- United States

- /

- Software

- /

- NYSE:CRM

Results: Salesforce, Inc. Beat Earnings Expectations And Analysts Now Have New Forecasts

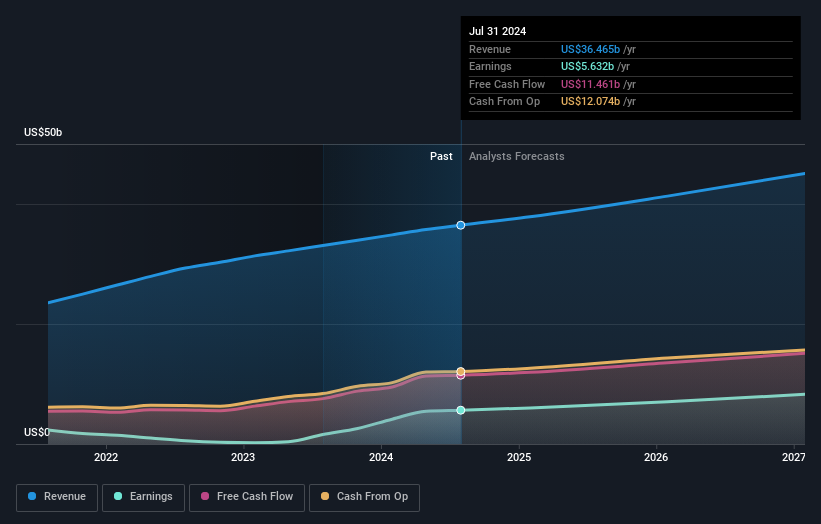

Salesforce, Inc. (NYSE:CRM) shareholders are probably feeling a little disappointed, since its shares fell 4.7% to US$253 in the week after its latest second-quarter results. The result was positive overall - although revenues of US$9.3b were in line with what the analysts predicted, Salesforce surprised by delivering a statutory profit of US$1.47 per share, modestly greater than expected. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

View our latest analysis for Salesforce

Taking into account the latest results, the most recent consensus for Salesforce from 46 analysts is for revenues of US$37.9b in 2025. If met, it would imply a satisfactory 3.8% increase on its revenue over the past 12 months. Per-share earnings are expected to rise 3.9% to US$6.12. In the lead-up to this report, the analysts had been modelling revenues of US$37.9b and earnings per share (EPS) of US$6.06 in 2025. So it's pretty clear that, although the analysts have updated their estimates, there's been no major change in expectations for the business following the latest results.

The analysts reconfirmed their price target of US$307, showing that the business is executing well and in line with expectations. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. The most optimistic Salesforce analyst has a price target of US$390 per share, while the most pessimistic values it at US$236. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the Salesforce's past performance and to peers in the same industry. We would highlight that Salesforce's revenue growth is expected to slow, with the forecast 7.8% annualised growth rate until the end of 2025 being well below the historical 17% p.a. growth over the last five years. Compare this against other companies (with analyst forecasts) in the industry, which are in aggregate expected to see revenue growth of 12% annually. So it's pretty clear that, while revenue growth is expected to slow down, the wider industry is also expected to grow faster than Salesforce.

The Bottom Line

The most obvious conclusion is that there's been no major change in the business' prospects in recent times, with the analysts holding their earnings forecasts steady, in line with previous estimates. On the plus side, there were no major changes to revenue estimates; although forecasts imply they will perform worse than the wider industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for Salesforce going out to 2027, and you can see them free on our platform here..

And what about risks? Every company has them, and we've spotted 1 warning sign for Salesforce you should know about.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:CRM

Salesforce

Provides customer relationship management technology that connects companies and customers together worldwide.

Good value with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

Butler National (Buks) outperforms.

A tech powerhouse quietly powering the world’s AI infrastructure.

Keppel DC REIT (SGX: AJBU) is a resilient gem in the data center space.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)