Stock Analysis

Money Forward And Two More Top Growth Companies With High Insider Ownership On The Japanese Exchange

Reviewed by Simply Wall St

As Japan's stock markets face notable declines, with the Nikkei 225 and TOPIX indices experiencing sharp weekly losses, investors are closely monitoring shifts in market dynamics. In this context, examining growth companies with high insider ownership can offer insights into firms that potentially have aligned interests between management and shareholders, a factor that might be particularly reassuring during times of market volatility.

Top 10 Growth Companies With High Insider Ownership In Japan

| Name | Insider Ownership | Earnings Growth |

| Hottolink (TSE:3680) | 27% | 59.7% |

| Micronics Japan (TSE:6871) | 15.3% | 39.8% |

| Kasumigaseki CapitalLtd (TSE:3498) | 34.8% | 43.3% |

| Medley (TSE:4480) | 34% | 28.7% |

| Kanamic NetworkLTD (TSE:3939) | 25% | 28.9% |

| SHIFT (TSE:3697) | 35.4% | 32.8% |

| ExaWizards (TSE:4259) | 21.9% | 91.1% |

| Money Forward (TSE:3994) | 21.4% | 66.9% |

| Astroscale Holdings (TSE:186A) | 20.9% | 90% |

| Soracom (TSE:147A) | 16.5% | 54.1% |

Let's uncover some gems from our specialized screener.

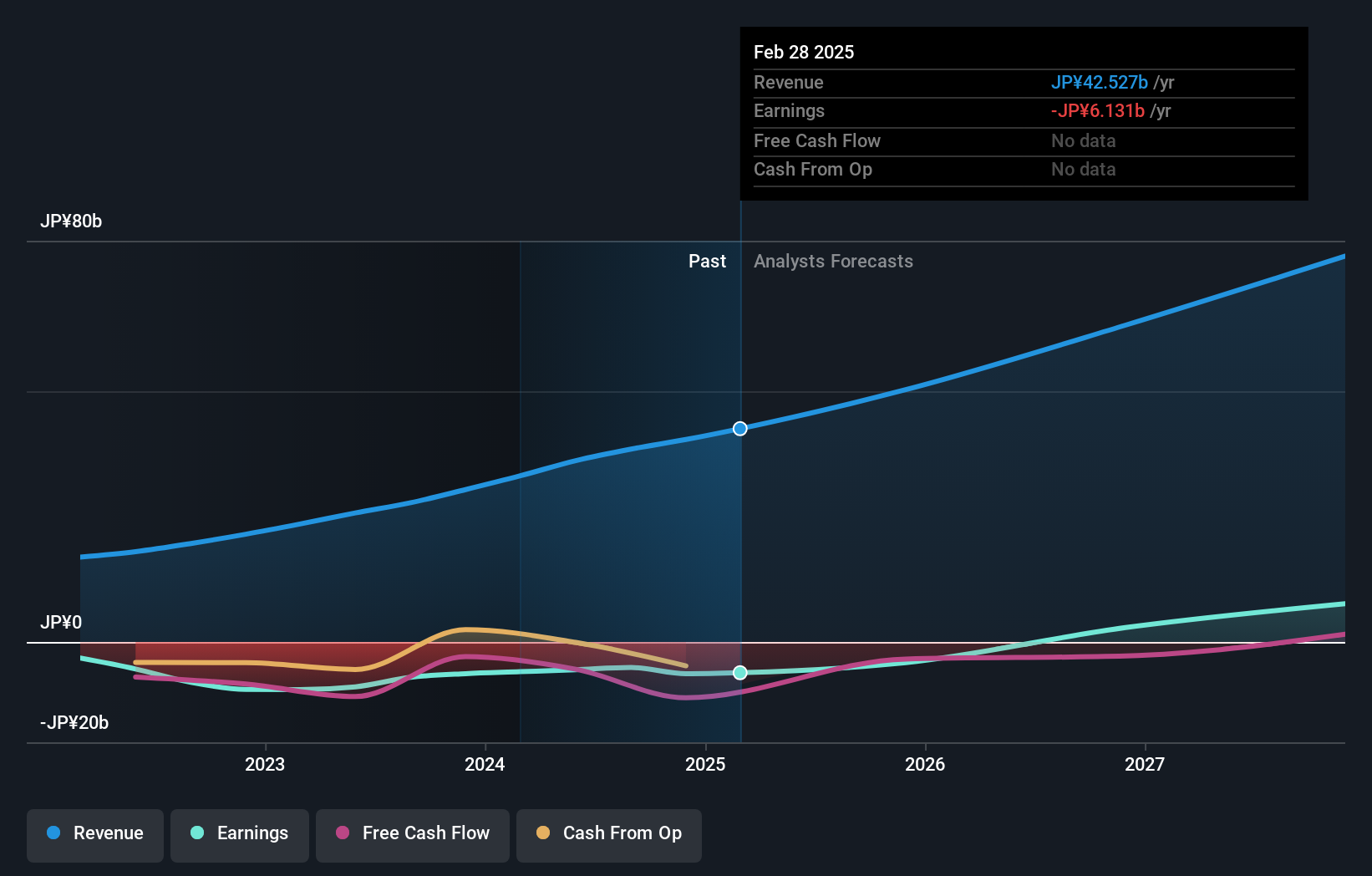

Money Forward (TSE:3994)

Simply Wall St Growth Rating: ★★★★★★

Overview: Money Forward, Inc. offers financial solutions to individuals, financial institutions, and corporations mainly in Japan, with a market capitalization of approximately ¥278.96 billion.

Operations: The firm generates revenue by offering financial solutions tailored to the needs of individuals, financial institutions, and corporations across Japan.

Insider Ownership: 21.4%

Earnings Growth Forecast: 66.9% p.a.

Money Forward, a Japanese company, is poised for significant growth with earnings expected to increase and revenue projected to grow at 20.5% annually, outpacing the domestic market's 4.3%. Despite its high volatility in share price recently, it trades at 50.5% below estimated fair value and anticipates becoming profitable within three years. Strategic moves include forming a joint venture for PFM services and restructuring business domains to enhance focus and efficiency, reflecting proactive management aligned with insider interests.

- Navigate through the intricacies of Money Forward with our comprehensive analyst estimates report here.

- Insights from our recent valuation report point to the potential overvaluation of Money Forward shares in the market.

Round One (TSE:4680)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Round One Corporation operates indoor leisure complex facilities, with a market capitalization of approximately ¥244.27 billion.

Operations: The company generates revenues primarily from its indoor leisure facilities in Japan and the USA, with respective earnings of ¥97.99 billion and ¥59.58 billion.

Insider Ownership: 35.2%

Earnings Growth Forecast: 11% p.a.

Round One, a Japanese growth company with high insider ownership, has shown robust sales performance with significant year-to-date increases in both Japan and the USA. Despite its highly volatile share price over the past three months, Round One's revenue is expected to grow at 7.1% annually, surpassing Japan's market average of 4.3%. The company also pays a reliable dividend and trades significantly below estimated fair value, offering potential value to investors. However, earnings growth forecasts are moderate compared to industry leaders.

- Get an in-depth perspective on Round One's performance by reading our analyst estimates report here.

- Our valuation report here indicates Round One may be undervalued.

Rakuten Group (TSE:4755)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Rakuten Group, Inc., a diversified company based in Japan, operates in e-commerce, fintech, digital content, and communications sectors globally with a market capitalization of approximately ¥1.94 trillion.

Operations: The company generates revenue through its operations in e-commerce, fintech, digital content, and communications sectors across both domestic and international markets.

Insider Ownership: 17.3%

Earnings Growth Forecast: 81.8% p.a.

Rakuten Group, a Japanese company with high insider ownership, is set to see its revenue grow by 7.8% annually, outpacing the local market's 4.3%. While its return on equity is expected to remain low at 8.9%, the firm forecasts significant earnings growth of 81.78% per year and anticipates profitability within three years. Despite these prospects, Rakuten trades at a substantial discount—78.2% below its estimated fair value—highlighting potential for investor gains amidst operational challenges.

- Click here to discover the nuances of Rakuten Group with our detailed analytical future growth report.

- Our valuation report unveils the possibility Rakuten Group's shares may be trading at a discount.

Where To Now?

- Delve into our full catalog of 101 Fast Growing Japanese Companies With High Insider Ownership here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:4755

Rakuten Group

Provides services in e-commerce, fintech, digital content, and communications to various users in Japan and internationally.

Reasonable growth potential with adequate balance sheet.