Advertisement

- United Kingdom

- /

- Construction

- /

- AIM:RNWH

Top 3 Undervalued European Small Caps With Insider Buys In March 2025

Simply Wall St

Reviewed by Simply Wall St

As European markets navigate the complexities of U.S. trade tariffs and monetary policy uncertainties, the pan-European STOXX Europe 600 Index recently saw a decline amid these global economic pressures. Despite this backdrop, certain small-cap stocks in Europe present intriguing opportunities for investors, particularly those with insider buying activity that may suggest confidence in their potential value amidst current market conditions.

Top 10 Undervalued Small Caps With Insider Buying In Europe

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Bytes Technology Group | 22.7x | 5.8x | 11.75% | ★★★★★☆ |

| Macfarlane Group | 10.5x | 0.6x | 40.48% | ★★★★★☆ |

| Robert Walters | NA | 0.2x | 45.50% | ★★★★★☆ |

| Speedy Hire | NA | 0.2x | 20.89% | ★★★★★☆ |

| Gamma Communications | 21.5x | 2.2x | 38.57% | ★★★★☆☆ |

| Franchise Brands | 39.4x | 2.0x | 25.13% | ★★★★☆☆ |

| Optima Health | NA | 1.6x | 42.25% | ★★★★☆☆ |

| FastPartner | 16.7x | 4.7x | -86.06% | ★★★☆☆☆ |

| Elmera Group | 10.9x | 0.3x | -123.69% | ★★★☆☆☆ |

| Exsitec Holding | 27.8x | 2.0x | 42.85% | ★★★☆☆☆ |

Let's take a closer look at a couple of our picks from the screened companies.

