Advertisement

Dollarama (TSE:DOL) Knows How To Allocate Capital

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. With that in mind, the ROCE of Dollarama (TSE:DOL) looks attractive right now, so lets see what the trend of returns can tell us.

What Is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. To calculate this metric for Dollarama, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

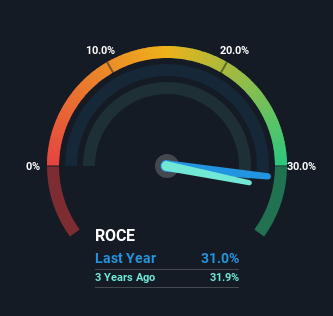

0.31 = CA$1.4b ÷ (CA$5.3b - CA$678m) (Based on the trailing twelve months to January 2024).

Thus, Dollarama has an ROCE of 31%. That's a fantastic return and not only that, it outpaces the average of 11% earned by companies in a similar industry.

Check out our latest analysis for Dollarama

In the above chart we have measured Dollarama's prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free analyst report for Dollarama .

What The Trend Of ROCE Can Tell Us

We'd be pretty happy with returns on capital like Dollarama. The company has employed 62% more capital in the last five years, and the returns on that capital have remained stable at 31%. Now considering ROCE is an attractive 31%, this combination is actually pretty appealing because it means the business can consistently put money to work and generate these high returns. If Dollarama can keep this up, we'd be very optimistic about its future.

The Bottom Line On Dollarama's ROCE

In summary, we're delighted to see that Dollarama has been compounding returns by reinvesting at consistently high rates of return, as these are common traits of a multi-bagger. And the stock has done incredibly well with a 188% return over the last five years, so long term investors are no doubt ecstatic with that result. So while the positive underlying trends may be accounted for by investors, we still think this stock is worth looking into further.

Dollarama does have some risks though, and we've spotted 2 warning signs for Dollarama that you might be interested in.

If you'd like to see other companies earning high returns, check out our free list of companies earning high returns with solid balance sheets here.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:DOL

Dollarama

Operates a chain of stores and provides related logistical and administrative support activities.

Adequate balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

RIO is poised to weather a depressed iron ore environment, but commodity diversification comes with lower margins

Fair Value AU$110.51|4.0% overvalued

DU

Community Contributor

The demand for personalized medicine will keep Thermo Fisher Scientific thriving

Fair Value US$540.27|20.1% undervalued

UN

Community Contributor

Silver Play by A Family with 10x Potential

Fair Value UK£24.00|88.5% undervalued

RO

Community Contributor