- Switzerland

- /

- Software

- /

- SWX:TEMN

February 2025's Leading Growth Companies With Insider Confidence

Reviewed by Simply Wall St

As global markets navigate a complex landscape of interest rate adjustments and geopolitical tensions, investor sentiment remains cautious amid volatile earnings reports and competitive pressures in the AI sector. Despite these challenges, certain growth companies with high insider ownership continue to draw attention, as insider confidence can be an indicator of potential resilience and long-term value amidst fluctuating market conditions.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Duc Giang Chemicals Group (HOSE:DGC) | 31.4% | 25.7% |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 41.2% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 26.2% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Pricol (NSEI:PRICOLLTD) | 25.4% | 25.2% |

| Plenti Group (ASX:PLT) | 12.7% | 120.1% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.2% | 135% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 119.4% |

| Brightstar Resources (ASX:BTR) | 16.2% | 86% |

| Fulin Precision (SZSE:300432) | 13.6% | 71% |

Let's uncover some gems from our specialized screener.

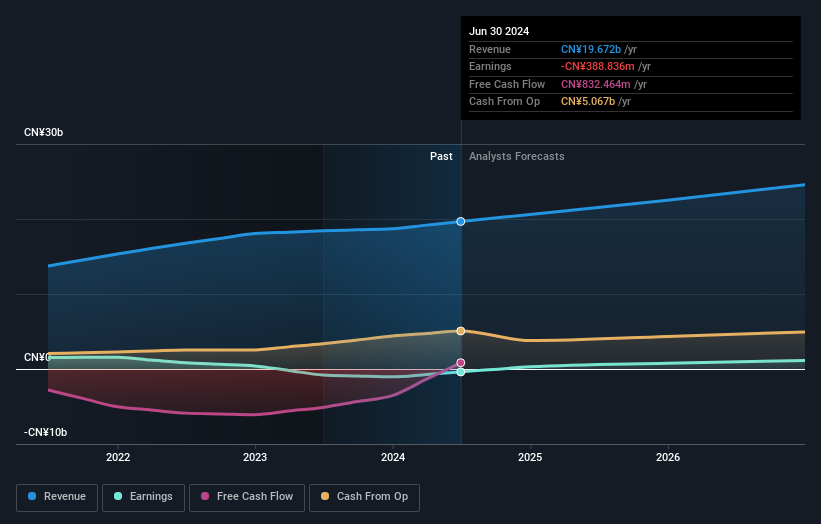

China Youran Dairy Group (SEHK:9858)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: China Youran Dairy Group Limited is an investment holding company that operates as an integrated provider of products and services in the upstream dairy industry in China, with a market cap of approximately HK$7.63 billion.

Operations: The company generates revenue from its Raw Milk Business, amounting to CN¥14.07 billion, and Comprehensive Ruminant Farming Solutions, contributing CN¥7.65 billion.

Insider Ownership: 14.5%

Earnings Growth Forecast: 98% p.a.

China Youran Dairy Group is poised for profitability within three years, with earnings expected to grow by 98% annually. Despite having a high level of debt, it trades at a good value compared to peers and the industry. Revenue growth is forecast at 8.9% per year, outpacing the Hong Kong market's average of 7.7%. However, its Return on Equity is projected to be low at 7.9%, which may temper some investor enthusiasm.

- Navigate through the intricacies of China Youran Dairy Group with our comprehensive analyst estimates report here.

- The analysis detailed in our China Youran Dairy Group valuation report hints at an deflated share price compared to its estimated value.

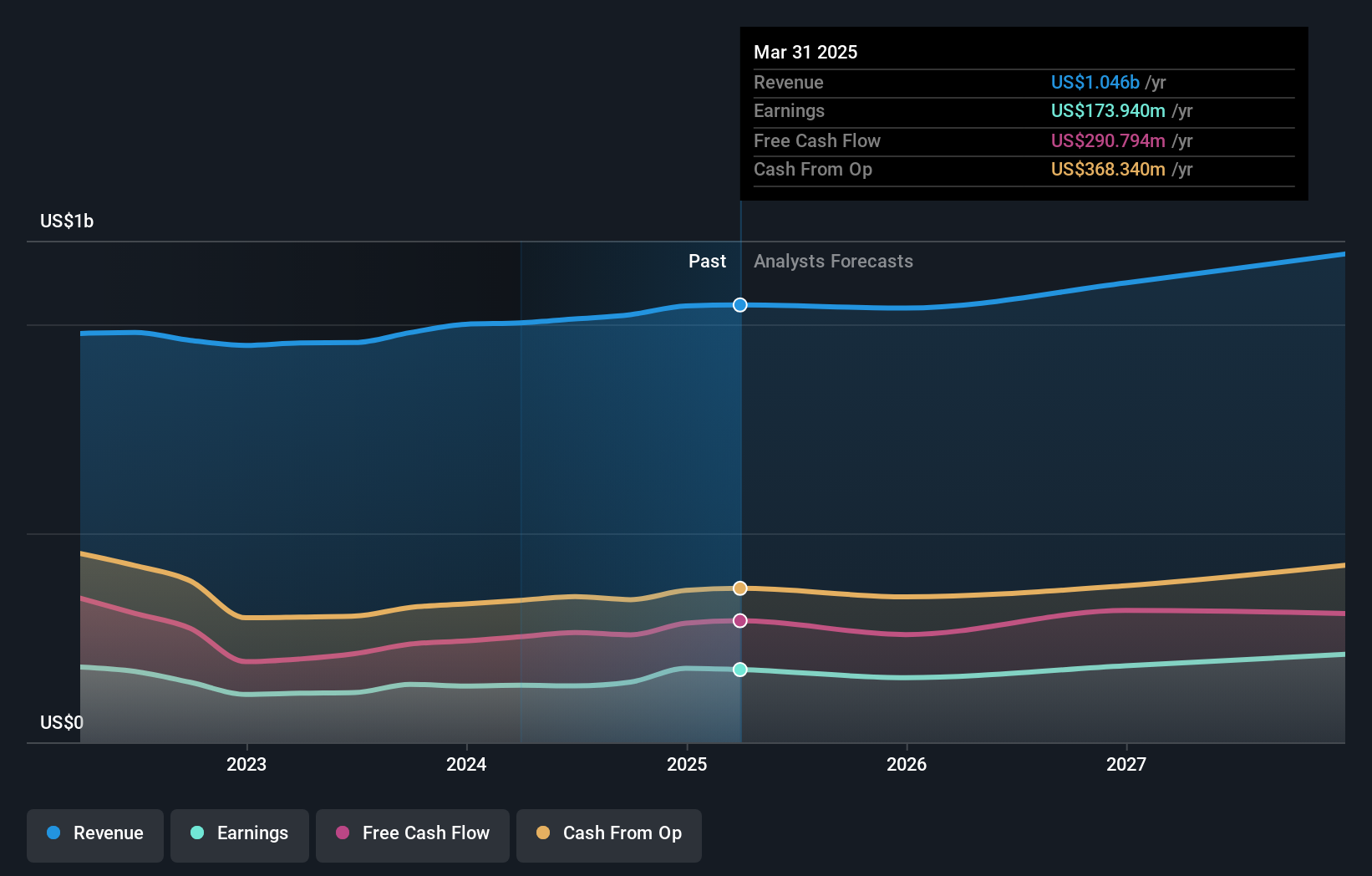

Temenos (SWX:TEMN)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Temenos AG develops, markets, and sells integrated banking software systems to banking and other financial institutions worldwide, with a market cap of CHF5.69 billion.

Operations: The company's revenue segments include software licensing, which generated $357.4 million; software-as-a-service (SaaS) at $118.2 million; maintenance at $422.1 million; and services contributing $199.3 million, all in USD.

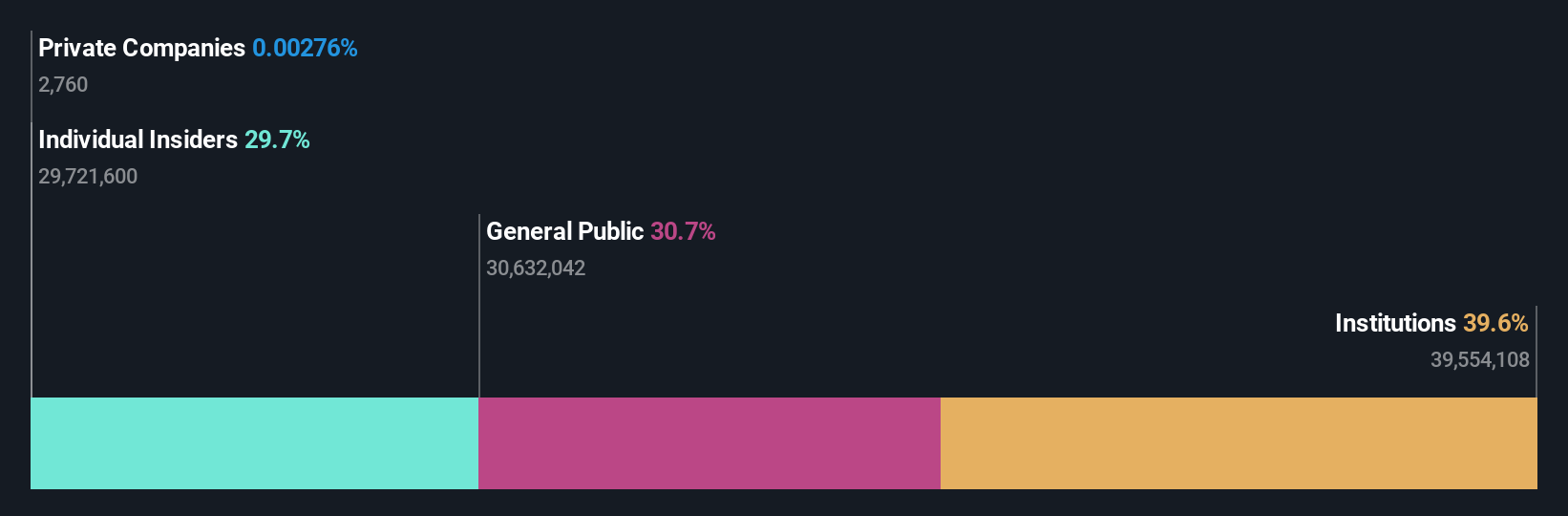

Insider Ownership: 21.8%

Earnings Growth Forecast: 12% p.a.

Temenos is positioned for growth, with earnings expected to increase by 12% annually, surpassing the Swiss market average. Revenue is also forecasted to grow at 7.3% per year. Recent partnerships with CEC Bank and AHAM Capital highlight its expanding influence in banking technology, while collaborations like the one with NVIDIA emphasize innovation in AI solutions. Despite a high debt level, Temenos trades below its estimated fair value, suggesting potential investment appeal.

- Dive into the specifics of Temenos here with our thorough growth forecast report.

- Insights from our recent valuation report point to the potential undervaluation of Temenos shares in the market.

CD Projekt (WSE:CDR)

Simply Wall St Growth Rating: ★★★★★★

Overview: CD Projekt S.A., along with its subsidiaries, develops, publishes, and digitally distributes video games for personal computers and consoles in Poland, with a market cap of PLN21.09 billion.

Operations: The company's revenue is primarily derived from its CD PROJEKT RED segment, contributing PLN937.83 million, and the GOG.Com segment, which adds PLN203.76 million.

Insider Ownership: 29.7%

Earnings Growth Forecast: 34.2% p.a.

CD Projekt is poised for significant growth, with earnings forecasted to rise 34.17% annually, outpacing the Polish market. Revenue is expected to grow at 24.5% per year, indicating strong potential despite recent declines in quarterly revenue and net income compared to the previous year. Trading substantially below its estimated fair value enhances its investment appeal. Recent conference presentations underscore a focus on future growth prospects amidst high insider ownership stability.

- Delve into the full analysis future growth report here for a deeper understanding of CD Projekt.

- In light of our recent valuation report, it seems possible that CD Projekt is trading beyond its estimated value.

Taking Advantage

- Click this link to deep-dive into the 1477 companies within our Fast Growing Companies With High Insider Ownership screener.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if Temenos might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SWX:TEMN

Temenos

Develops, markets, and sells integrated banking software systems to banking and other financial institutions worldwide.

Reasonable growth potential average dividend payer.

Similar Companies

Market Insights

Community Narratives