- Canada

- /

- Oil and Gas

- /

- TSX:BTE

Top 3 Undervalued Small Caps On TSX With Insider Buying In Canada

Reviewed by Simply Wall St

The Canadian stock market has experienced some recent pullback, with the TSX index down about 6.5% since its peak, amid political uncertainties and shifts in economic policies. Despite this volatility, the backdrop of positive economic growth and easing inflation suggests potential opportunities for investors willing to navigate these challenges. In such an environment, identifying small-cap stocks with strong fundamentals and insider buying can be a strategic approach to uncovering value within the market.

Top 10 Undervalued Small Caps With Insider Buying In Canada

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Sagicor Financial | 1.1x | 0.3x | 37.76% | ★★★★★★ |

| Primaris Real Estate Investment Trust | 12.8x | 3.4x | 43.92% | ★★★★★☆ |

| Calfrac Well Services | 11.6x | 0.2x | 37.67% | ★★★★★☆ |

| Nexus Industrial REIT | 12.5x | 3.1x | 28.87% | ★★★★★☆ |

| Aris Mining | NA | 1.2x | 46.42% | ★★★★★☆ |

| Vermilion Energy | NA | 1.1x | -131.51% | ★★★★☆☆ |

| Baytex Energy | NA | 0.8x | -105.74% | ★★★★☆☆ |

| Minto Apartment Real Estate Investment Trust | NA | 5.5x | 20.68% | ★★★★☆☆ |

| Hemisphere Energy | 5.9x | 2.2x | -104.49% | ★★★☆☆☆ |

| European Residential Real Estate Investment Trust | NA | 2.4x | -210.70% | ★★★☆☆☆ |

Here we highlight a subset of our preferred stocks from the screener.

