- United States

- /

- Banks

- /

- NasdaqGS:TFSL

TFS Financial (TFSL): Examining the Valuation Behind Its Recent Momentum

Reviewed by Simply Wall St

If you have been watching TFS Financial (TFSL) lately, you might be wondering what is behind its latest move and what it means for your portfolio. Although there has been no specific headline or event setting the stock in motion this week, the shift in price action is catching the attention of those looking for clues about where the market sees TFSL going next. Sometimes, these quieter stretches offer investors a chance to dig deeper into what is driving value under the surface.

Looking at the bigger picture, TFSL has quietly posted a 15% increase over the past year, outpacing the broader banking sector in that timeframe. Short-term traders have experienced both ups and downs, but the past month saw a strong 8% gain, even as volatility remained in the mix. Beyond price swings, TFS Financial has reported steady revenue and net income growth on an annual basis, which may hint at potential momentum beneath recent price moves.

With the stock trending higher this year, investors may now be wondering whether TFSL is offering real value for buyers or if the market has already priced in the bank’s future earnings power.

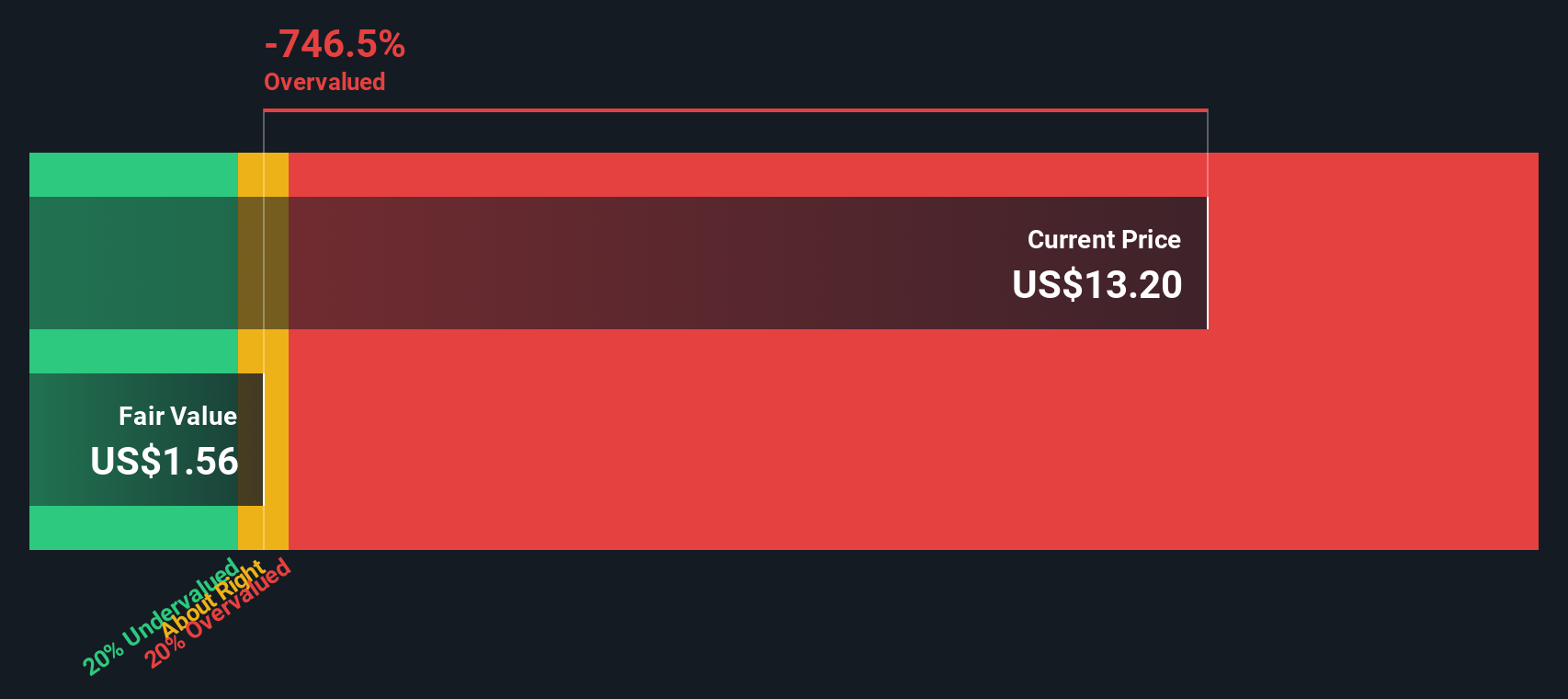

Price-to-Earnings of 46.7x: Is it justified?

Based on the price-to-earnings (P/E) ratio, TFS Financial’s stock currently appears expensive compared to both its industry peers and the broader banking sector.

The P/E ratio compares a company's share price to its per-share earnings, serving as a measure of how much investors are willing to pay for each dollar of profit. For banks like TFSL, this metric is particularly relevant, as it reflects how the market values current and anticipated profit growth relative to competitors.

With TFSL trading at a 46.7x earnings multiple, far above the industry average, the market is pricing in a significant premium despite below-average growth forecasts and profit margins that trail sector peers. This high valuation suggests that investors may be overestimating near-term growth potential or are willing to pay up for other perceived strengths. These are factors worth deeper examination for prospective shareholders.

Result: Fair Value of $1.56 (OVERVALUED)

See our latest analysis for TFS Financial.However, any shift in revenue growth or unexpected changes in earnings could quickly challenge the market's confidence in TFSL's current premium valuation.

Find out about the key risks to this TFS Financial narrative.Another View: SWS DCF Model

While the market price seems high compared to sector averages, our DCF model takes a different approach and comes to a similar conclusion. This also points towards limited value at the current share price. Could both be missing something beneath the surface?

Look into how the SWS DCF model arrives at its fair value.

Stay updated when valuation signals shift by adding TFS Financial to your watchlist or portfolio. Alternatively, explore our screener to discover other companies that fit your criteria.

Build Your Own TFS Financial Narrative

If you see things differently or want to dig deeper into the numbers yourself, you can put together your own perspective in just a few minutes. Do it your way.

A great starting point for your TFS Financial research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Set yourself up for smarter investments by finding opportunities others overlook, using the powerful Simply Wall Street Screener for your next big move.

- Tap into tomorrow's financial breakthroughs and uncover cryptocurrency and blockchain stocks promising to transform the way we exchange and store value.

- Boost your cash flow with stocks offering reliable income streams by checking out the latest dividend stocks with yields > 3% opportunities with attractive yields.

- Stay ahead of fast-moving breakthroughs and gain exposure to AI penny stocks shaping the future of technology and business growth.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if TFS Financial might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NasdaqGS:TFSL

TFS Financial

Through its subsidiaries, provides retail consumer banking services in the United States.

Excellent balance sheet with proven track record and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion