- United States

- /

- Renewable Energy

- /

- NYSE:VST

Vistra (VST) Valuation Check as Credit Upgrade and New Gas Projects Draw Fresh Investor Focus

Reviewed by Simply Wall St

Vistra (VST) is back in the spotlight after a flurry of bullish catalysts, from an S&P Global credit upgrade to new natural gas projects aimed at feeding power hungry data centers and AI growth.

See our latest analysis for Vistra.

Those catalysts are landing against a choppy backdrop, with the share price at $170.1 after a recent pullback that left the 90 day share price return at negative 18.88 percent. However, the year to date share price return of 13.66 percent and especially the five year total shareholder return of 970.11 percent suggest longer term momentum is still firmly intact as investors reassess Vistra’s growth and risk profile.

If Vistra’s surge on data center power demand has your attention, it could be a good moment to explore aerospace and defense stocks as another corner of the market where critical infrastructure themes are reshaping return potential.

With earnings estimates inflecting higher and the stock still trading at a steep discount to Wall Street targets, is Vistra quietly undervalued here? Or are markets already baking in years of AI powered growth, leaving little upside?

Most Popular Narrative Narrative: 26.3% Undervalued

Compared with Vistra’s last close at $170.10, the most followed narrative pins fair value materially higher, pointing to powerful earnings and margin expansion ahead.

Analysts expect earnings to reach $3.4 billion (and earnings per share of $10.94) by about September 2028, up from $2.2 billion today. However, there is some disagreement amongst the analysts with the more bearish ones expecting earnings as low as $2.6 billion.

Want to see what kind of revenue runway and margin lift could justify that profit jump, and the bold future profit multiple behind it? The narrative lays out an aggressive growth path, granular earnings milestones, and a valuation framework that treats Vistra less like a slow moving utility and more like a high growth infrastructure platform. Curious which assumptions really carry the model, and how sensitive that fair value is if they slip? Dive in to unpack the full playbook behind this price target.

Result: Fair Value of $230.71 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, heavy leverage from acquisitions and regulatory uncertainty around fossil assets could quickly challenge today’s optimistic growth and valuation assumptions.

Find out about the key risks to this Vistra narrative.

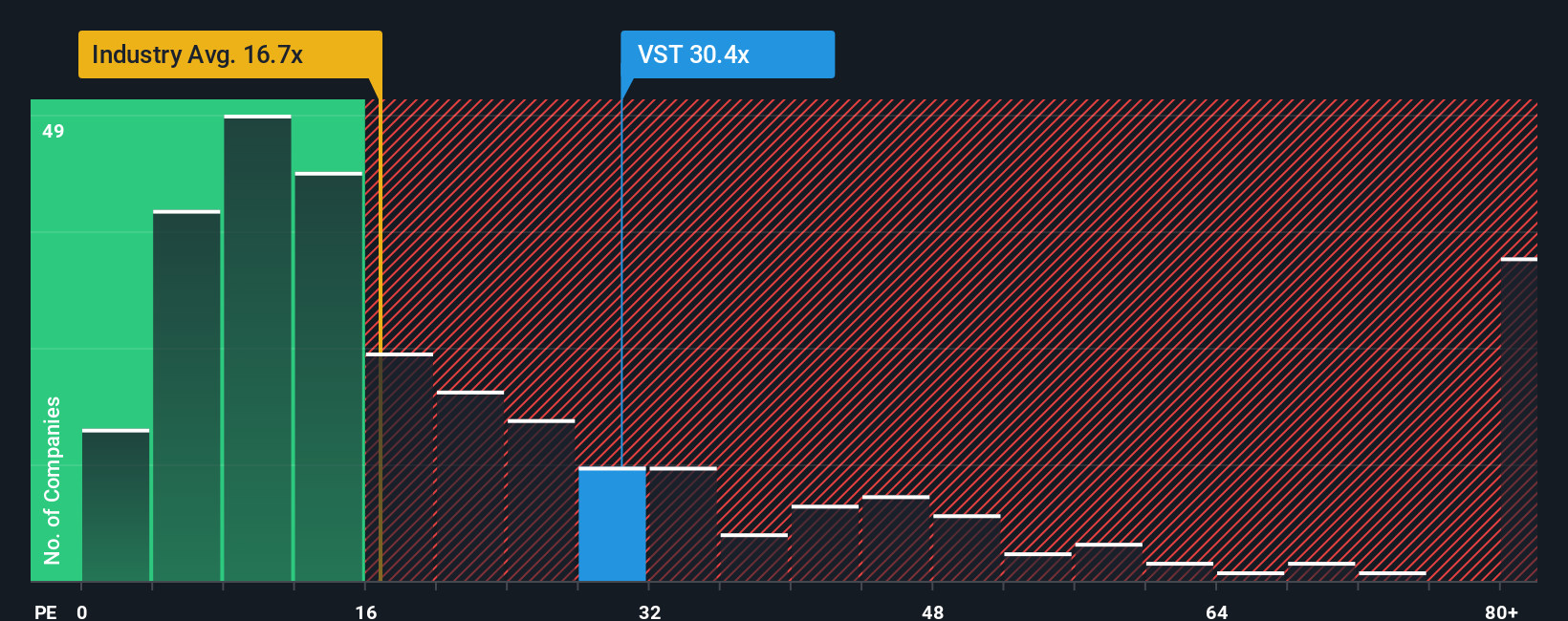

Another Angle on Valuation

Those bullish fair value numbers look generous next to how the market is actually pricing Vistra today. On a price to earnings basis, shares trade around 60 times earnings versus about 29.3 times for peers and 16.6 times for the wider renewable energy space, and even above a fair ratio of 47.7 times. That premium signals investors are already paying up for a lot of growth, so the question is how much margin for error is really left.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Vistra Narrative

If you are not fully convinced by this view, or you would rather dig into the numbers yourself, you can build a personalized narrative in just a few minutes: Do it your way

A great starting point for your Vistra research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, consider building a stronger watchlist by scanning focused opportunities across themes that could play a role in shaping your returns over the next few years.

- Explore income potential with these 13 dividend stocks with yields > 3% that can help anchor your portfolio with cash flows while markets stay volatile.

- Evaluate opportunities in innovation by assessing these 26 AI penny stocks positioned at the front line of artificial intelligence adoption and monetization.

- Refine your value strategy by reviewing these 907 undervalued stocks based on cash flows where current prices may differ from the underlying cash flow profile.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:VST

Vistra

Operates as an integrated retail electricity and power generation company in the United States.

Reasonable growth potential with low risk.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)