- United Kingdom

- /

- Transportation

- /

- LSE:FGP

Alpha Group International Leads These 3 Undervalued Small Caps With Insider Buying In UK

Reviewed by Simply Wall St

The United Kingdom's stock market has recently faced challenges, with the FTSE 100 and FTSE 250 indices experiencing declines amid weak trade data from China, highlighting concerns over global economic recovery. This environment underscores the importance of identifying resilient small-cap companies that can navigate such uncertainties, particularly those showing signs of insider confidence and potential undervaluation.

Top 10 Undervalued Small Caps With Insider Buying In The United Kingdom

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Senior | 18.8x | 0.6x | 35.85% | ★★★★★★ |

| NWF Group | 8.1x | 0.1x | 39.20% | ★★★★★☆ |

| J D Wetherspoon | 14.7x | 0.4x | 13.90% | ★★★★★☆ |

| John Wood Group | NA | 0.2x | 41.60% | ★★★★★☆ |

| Genus | 164.6x | 1.9x | 17.41% | ★★★★★☆ |

| Headlam Group | NA | 0.2x | 25.79% | ★★★★★☆ |

| Marlowe | NA | 0.7x | 40.70% | ★★★★☆☆ |

| Optima Health | NA | 1.3x | 37.32% | ★★★★☆☆ |

| Sabre Insurance Group | 11.4x | 1.5x | 13.97% | ★★★☆☆☆ |

| THG | NA | 0.3x | -265.26% | ★★★☆☆☆ |

Let's uncover some gems from our specialized screener.

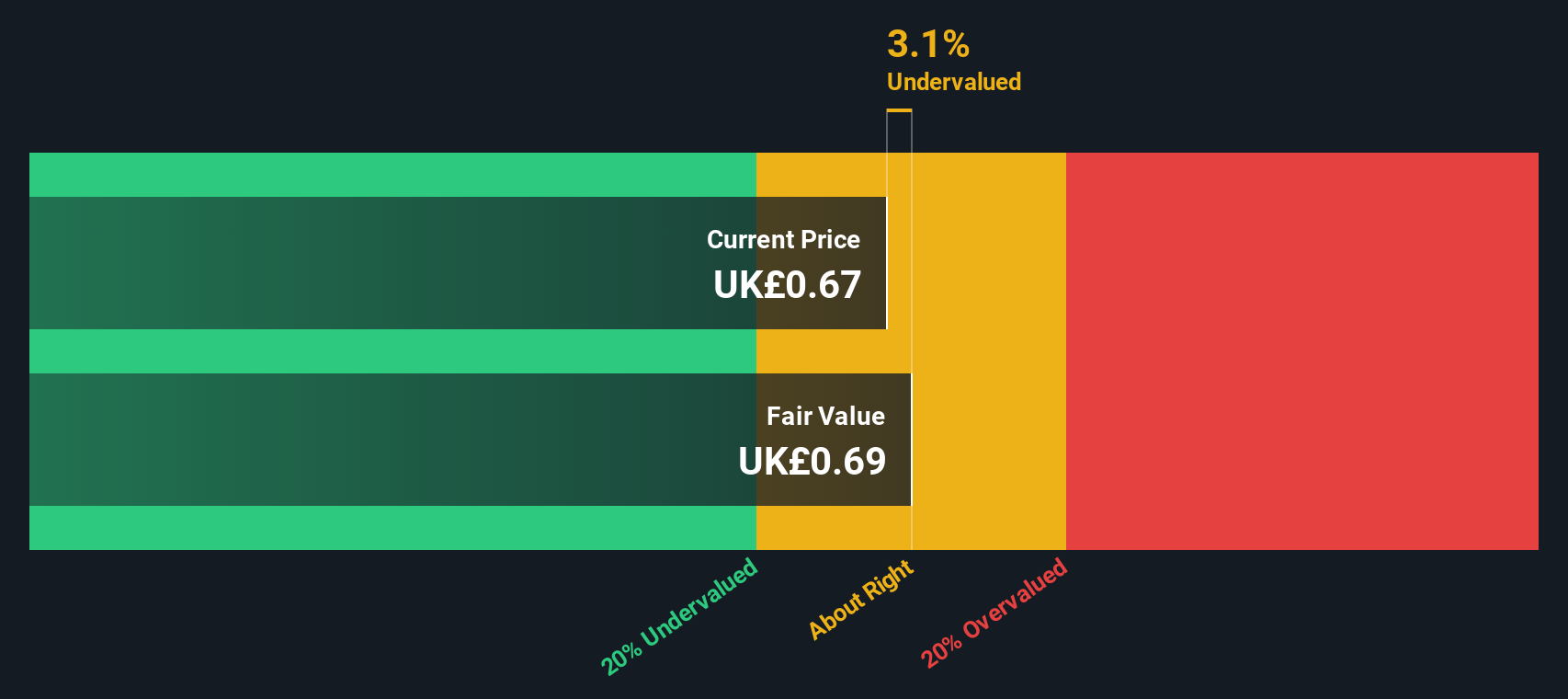

Alpha Group International (LSE:ALPH)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Alpha Group International operates in the financial services sector, providing payment and risk management solutions across various segments, with a market capitalization of £1.2 billion.

Operations: Alpha Group International's revenue streams primarily include Alpha Pay (£72.30 million), Institutional (£67.47 million), Corporate London excluding Amsterdam (£46.92 million), Corporate Amsterdam (£9.57 million), and Corporate Toronto (£3.72 million). The company reported a gross profit margin of 85.58% as of June 2024, reflecting its ability to manage costs effectively relative to revenue growth over time, with operating expenses including general and administrative costs being a significant component of its expenditure structure.

PE: 10.0x

Alpha Group International, a UK-based company, recently joined the S&P Global BMI Index and reported strong financial performance for the half-year ending June 2024, with sales of £64.33 million and net income of £44.84 million. Insider confidence is evident as Clive Kahn purchased 50,000 shares for approximately £1.04 million in September 2024. The company plans to increase its interim dividend to 4.2 pence per share, reflecting potential growth prospects despite relying on external borrowing for funding needs.

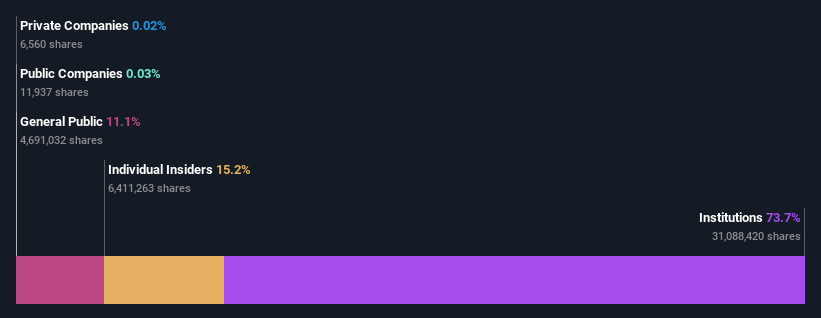

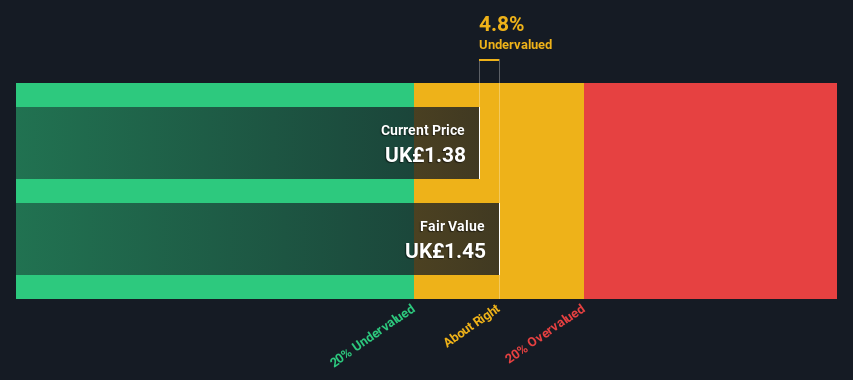

FirstGroup (LSE:FGP)

Simply Wall St Value Rating: ★★★★★☆

Overview: FirstGroup is a leading UK-based transport operator with core operations in bus and rail services, and it has a market capitalization of approximately £0.83 billion.

Operations: FirstGroup generates revenue primarily from its First Rail and First Bus segments, with the former contributing significantly more. The company experienced fluctuations in its gross profit margin, which peaked at 77.56% in September 2020 but showed negative values at other times, such as -8.03% in June 2023.

PE: -80.3x

FirstGroup, a UK-based transportation company, is currently viewed as undervalued in the market. Recent insider confidence is evident with notable share purchases made by insiders over the past few months. The company's growth forecast shows an impressive 44% annual increase in earnings, suggesting strong potential for future performance. However, it's important to note that FirstGroup relies entirely on external borrowing for funding, which carries higher risk compared to customer deposits.

- Delve into the full analysis valuation report here for a deeper understanding of FirstGroup.

Gain insights into FirstGroup's past trends and performance with our Past report.

Hays (LSE:HAS)

Simply Wall St Value Rating: ★★★★★★

Overview: Hays is a global recruitment company specializing in qualified, professional, and skilled recruitment services with a market cap of approximately £1.72 billion.

Operations: The company generates revenue primarily from its Qualified, Professional and Skilled Recruitment segment, with a recent figure of £6.95 billion. The gross profit margin has shown variability, reaching 14.34% in late 2019 before declining to 4.21% by mid-2024. Operating expenses are significant, including general and administrative costs which were £159.5 million as of the latest period ending in November 2024.

PE: -253.1x

Hays, a recruitment firm in the UK, is navigating challenging waters with a recent net loss of £4.9 million for the year ending June 2024, contrasting sharply with last year's £138.3 million profit. Despite this setback, earnings are projected to grow at an impressive 63% annually. Insider confidence is evident as executives have increased their shareholdings over recent months. While reliant on external borrowing for funding, Hays' strategic shifts and leadership changes could steer future growth opportunities in a competitive market landscape.

- Click here and access our complete valuation analysis report to understand the dynamics of Hays.

Review our historical performance report to gain insights into Hays''s past performance.

Seize The Opportunity

- Explore the 25 names from our Undervalued UK Small Caps With Insider Buying screener here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:FGP

Adequate balance sheet and fair value.