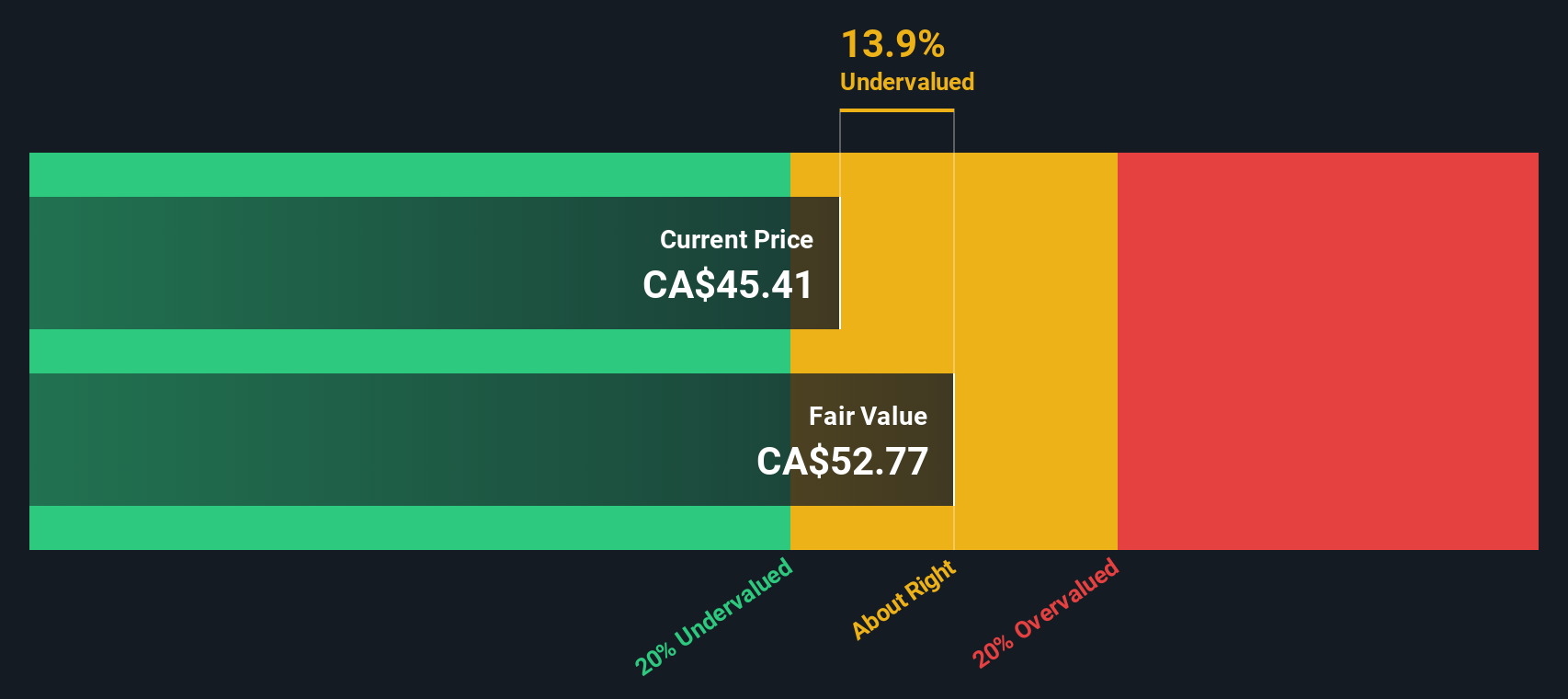

Atrium Mortgage Investment (TSX:AI)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Atrium Mortgage Investment operates as a non-bank lender specializing in providing residential and commercial mortgages, with a market capitalization of approximately CA$0.49 billion.

Operations: The company generates revenue primarily from its financial services, specifically in the mortgage sector, with a reported CA$57.55 million for the latest period. The gross profit margin has shown fluctuations over time, reaching 85.02% in the most recent quarter. Operating expenses include general and administrative costs, which were CA$1.38 million in the same period.

PE: 11.0x

Atrium Mortgage Investment, a Canadian small-cap, has captured attention with its recent 3.3% dividend increase to C$0.93 per share annually, signaling confidence in its financial health despite high debt levels. Earnings for Q3 2024 showed resilience with net income rising to C$11.61 million from C$10.99 million year-over-year, though revenue slightly dipped to C$24.51 million from C$25.41 million. Notably, insider confidence is reflected in share purchases during the past year, hinting at potential growth prospects amidst external borrowing risks.

- Unlock comprehensive insights into our analysis of Atrium Mortgage Investment stock in this valuation report.

Learn about Atrium Mortgage Investment's historical performance.

Badger Infrastructure Solutions (TSX:BDGI)

Simply Wall St Value Rating: ★★★★★★

Overview: Badger Infrastructure Solutions specializes in providing non-destructive excavating services, with a market cap of approximately $1.19 billion CAD.

Operations: Badger Infrastructure Solutions generates revenue primarily from its Non-Destructive Excavating Services, with recent figures reaching $730.92 million. The company's cost of goods sold (COGS) was reported at $522.81 million, leading to a gross profit margin of 28.47%. Operating expenses include significant allocations for depreciation and amortization, which amounted to $77.32 million in the latest period.

PE: 20.6x

Badger Infrastructure Solutions, a Canadian company with a small market capitalization, has seen insider confidence with recent share purchases. From July to September 2024, the company repurchased 44,400 shares for C$1.64 million. Despite high debt levels and reliance on external borrowing, Badger's third-quarter sales rose to US$209 million from US$196 million the previous year. The appointment of George Williams to their board in January 2025 could enhance strategic direction given his extensive industry experience.

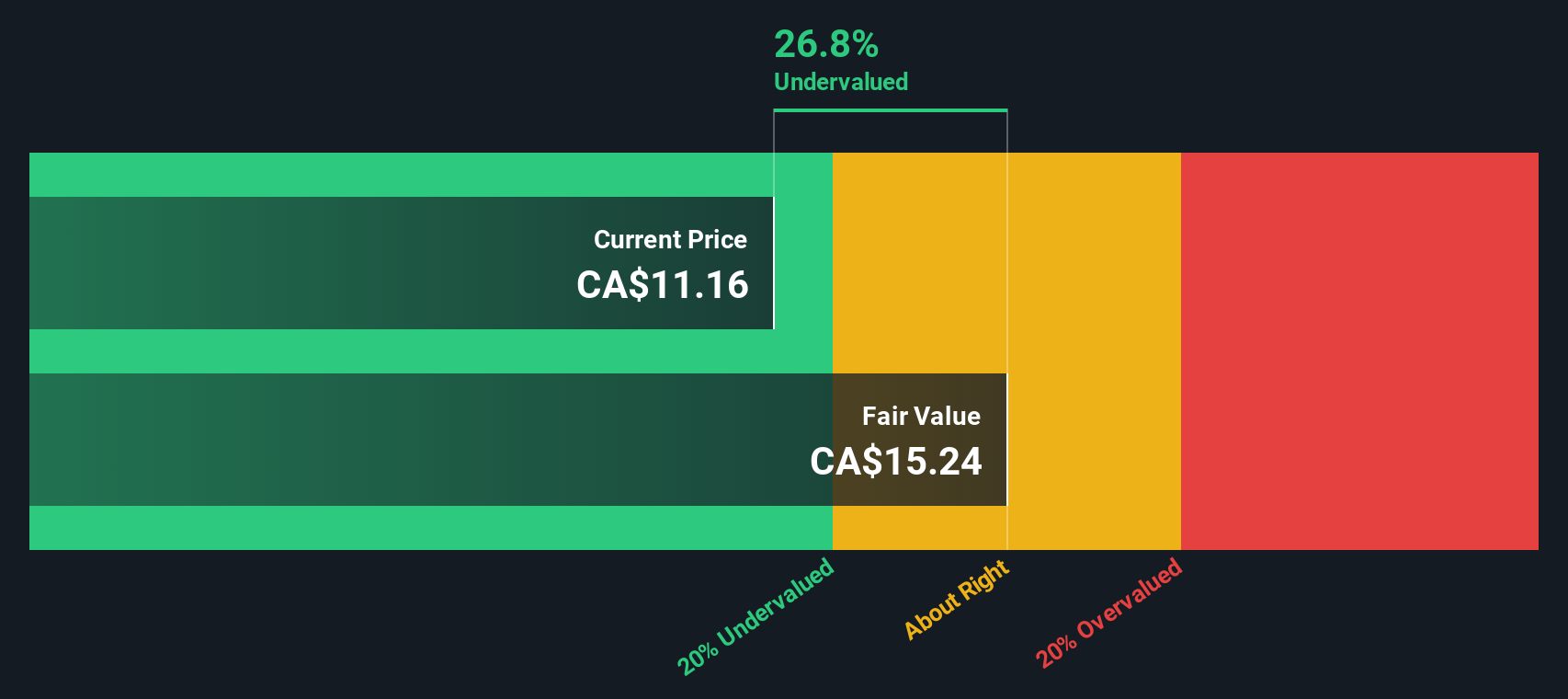

Baytex Energy (TSX:BTE)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Baytex Energy is a Canadian oil and gas company focused on exploration and production, with a market cap of approximately CA$3.12 billion.

Operations: The company generates revenue primarily from oil and gas exploration and production, with recent figures showing CA$3.36 billion in revenue. The gross profit margin has shown fluctuations, reaching 68.54% recently, indicating varying profitability levels over time. Operating expenses have been significant, impacting net income results across different periods.

PE: -7.8x

Baytex Energy, a Canadian energy player, showcases potential value with its projected 30% annual earnings growth. Despite relying solely on external borrowing for funding, which poses higher risk, the company continues to draw attention. Recent insider confidence is evident as they increased their holdings over recent months. The firm repurchased 17.6 million shares for C$82.37 million by September 2024 and anticipates production between 150,000 to 154,000 boe/d in 2025.

- Click to explore a detailed breakdown of our findings in Baytex Energy's valuation report.

Gain insights into Baytex Energy's historical performance by reviewing our past performance report.

Turning Ideas Into Actions

- Discover the full array of 23 Undervalued TSX Small Caps With Insider Buying right here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechValuation is complex, but we're here to simplify it.

Discover if Baytex Energy might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:BTE

Baytex Energy

An energy company, engages in the acquisition, development, and production of crude oil and natural gas in the Western Canadian Sedimentary Basin and in the Eagle Ford, the United States.

Fair value with acceptable track record.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Hitit Bilgisayar Hizmetleri will achieve a 19.7% revenue boost in the next five years

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)