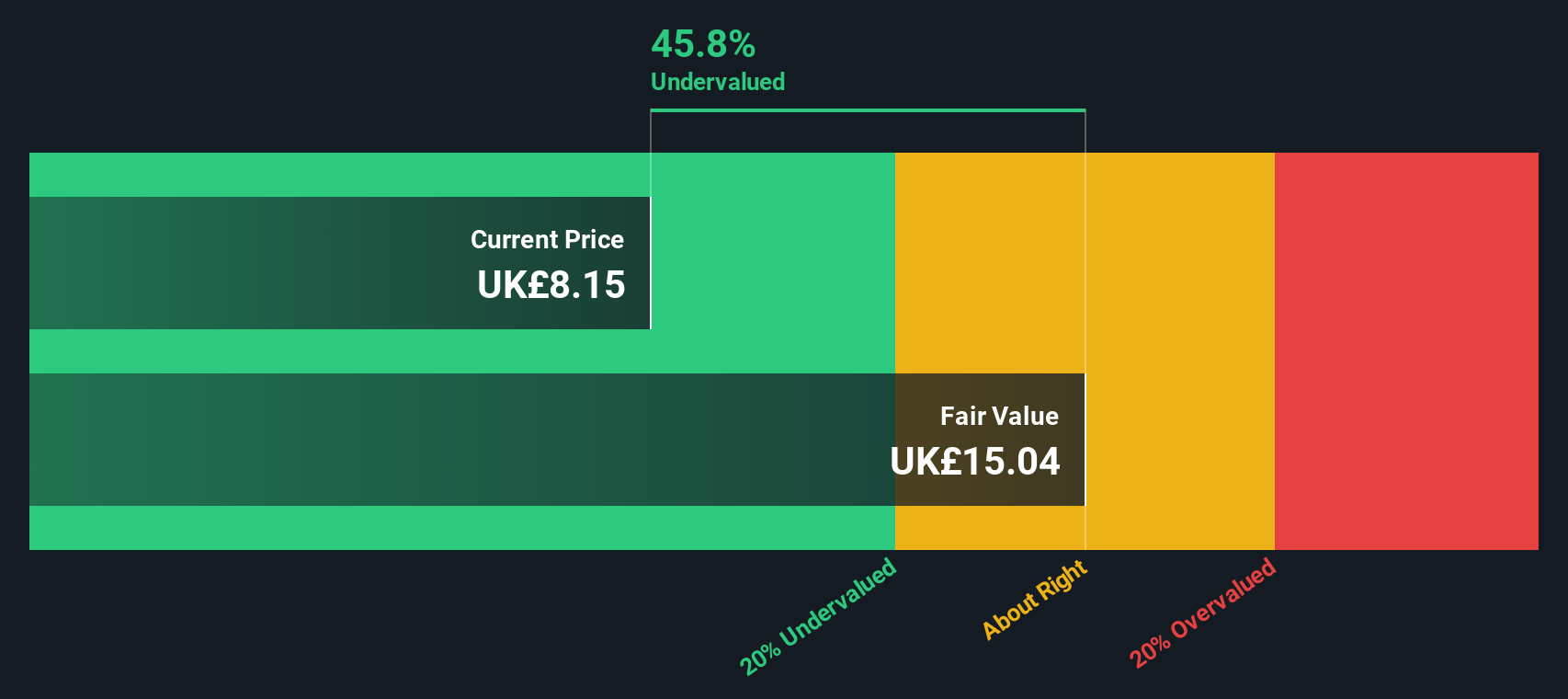

Renew Holdings (AIM:RNWH)

Simply Wall St Value Rating: ★★★★★☆

Overview: Renew Holdings is a UK-based engineering services group specializing in infrastructure, energy, and environmental markets with a market cap of £0.74 billion.

Operations: The company generates its revenue primarily from Engineering Services, with the latest reported revenue at £1.01 billion. The gross profit margin has shown fluctuations, reaching 15.23% in recent periods before declining to 14.04%. Operating expenses have been a significant component of costs, consistently impacting net income margins which were last recorded at 4.36%.

PE: 12.5x

Renew Holdings, a smaller player in the European market, exhibits potential for value with projected earnings growth of 7.74% annually. Despite recent share price volatility over the past three months, insider confidence is evident through strategic share purchases by executives from January to March 2024. However, reliance on external borrowing highlights funding risks. The upcoming Annual General Meeting on January 27, 2025, could provide further insights into their strategic direction and growth prospects within the industry.

- Click here and access our complete valuation analysis report to understand the dynamics of Renew Holdings.

Gain insights into Renew Holdings' historical performance by reviewing our past performance report.

