Advertisement

- United States

- /

- Software

- /

- NYSE:SMAR

Three Value Stocks Estimated To Be Discounted Between 11% And 49.6%

Simply Wall St

Reviewed by Simply Wall St

As global markets exhibit mixed performances with notable shifts towards value and small-cap stocks, investors are keenly observing these movements for potential opportunities. In this context, identifying undervalued stocks becomes particularly compelling, offering a strategic avenue for those looking to capitalize on market inefficiencies during times of economic recalibration and sector rotations.

Top 10 Undervalued Stocks Based On Cash Flows

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| UMB Financial (NasdaqGS:UMBF) | US$94.71 | US$189.13 | 49.9% |

| Fenix Resources (ASX:FEX) | A$0.385 | A$0.77 | 49.9% |

| MaxiPARTS (ASX:MXI) | A$2.00 | A$3.99 | 49.9% |

| Truecaller (OM:TRUE B) | SEK35.66 | SEK71.28 | 50% |

| NSE (ENXTPA:ALNSE) | €25.50 | €50.92 | 49.9% |

| Sachem Capital (NYSEAM:SACH) | US$2.61 | US$5.21 | 49.9% |

| Fluence Energy (NasdaqGS:FLNC) | US$15.96 | US$31.80 | 49.8% |

| Super Hi International Holding (SEHK:9658) | HK$12.92 | HK$25.84 | 50% |

| Zijin Mining Group (SEHK:2899) | HK$16.20 | HK$32.32 | 49.9% |

| TF Bank (OM:TFBANK) | SEK260.00 | SEK518.39 | 49.8% |

Let's explore several standout options from the results in the screener.

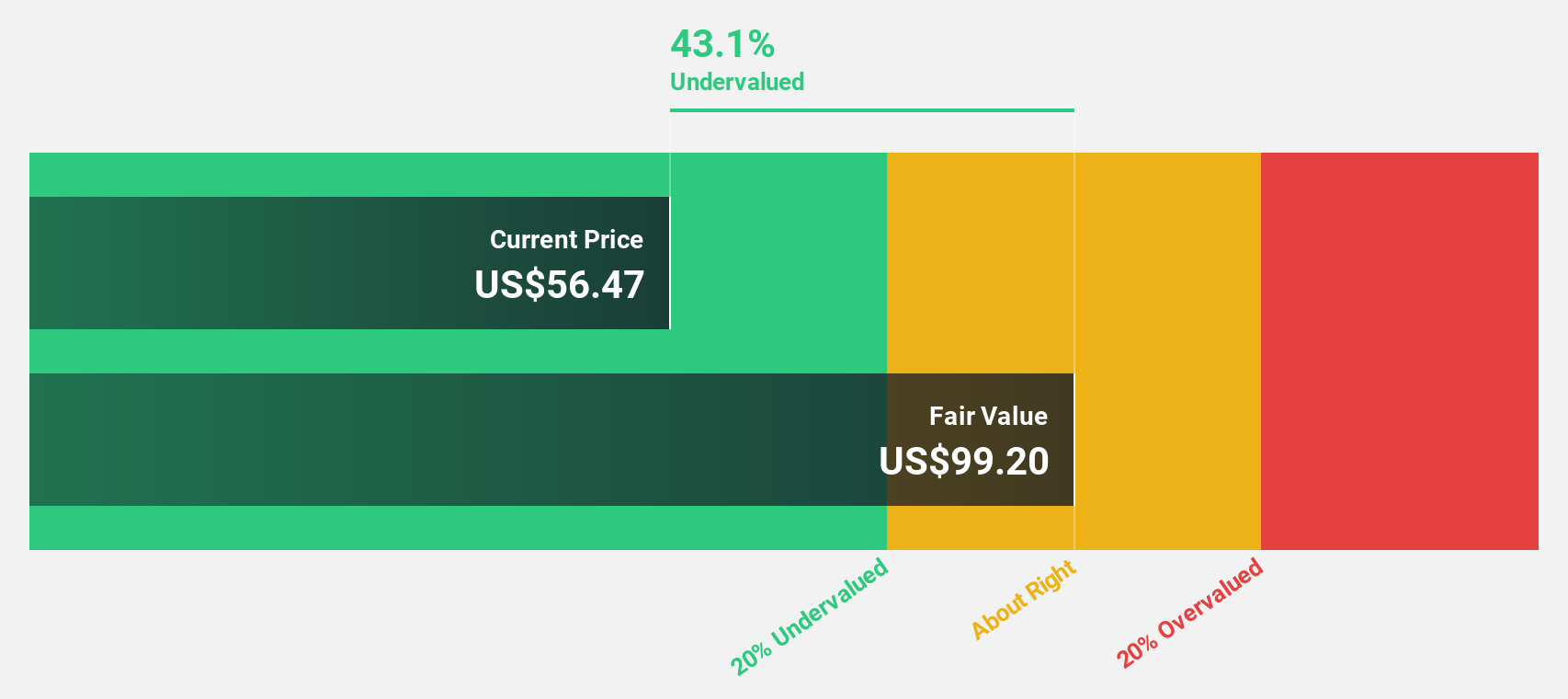

HubSpot (NYSE:HUBS)

Overview: HubSpot, Inc. operates globally, offering a cloud-based CRM platform to businesses across the Americas, Europe, and Asia Pacific, with a market capitalization of approximately $24.45 billion.

Operations: The company generates its revenue primarily from its Internet Software & Services segment, totaling approximately $2.29 billion.

Estimated Discount To Fair Value: 11%

HubSpot, recently in the spotlight due to halted acquisition talks with Alphabet, remains a compelling case for cash flow-based valuation. Despite the market's initial negative reaction to the news, dropping share prices by 12%, HubSpot shows resilience with a strong financial forecast. The company is expected to grow its revenue by 15.3% annually and become profitable within three years, surpassing average market growth rates. Currently trading at US$479.82—below its estimated fair value of US$539.29—HubSpot presents an undervalued opportunity based on its future cash flows and profitability prospects.

- Insights from our recent growth report point to a promising forecast for HubSpot's business outlook.

- Click here and access our complete balance sheet health report to understand the dynamics of HubSpot.

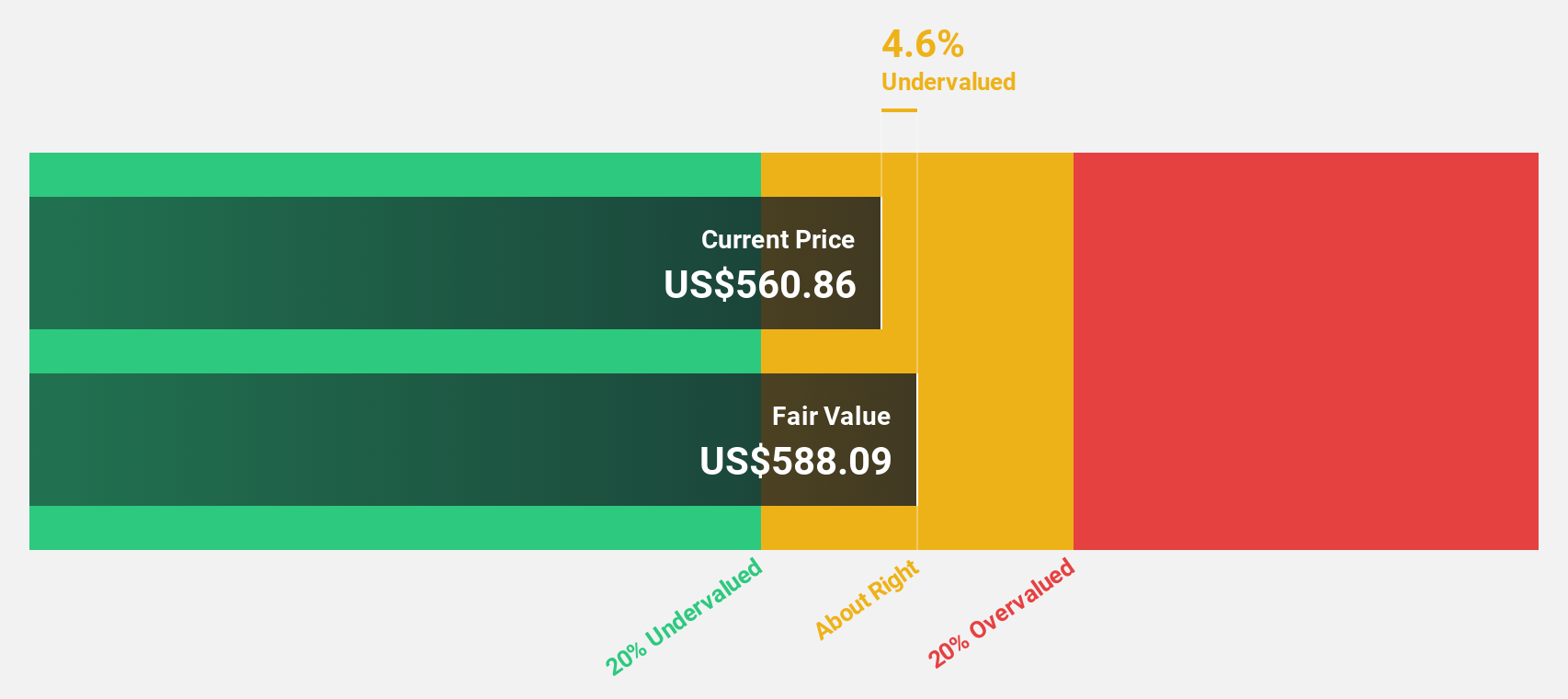

Smartsheet (NYSE:SMAR)

Overview: Smartsheet Inc. operates as an enterprise platform that helps teams and organizations plan, capture, manage, automate, and report on work, with a market capitalization of approximately $6.68 billion.

Operations: The company generates its revenue primarily from the Internet Software & Services segment, totaling approximately $1.00 billion.

Estimated Discount To Fair Value: 49.6%

Smartsheet, with a current price of US$48.29, is significantly undervalued by 49.6%, assessed against a fair value estimate of US$95.82. This valuation discrepancy highlights its potential despite recent financial results showing a narrowed net loss to US$8.86 million from last year's US$29.87 million on revenues of US$262.98 million, up from US$219.89 million. Forecasts suggest robust growth with expected revenue increases and profitability within three years, backed by innovations like new AI features enhancing enterprise decision-making capabilities.

- Our expertly prepared growth report on Smartsheet implies its future financial outlook may be stronger than recent results.

- Click to explore a detailed breakdown of our findings in Smartsheet's balance sheet health report.

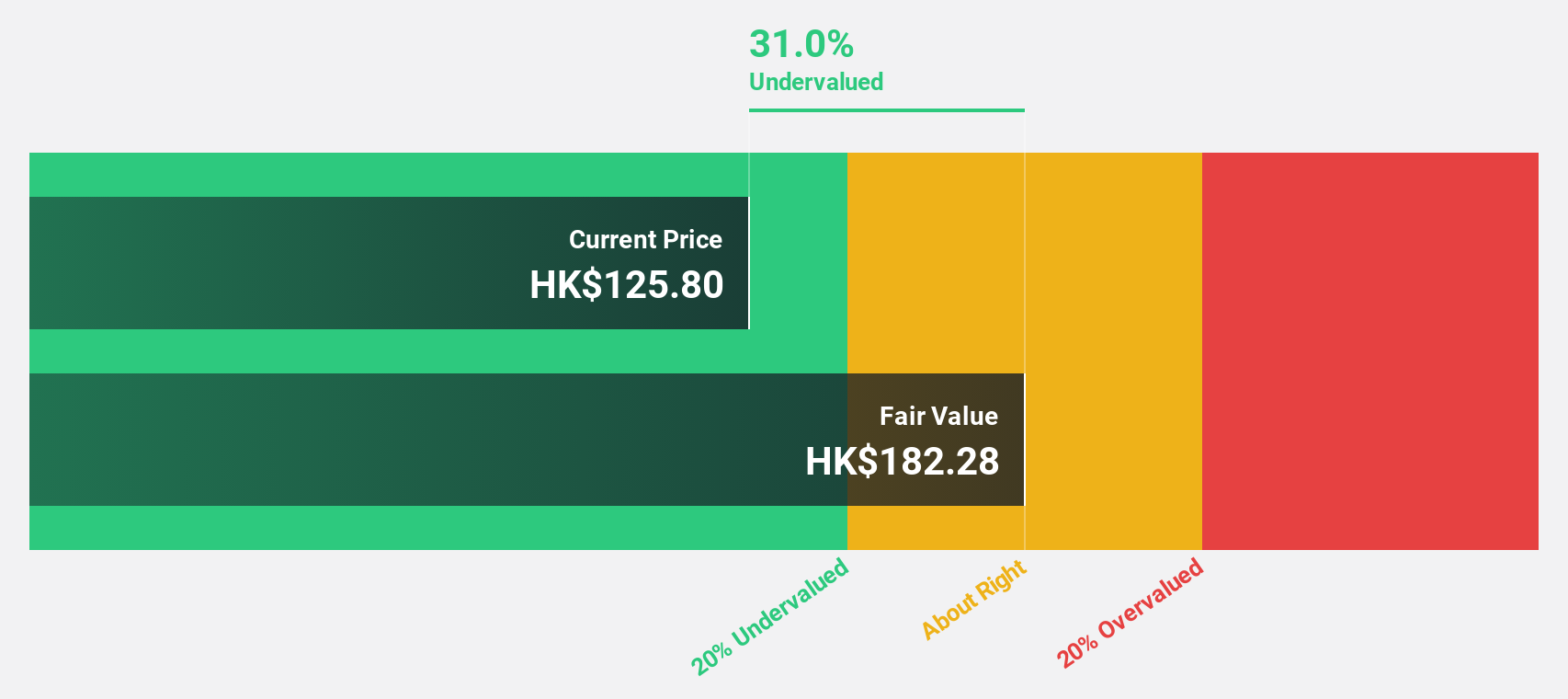

BYD (SEHK:1211)

Overview: BYD Company Limited operates in the automobile and battery sectors across China, Hong Kong, Macau, Taiwan, and internationally, with a market capitalization of approximately HK$779.12 billion.

Operations: The company's revenue is primarily derived from its automobile and battery sectors.

Estimated Discount To Fair Value: 47%

BYD's recent operational achievements, including the inauguration of its Thailand plant and robust sales growth, underscore its strategic expansion and market penetration. Despite trading below our fair value estimate by over 20% at HK$246, with a calculated fair value of HK$464.53, BYD exhibits strong fundamentals with revenue forecasted to grow at 14.2% annually—outpacing the Hong Kong market's 7.8%. However, earnings are expected to grow moderately by 15.3% per year, indicating potential yet tempered profitability enhancements ahead.

- Our earnings growth report unveils the potential for significant increases in BYD's future results.

- Unlock comprehensive insights into our analysis of BYD stock in this financial health report.

Key Takeaways

- Reveal the 984 hidden gems among our Undervalued Stocks Based On Cash Flows screener with a single click here.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:SMAR

Smartsheet

Provides enterprise platform to plan, capture, manage, automate, and report on work for teams and organizations.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor