- United Kingdom

- /

- Specialty Stores

- /

- LSE:AO.

UK Stocks With Insider Ownership Expecting Up To 93% Growth

Reviewed by Simply Wall St

The United Kingdom's stock market has recently faced challenges, with the FTSE 100 index experiencing declines due to weak trade data from China and falling commodity prices impacting major companies. As global economic uncertainties persist, investors often look for growth companies with substantial insider ownership, as this can indicate confidence in the company's future prospects and alignment of interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership In The United Kingdom

| Name | Insider Ownership | Earnings Growth |

| Filtronic (AIM:FTC) | 28.8% | 55.7% |

| Gulf Keystone Petroleum (LSE:GKP) | 12.2% | 93.9% |

| Integrated Diagnostics Holdings (LSE:IDHC) | 27.6% | 21.5% |

| Foresight Group Holdings (LSE:FSG) | 34.2% | 23.5% |

| Facilities by ADF (AIM:ADF) | 13.1% | 190% |

| LSL Property Services (LSE:LSL) | 10.7% | 28.2% |

| Judges Scientific (AIM:JDG) | 10.6% | 29.4% |

| Mortgage Advice Bureau (Holdings) (AIM:MAB1) | 19.8% | 26.4% |

| PensionBee Group (LSE:PBEE) | 38.8% | 67.1% |

| Anglo Asian Mining (AIM:AAZ) | 40% | 189.1% |

Let's uncover some gems from our specialized screener.

