Advertisement

- India

- /

- Consumer Finance

- /

- NSEI:CHOLAFIN

Investors Holding Back On Cholamandalam Investment and Finance Company Limited (NSE:CHOLAFIN)

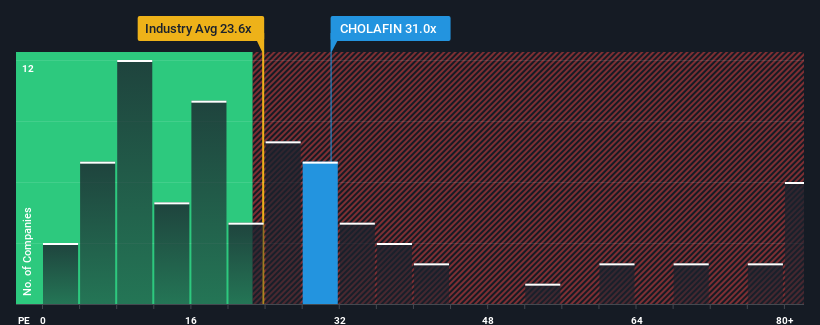

With a median price-to-earnings (or "P/E") ratio of close to 34x in India, you could be forgiven for feeling indifferent about Cholamandalam Investment and Finance Company Limited's (NSE:CHOLAFIN) P/E ratio of 31x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

Cholamandalam Investment and Finance certainly has been doing a good job lately as it's been growing earnings more than most other companies. One possibility is that the P/E is moderate because investors think this strong earnings performance might be about to tail off. If not, then existing shareholders have reason to be feeling optimistic about the future direction of the share price.

View our latest analysis for Cholamandalam Investment and Finance

How Is Cholamandalam Investment and Finance's Growth Trending?

The only time you'd be comfortable seeing a P/E like Cholamandalam Investment and Finance's is when the company's growth is tracking the market closely.

Taking a look back first, we see that the company grew earnings per share by an impressive 29% last year. Pleasingly, EPS has also lifted 152% in aggregate from three years ago, thanks to the last 12 months of growth. Therefore, it's fair to say the earnings growth recently has been superb for the company.

Looking ahead now, EPS is anticipated to climb by 24% per year during the coming three years according to the analysts following the company. That's shaping up to be materially higher than the 20% per year growth forecast for the broader market.

In light of this, it's curious that Cholamandalam Investment and Finance's P/E sits in line with the majority of other companies. It may be that most investors aren't convinced the company can achieve future growth expectations.

What We Can Learn From Cholamandalam Investment and Finance's P/E?

Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that Cholamandalam Investment and Finance currently trades on a lower than expected P/E since its forecast growth is higher than the wider market. When we see a strong earnings outlook with faster-than-market growth, we assume potential risks are what might be placing pressure on the P/E ratio. At least the risk of a price drop looks to be subdued, but investors seem to think future earnings could see some volatility.

And what about other risks? Every company has them, and we've spotted 2 warning signs for Cholamandalam Investment and Finance (of which 1 is a bit concerning!) you should know about.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:CHOLAFIN

Cholamandalam Investment and Finance

Operates as a non-banking finance company in India.

High growth potential with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor