Advertisement

August 2025's European Stocks That May Be Trading Below Estimated Value

Simply Wall St

Reviewed by Simply Wall St

As European markets navigate a period of economic stagnation and trade uncertainties, the pan-European STOXX Europe 600 Index recently ended 2.57% lower, reflecting disappointment with a new trade framework between the U.S. and the EU. Despite these challenges, investors may find opportunities in stocks that are potentially trading below their estimated value, offering a chance to capitalize on long-term growth prospects amidst current market fluctuations.

Top 10 Undervalued Stocks Based On Cash Flows In Europe

| Name | Current Price | Fair Value (Est) | Discount (Est) |

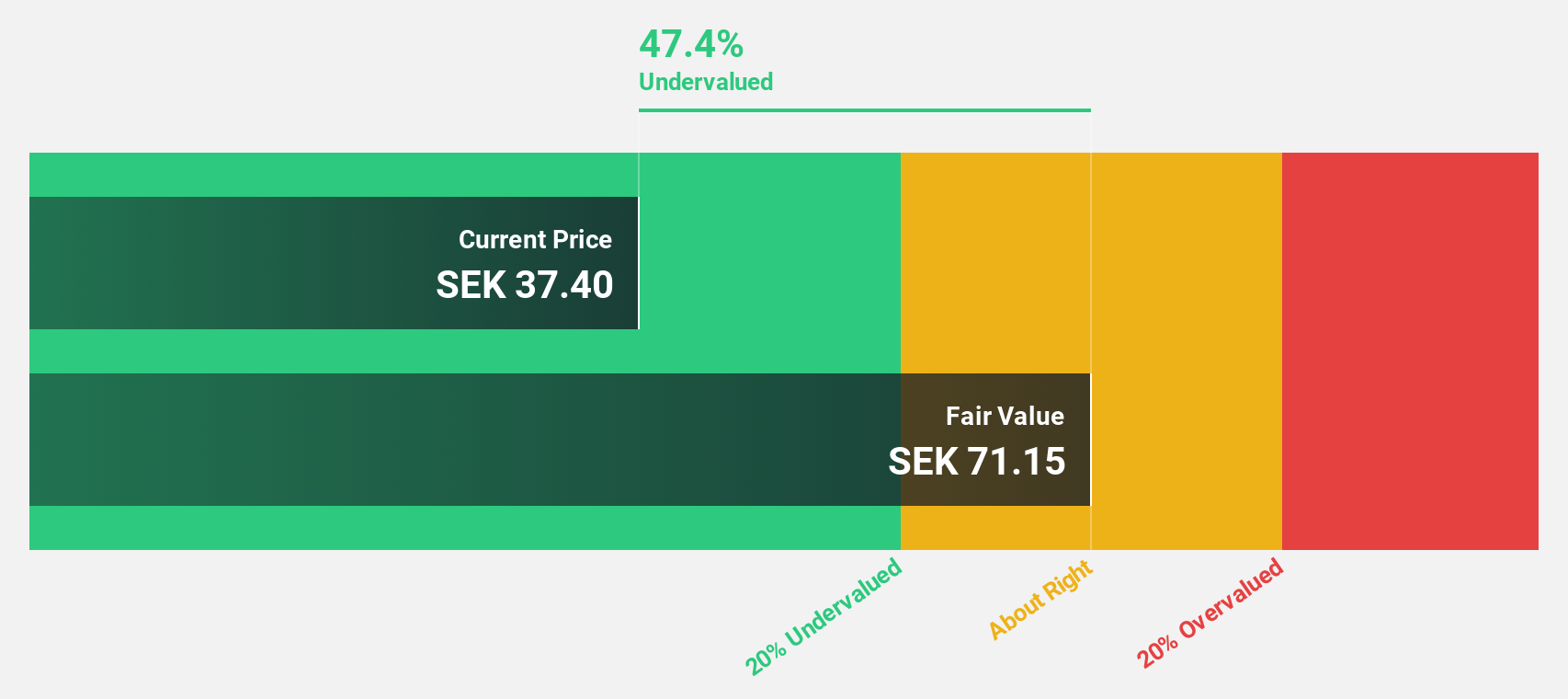

| Upsales Technology (OM:UPSALE) | SEK39.10 | SEK76.83 | 49.1% |

| Tecnotree Oyj (HLSE:TEM1V) | €4.855 | €9.57 | 49.3% |

| Sparebank 68° Nord (OB:SB68) | NOK177.00 | NOK349.92 | 49.4% |

| Rheinmetall (XTRA:RHM) | €1769.00 | €3480.81 | 49.2% |

| Libertas 7 (BME:LIB) | €2.96 | €5.87 | 49.6% |

| Exel Composites Oyj (HLSE:EXL1V) | €0.381 | €0.75 | 49.5% |

| doValue (BIT:DOV) | €2.48 | €4.85 | 48.9% |

| ams-OSRAM (SWX:AMS) | CHF10.35 | CHF20.67 | 49.9% |

| Alfio Bardolla Training Group (BIT:ABTG) | €1.85 | €3.63 | 49.1% |

| Absolent Air Care Group (OM:ABSO) | SEK260.00 | SEK508.35 | 48.9% |

Let's review some notable picks from our screened stocks.

Fagerhult Group (OM:FAG)

Overview: Fagerhult Group AB, along with its subsidiaries, designs, manufactures, and markets professional lighting solutions globally and has a market cap of approximately SEK6.98 billion.

Operations: The company generates revenue from several segments, including Premium (SEK2.69 billion), Collection (SEK3.59 billion), Professional (SEK929.70 million), Infrastructure (SEK778.70 million), and Smart Solutions (SEK12.50 million).

Estimated Discount To Fair Value: 45.6%

Fagerhult Group is trading significantly below its estimated fair value of SEK72.84, at SEK39.6, suggesting it is undervalued based on discounted cash flow analysis. Despite a challenging year with declining sales and net income, the company anticipates robust annual earnings growth of 34.8%, outpacing the Swedish market's 16.9%. However, profit margins have decreased to 2.9% from last year's 6%, and dividend coverage remains weak at a yield of 3.54%.

- Insights from our recent growth report point to a promising forecast for Fagerhult Group's business outlook.

- Click here and access our complete balance sheet health report to understand the dynamics of Fagerhult Group.

