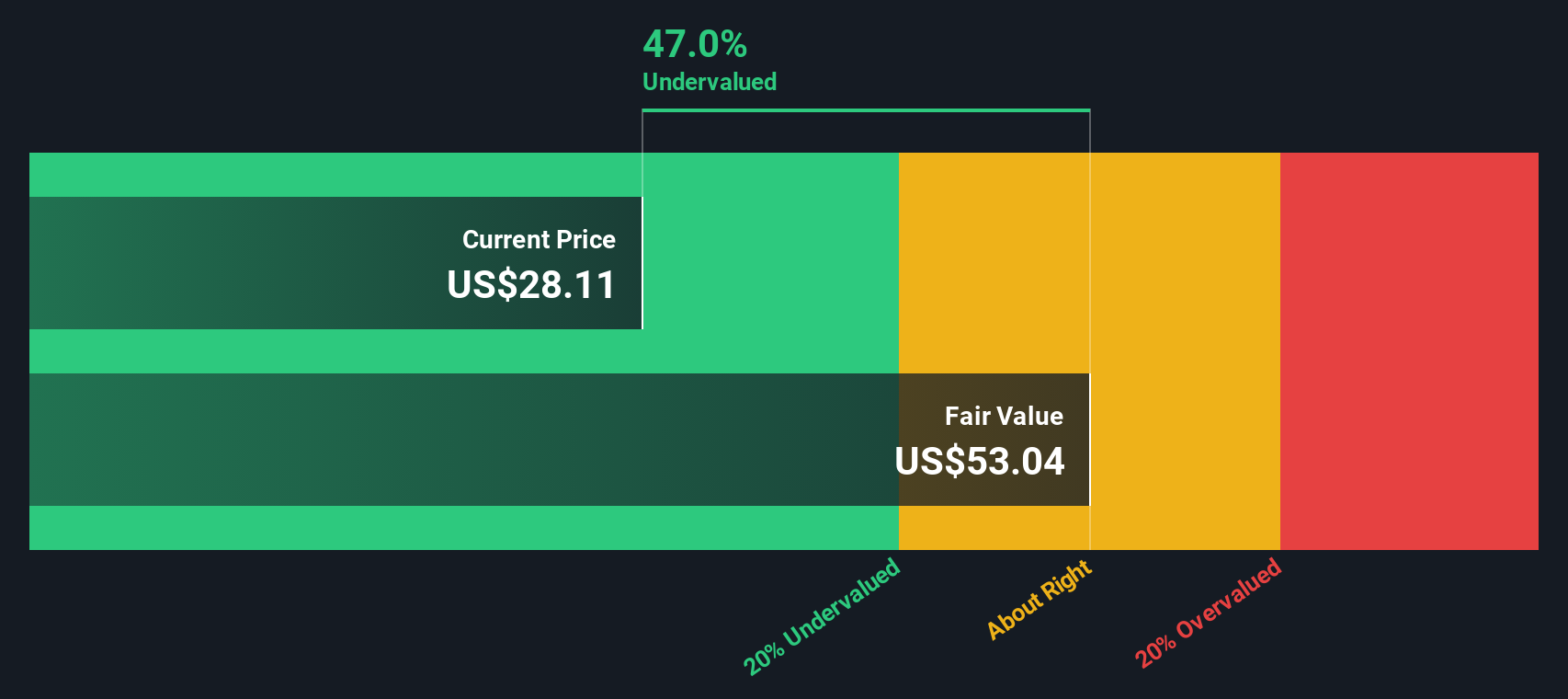

Midland States Bancorp (NasdaqGS:MSBI)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Midland States Bancorp is a diversified financial holding company that provides a range of banking and related financial services to individuals, businesses, and governmental entities, with a market cap of approximately $0.46 billion.

Operations: Midland States Bancorp generates revenue primarily through its operations, with gross profit margins consistently at 100% over the observed periods. Operating expenses are a significant cost factor, with general and administrative expenses frequently comprising a substantial portion of these costs. The company's net income margin has shown variability, reaching as high as 30.32% in some quarters but also experiencing negative figures in recent reports.

PE: -19.3x

Midland States Bancorp, a small company in the financial sector, is gaining attention for its potential growth and insider confidence. Despite a high bad loans ratio of 2.7%, earnings are projected to grow 90% annually. Insider confidence is evident with recent share purchases, though no buybacks occurred from October to December 2024. The firm declared dividends on both preferred and common stock in February 2025, indicating stability amidst challenges like significant net charge-offs last quarter (US$102 million).

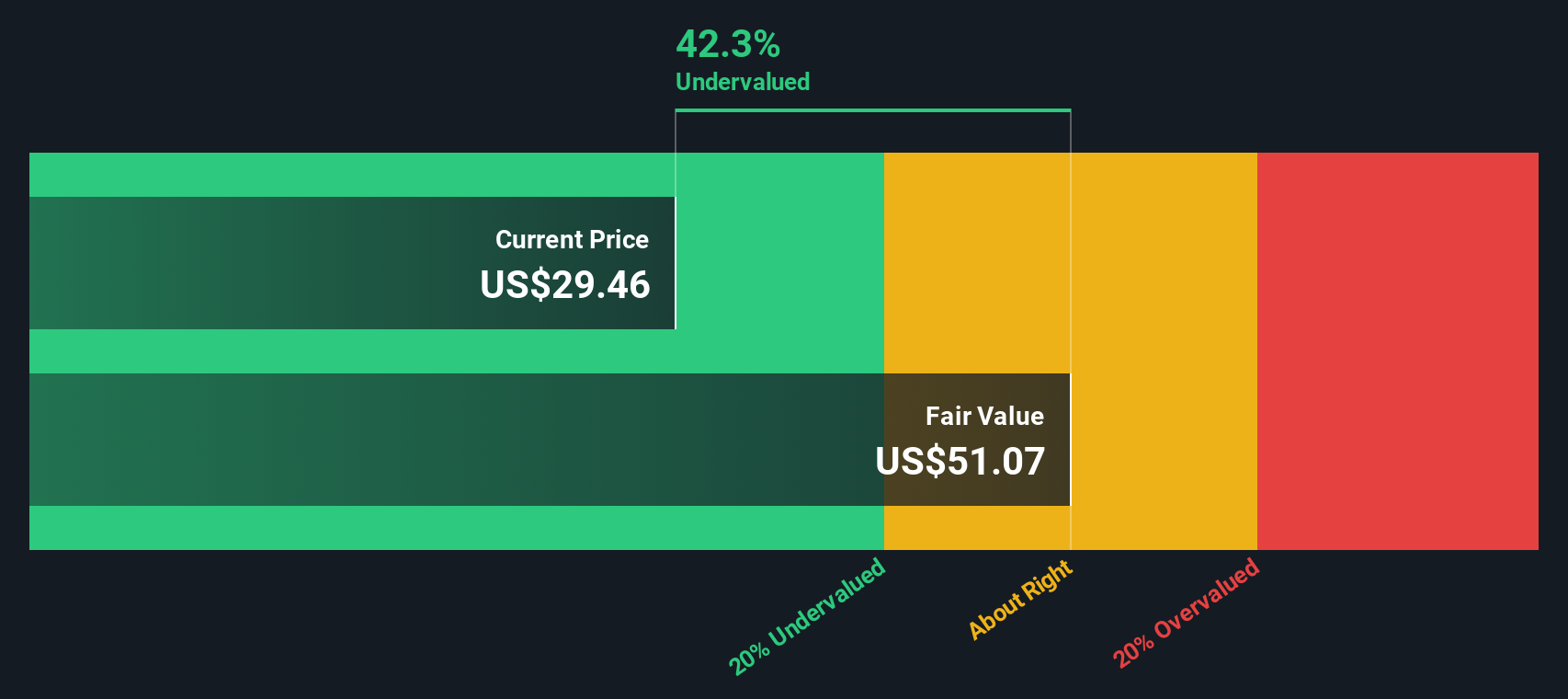

Univest Financial (NasdaqGS:UVSP)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Univest Financial is a financial services company that provides banking, insurance, and investment solutions primarily in the United States, with a market capitalization of approximately $0.74 billion.

Operations: UVSP primarily generates revenue through its operations with a consistent gross profit margin of 100.00% over the periods analyzed. The company incurs significant operating expenses, with general and administrative expenses being a major component, reaching $162.58 million in the latest period. Net income margin has shown variability, peaking at 34.66% and most recently recorded at 25.89%.

PE: 12.0x

Univest Financial, a smaller player in the financial sector, has recently shown signs of being undervalued. Their net income rose to US$75.93 million for 2024 from US$71.1 million in 2023, with basic earnings per share increasing to US$2.6 from US$2.42. Insider confidence is evident as they have been buying shares over the past months, signaling potential value recognition within the company itself. The company also completed a share buyback program totaling nearly 10% of outstanding shares since its inception in 2013, reflecting management's belief in its intrinsic value and future prospects amidst steady earnings growth forecasts at around 3% annually.

- Delve into the full analysis valuation report here for a deeper understanding of Univest Financial.

Evaluate Univest Financial's historical performance by accessing our past performance report.

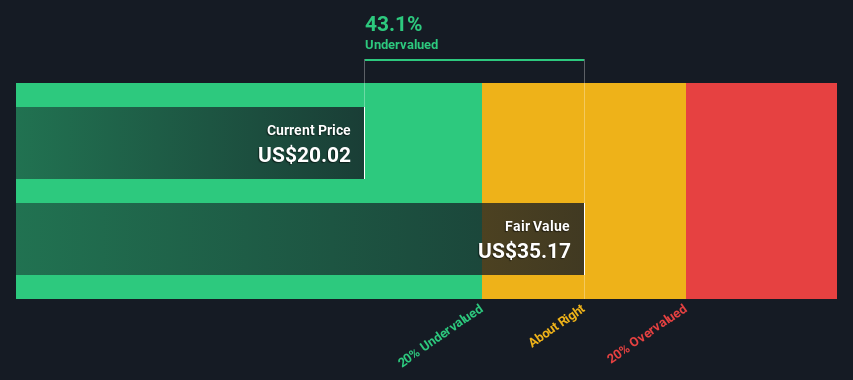

Byline Bancorp (NYSE:BY)

Simply Wall St Value Rating: ★★★★★☆

Overview: Byline Bancorp operates as a bank holding company providing a range of banking products and services, with a market cap of approximately $0.82 billion.

Operations: Byline Bancorp's revenue primarily comes from its banking operations, with a recent figure of $379.86 million. The company consistently achieves a gross profit margin of 100%, indicating that all reported revenue translates directly into gross profit. Operating expenses are substantial, with general and administrative expenses being the largest component, reaching $189.12 million in the latest period.

PE: 11.1x

Byline Bancorp, a financial services company, is gaining attention in the investment community due to its recent insider confidence. Over the past quarter, insiders have increased their holdings, indicating belief in the company's potential. The firm announced a share buyback program for up to 1.25 million shares through December 2025, suggesting management's commitment to enhancing shareholder value. With new leadership under Brian F. Doran as Executive Vice President and General Counsel since January 21, Byline is poised for strategic growth and improved governance within its sector.

- Take a closer look at Byline Bancorp's potential here in our valuation report.

Review our historical performance report to gain insights into Byline Bancorp's's past performance.

Summing It All Up

- Click here to access our complete index of 56 Undervalued US Small Caps With Insider Buying.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Byline Bancorp might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:BY

Byline Bancorp

Operates as the bank holding company for Byline Bank that provides various banking products and services for small and medium sized businesses, commercial real estate and financial sponsors, and consumers in the United States.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Community Narratives