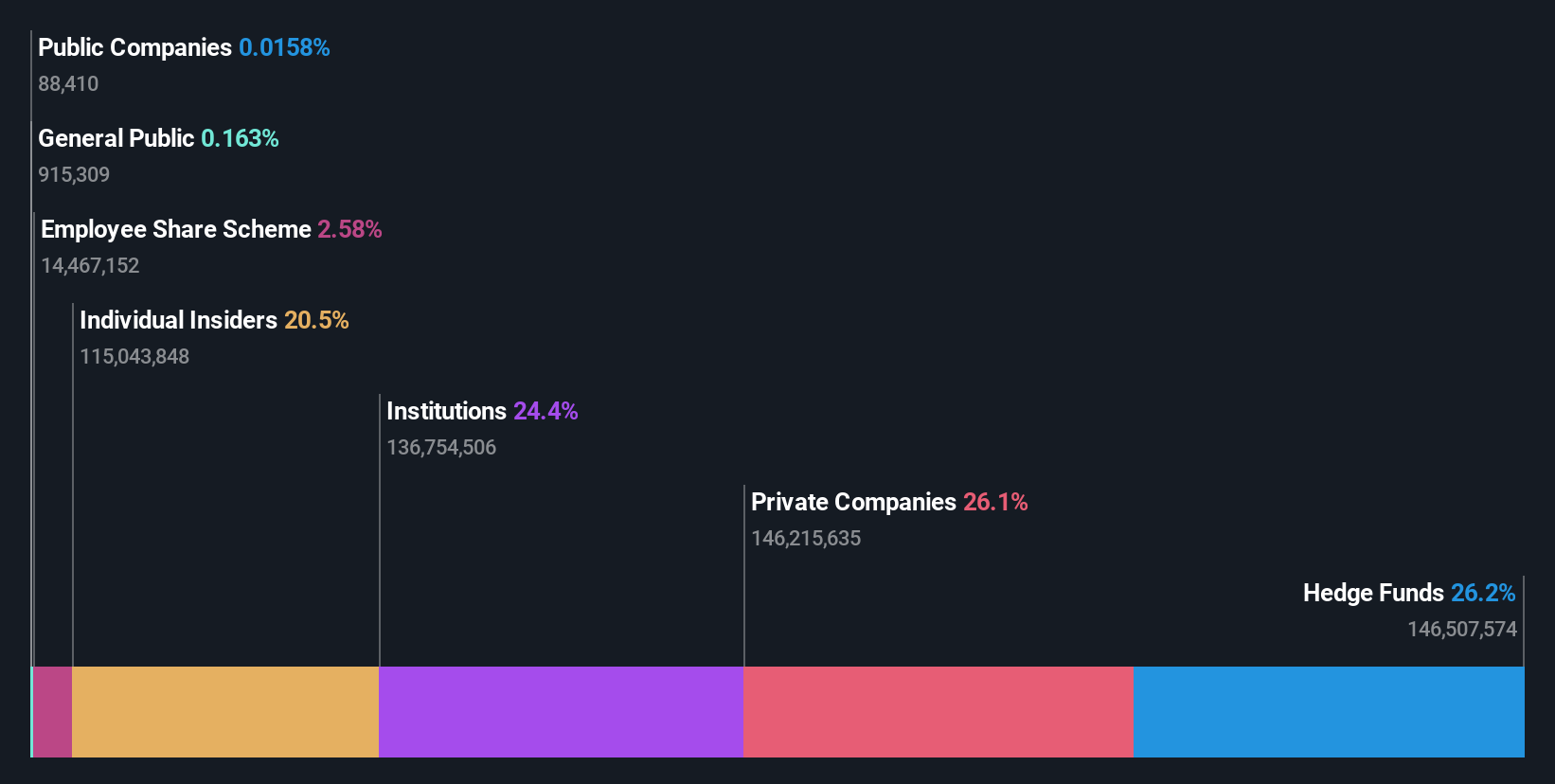

Equals Group (AIM:EQLS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Equals Group plc develops and sells payment platforms in the United Kingdom, offering services such as prepaid currency cards, international money transfers, and current accounts to private clients and corporations, with a market cap of £253.74 million.

Operations: The company's revenue segments include Banking (£8.26 million), Solutions (£42.15 million), Travel Cash (£0.02 million), Currency Cards (£15.46 million), and International Payments excluding Solutions (£40.71 million).

Insider Ownership: 20.3%

Earnings Growth Forecast: 32% p.a.

Equals Group is undergoing a significant transition with an all-cash acquisition leading to its delisting from AIM and re-registration as a private company. Despite this, the company's earnings are forecast to grow significantly at 32% annually, outpacing the UK market. Revenue growth is also expected at 18.8% per year, though slightly below high-growth thresholds. Recent insider activities show more buying than selling over three months, indicating confidence amidst substantial profit growth in recent years.

- Click here to discover the nuances of Equals Group with our detailed analytical future growth report.

- Our valuation report here indicates Equals Group may be overvalued.