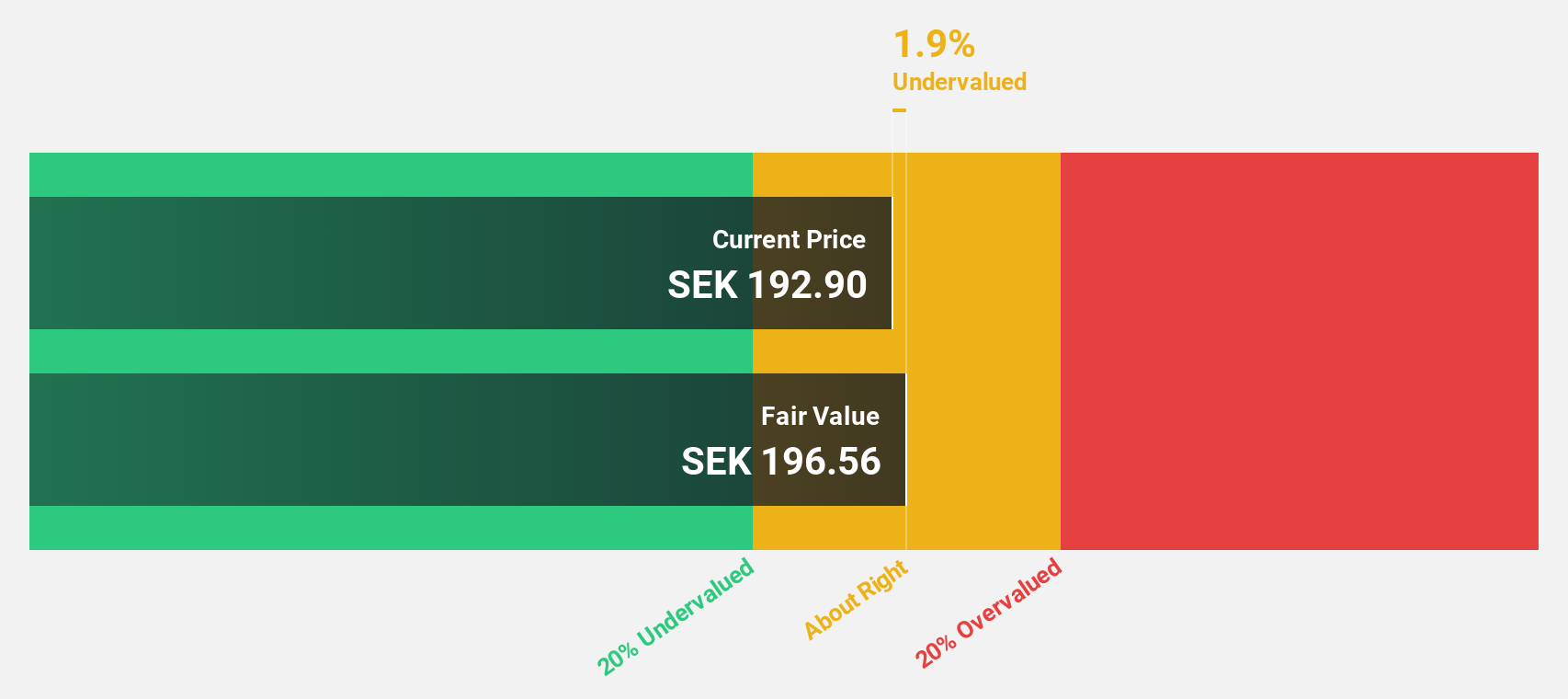

Paradox Interactive (OM:PDX)

Overview: Paradox Interactive AB (publ) is a developer and publisher of strategy and management games for PC and consoles, operating in the United States, Europe, Sweden, and internationally, with a market cap of SEK17.96 billion.

Operations: Paradox Interactive generates revenue primarily from its computer graphics segment, amounting to SEK2.18 billion.

Estimated Discount To Fair Value: 13.9%

Paradox Interactive is trading at SEK170, below its estimated fair value of SEK197.47, indicating potential undervaluation based on cash flow analysis. Recent product expansions and strategic alliances may support future revenue growth, forecasted at 9.3% annually—outpacing the Swedish market's 5.1%. Earnings are expected to grow significantly by 21.29% per year over the next three years, with a high return on equity projected at 24.9%, enhancing its investment appeal despite large one-off items impacting financial results recently.

- Our earnings growth report unveils the potential for significant increases in Paradox Interactive's future results.

- Click to explore a detailed breakdown of our findings in Paradox Interactive's balance sheet health report.

Basler (XTRA:BSL)

Overview: Basler Aktiengesellschaft develops, manufactures, and sells digital cameras for professional users both in Germany and internationally, with a market cap of €395.35 million.

Operations: The company's revenue segment includes the sale of digital cameras, generating €199.67 million.

Estimated Discount To Fair Value: 15.1%

Basler is trading at €12.86, below its estimated fair value of €15.15, offering potential undervaluation based on cash flow analysis. Despite a volatile share price recently, Basler's earnings are forecast to grow significantly at 84.68% annually, with revenue growth expected to outpace the German market at 10% per year. Recent Q1 results showed sales of €59.46 million and net income of €4.79 million, reversing a previous loss—a positive sign for profitability prospects over the next three years.

- According our earnings growth report, there's an indication that Basler might be ready to expand.

- Unlock comprehensive insights into our analysis of Basler stock in this financial health report.

Summing It All Up

- Discover the full array of 187 Undervalued European Stocks Based On Cash Flows right here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Basler might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About XTRA:BSL

Basler

Engages in the development, manufacture, and sale of digital cameras for professional users in Germany and internationally.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|33.9% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|26.5% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.3% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor