- United States

- /

- IT

- /

- NYSE:DAVA

Endava plc Just Beat EPS By 23%: Here's What Analysts Think Will Happen Next

Endava plc (NYSE:DAVA) just released its quarterly report and things are looking bullish. The company beat both earnings and revenue forecasts, with revenue of UK£169m, some 4.2% above estimates, and statutory earnings per share (EPS) coming in at UK£0.35, 23% ahead of expectations. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

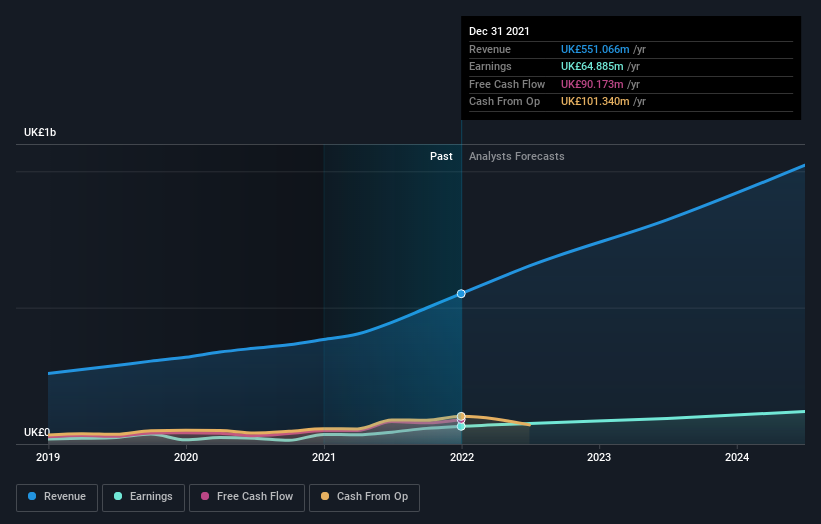

View our latest analysis for Endava

Taking into account the latest results, the consensus forecast from Endava's eight analysts is for revenues of UK£821.7m in 2023, which would reflect a major 49% improvement in sales compared to the last 12 months. Per-share earnings are expected to soar 33% to UK£1.55. Yet prior to the latest earnings, the analysts had been anticipated revenues of UK£797.8m and earnings per share (EPS) of UK£1.49 in 2023. It looks like there's been a modest increase in sentiment following the latest results, withthe analysts becoming a bit more optimistic in their predictions for both revenues and earnings.

Despite these upgrades, the consensus price target fell 17% to US$137, perhaps signalling that the uplift in performance is not expected to last. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. There are some variant perceptions on Endava, with the most bullish analyst valuing it at US$180 and the most bearish at US$94.04 per share. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. The analysts are definitely expecting Endava's growth to accelerate, with the forecast 38% annualised growth to the end of 2023 ranking favourably alongside historical growth of 24% per annum over the past three years. Compare this with other companies in the same industry, which are forecast to grow their revenue 13% annually. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect Endava to grow faster than the wider industry.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around Endava's earnings potential next year. Pleasantly, they also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow faster than the wider industry. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Endava's future valuation.

With that in mind, we wouldn't be too quick to come to a conclusion on Endava. Long-term earnings power is much more important than next year's profits. We have forecasts for Endava going out to 2024, and you can see them free on our platform here.

Before you take the next step you should know about the 2 warning signs for Endava that we have uncovered.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Endava might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:DAVA

Endava

Provides technology services in North America, Europe, the United Kingdom, and internationally.

Undervalued with proven track record.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Stride Stock: Online Education Finds Its Second Act

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)