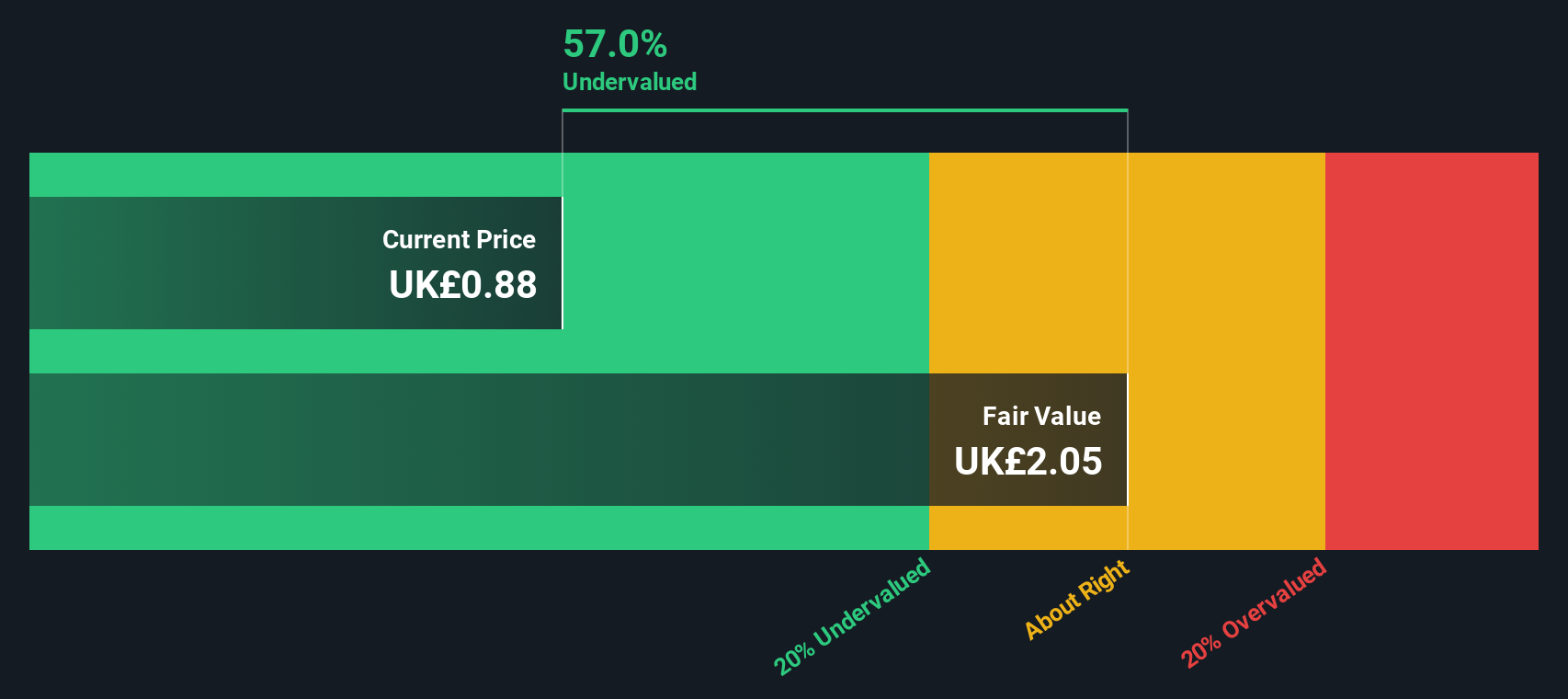

Card Factory (LSE:CARD)

Simply Wall St Value Rating: ★★★★★★

Overview: Card Factory is a UK-based retailer specializing in greeting cards, gifts, and celebration essentials through its physical stores and online platforms, with a market cap of £0.50 billion.

Operations: The company's revenue primarily comes from Cardfactory Stores, generating £491.90 million, with additional contributions from online sales and partnerships. Over the observed periods, the net income margin showed fluctuations, peaking at 17.40% in early 2016 before declining to 7.79% by mid-2024. Operating expenses have been a significant cost factor, consistently increasing alongside revenue growth over time.

PE: 7.1x

Card Factory, a smaller player in Europe's retail market, shows potential as an undervalued investment. Their recent sales report for the eleven months ending December 2024 revealed a 6.2% increase to £506.6 million, outperforming a tough non-food retail sector. Insider confidence is evident with significant share purchases over the past year, suggesting belief in future growth despite reliance on external borrowing for funding. Earnings are projected to grow by 14% annually, indicating promising prospects ahead.

- Click here to discover the nuances of Card Factory with our detailed analytical valuation report.

Review our historical performance report to gain insights into Card Factory's's past performance.

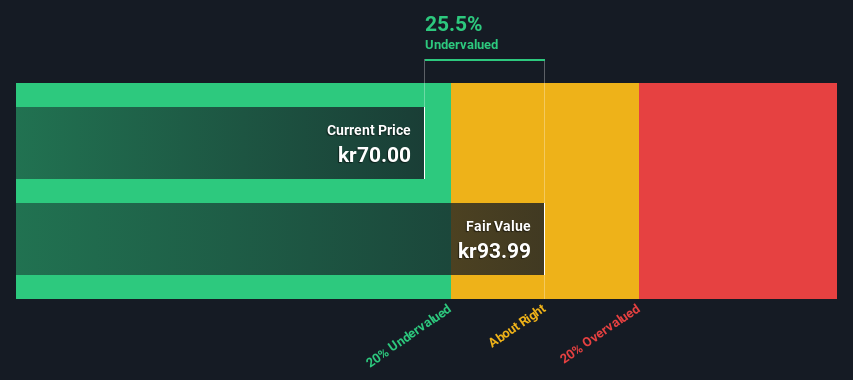

Hoist Finance (OM:HOFI)

Simply Wall St Value Rating: ★★★★★☆

Overview: Hoist Finance is a financial services company specializing in the acquisition and management of non-performing loan portfolios, with a market cap of SEK 2.5 billion.

Operations: The company's revenue primarily stems from unsecured and secured segments, with the former contributing significantly more. Operating expenses have been a substantial part of the cost structure, notably influenced by general and administrative expenses. A noteworthy trend is observed in net income margin, which has fluctuated over time, reaching 21.08% in recent periods after experiencing negative values earlier.

PE: 7.3x

Hoist Finance, a European financial services company, has seen insider confidence with share purchases over the past six months. Despite its high debt levels and reliance on external borrowing, Hoist's earnings are projected to grow by 20.33% annually. Recent leadership changes include the departure of Deputy CEO and CFO Christian Wallentin in March 2025. The firm announced a dividend of SEK 2 per share for May 2025, following improved Q4 net income of SEK 248 million compared to SEK 173 million last year.

- Take a closer look at Hoist Finance's potential here in our valuation report.

Examine Hoist Finance's past performance report to understand how it has performed in the past.

Turning Ideas Into Actions

- Unlock our comprehensive list of 61 Undervalued European Small Caps With Insider Buying by clicking here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About AIM:RNWH

Excellent balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor