- Hong Kong

- /

- Real Estate

- /

- SEHK:14

Revenue Downgrade: Here's What Analysts Forecast For Hysan Development Company Limited (HKG:14)

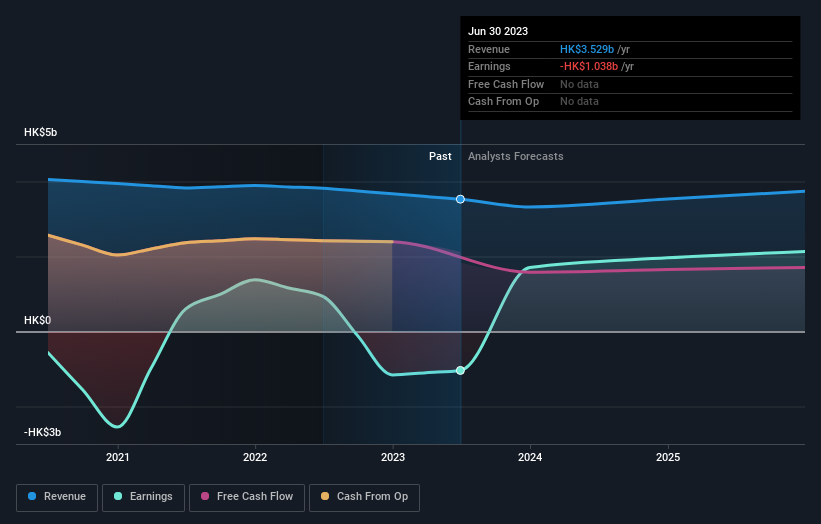

One thing we could say about the analysts on Hysan Development Company Limited (HKG:14) - they aren't optimistic, having just made a major negative revision to their near-term (statutory) forecasts for the organization. There was a fairly draconian cut to their revenue estimates, perhaps an implicit admission that previous forecasts were much too optimistic.

Following the latest downgrade, the current consensus, from the twelve analysts covering Hysan Development, is for revenues of HK$3.3b in 2023, which would reflect a noticeable 5.4% reduction in Hysan Development's sales over the past 12 months. Prior to the latest estimates, the analysts were forecasting revenues of HK$3.7b in 2023. The forecasts seem less optimistic overall, with the modest decline in revenue estimates in the latest consensus update.

Check out our latest analysis for Hysan Development

The consensus price target fell 7.3% to HK$26.07, with the analysts clearly less optimistic about Hysan Development's valuation following this update.

Of course, another way to look at these forecasts is to place them into context against the industry itself. Over the past five years, revenues have declined around 2.8% annually. Worse, forecasts are essentially predicting the decline to accelerate, with the estimate for an annualised 10% decline in revenue until the end of 2023. Compare this against analyst estimates for companies in the broader industry, which suggest that revenues (in aggregate) are expected to grow 10% annually. So it's pretty clear that, while it does have declining revenues, the analysts also expect Hysan Development to suffer worse than the wider industry.

The Bottom Line

The clear low-light was that analysts slashing their revenue forecasts for Hysan Development this year. They also expect company revenue to perform worse than the wider market. The consensus price target fell measurably, with analysts seemingly not reassured by recent business developments, leading to a lower estimate of Hysan Development's future valuation. Overall, given the drastic downgrade to this year's forecasts, we'd be feeling a little more wary of Hysan Development going forwards.

Thirsting for more data? We have estimates for Hysan Development from its twelve analysts out until 2025, and you can see them free on our platform here.

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are downgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Hysan Development might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:14

Hysan Development

Hysan’s investment portfolio is set predominantly in Lee Gardens, a unique part of Hong Kong’s renowned commercial heart in Causeway Bay.

Moderate growth potential with imperfect balance sheet.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)