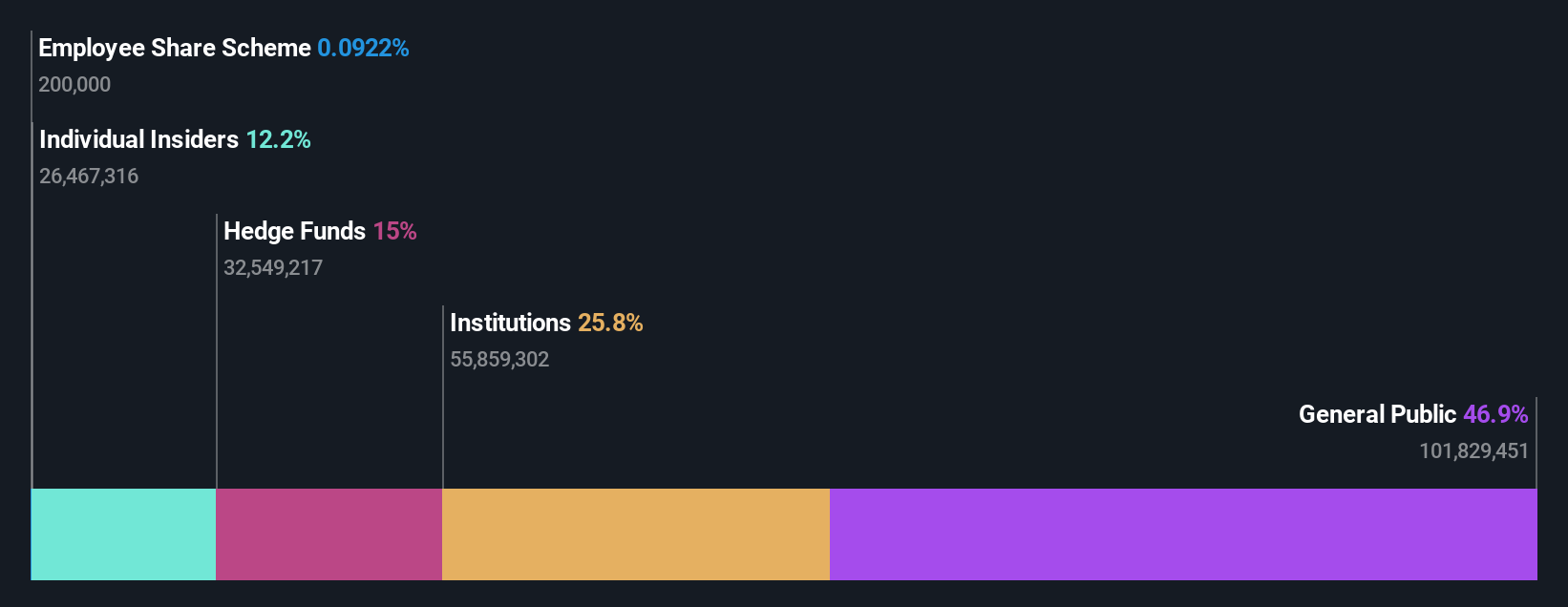

AO World (LSE:AO.)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: AO World plc, along with its subsidiaries, operates as an online retailer of domestic appliances and ancillary services in the United Kingdom and Germany, with a market cap of £596.23 million.

Operations: The company generates revenue of £1.07 billion from its online retailing of domestic appliances and ancillary services in the UK and Germany.

Insider Ownership: 20.9%

Earnings Growth Forecast: 20.2% p.a.

AO World is trading at a substantial discount to its estimated fair value, with earnings projected to grow significantly at 20.24% annually, surpassing the UK market average. Revenue growth is expected at 6% per year, exceeding the market's 3.6%. Recent earnings reports show increased sales and net income compared to last year, alongside revised guidance indicating over 10% growth in B2C Retail revenue for 2024. No recent insider trading activities have been reported.

- Navigate through the intricacies of AO World with our comprehensive analyst estimates report here.

- Upon reviewing our latest valuation report, AO World's share price might be too optimistic.

Gulf Keystone Petroleum (LSE:GKP)

Simply Wall St Growth Rating: ★★★★★★

Overview: Gulf Keystone Petroleum Limited focuses on the exploration, development, and production of oil and gas in the Kurdistan Region of Iraq with a market cap of £296.81 million.

Operations: The company's revenue is derived from its activities in the exploration and production of oil and gas, amounting to $115.15 million.

Insider Ownership: 12.2%

Earnings Growth Forecast: 93.9% p.a.

Gulf Keystone Petroleum is projected to achieve high revenue growth of 35.2% annually, significantly outpacing the UK market average. The company is expected to become profitable within three years, with earnings forecasted to grow by 93.91% per year. Insider confidence is evident with substantial share purchases over the past three months and no significant sales. However, its dividend yield of 10.75% may not be sustainable given current earnings coverage challenges.

- Dive into the specifics of Gulf Keystone Petroleum here with our thorough growth forecast report.

- According our valuation report, there's an indication that Gulf Keystone Petroleum's share price might be on the expensive side.

Key Takeaways

- Click through to start exploring the rest of the 62 Fast Growing UK Companies With High Insider Ownership now.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About LSE:AO.

AO World

Engages in the online retailing of domestic appliances and ancillary services in the United Kingdom and Germany.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Community Narratives