Advertisement

- United States

- /

- Software

- /

- NasdaqCM:SNCR

Synchronoss Technologies (NASDAQ:SNCR) Seems To Be Using A Lot Of Debt

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Synchronoss Technologies, Inc. (NASDAQ:SNCR) does carry debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Synchronoss Technologies

What Is Synchronoss Technologies's Debt?

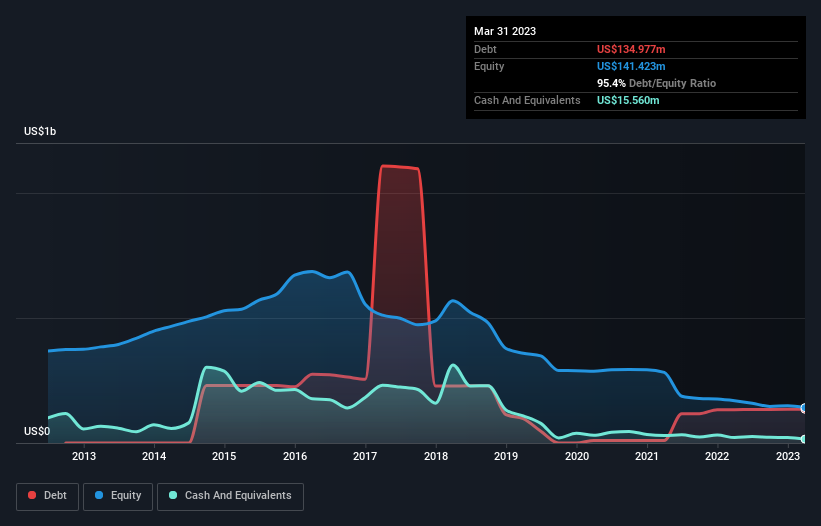

The chart below, which you can click on for greater detail, shows that Synchronoss Technologies had US$135.0m in debt in March 2023; about the same as the year before. However, it also had US$15.6m in cash, and so its net debt is US$119.4m.

A Look At Synchronoss Technologies' Liabilities

Zooming in on the latest balance sheet data, we can see that Synchronoss Technologies had liabilities of US$83.1m due within 12 months and liabilities of US$166.8m due beyond that. Offsetting these obligations, it had cash of US$15.6m as well as receivables valued at US$52.0m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$182.3m.

This deficit casts a shadow over the US$87.4m company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. After all, Synchronoss Technologies would likely require a major re-capitalisation if it had to pay its creditors today.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Synchronoss Technologies shareholders face the double whammy of a high net debt to EBITDA ratio (8.7), and fairly weak interest coverage, since EBIT is just 0.051 times the interest expense. This means we'd consider it to have a heavy debt load. However, the silver lining was that Synchronoss Technologies achieved a positive EBIT of US$685k in the last twelve months, an improvement on the prior year's loss. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Synchronoss Technologies's ability to maintain a healthy balance sheet going forward. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So it is important to check how much of its earnings before interest and tax (EBIT) converts to actual free cash flow. Over the last year, Synchronoss Technologies reported free cash flow worth 16% of its EBIT, which is really quite low. For us, cash conversion that low sparks a little paranoia about is ability to extinguish debt.

Our View

To be frank both Synchronoss Technologies's interest cover and its track record of staying on top of its total liabilities make us rather uncomfortable with its debt levels. Having said that, its ability to grow its EBIT isn't such a worry. After considering the datapoints discussed, we think Synchronoss Technologies has too much debt. That sort of riskiness is ok for some, but it certainly doesn't float our boat. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 2 warning signs for Synchronoss Technologies that you should be aware of before investing here.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:SNCR

Synchronoss Technologies

Provides white label cloud software and services in North America, Europe, the Middle East, Africa, and the Asia Pacific.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Gain Therapeutics ·

The Market Is Sleeping on This Parkinson's Biotech - And I Think That's a Mistake

Fair Value:US$7.672.0% undervalued

40 followersusers have followed this narrative

2 commentsusers have commented on this narrative

20 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.233.8% undervalued

63 followersusers have followed this narrative

1 commentusers have commented on this narrative

21 likesusers have liked this narrative

TE

TechMegaTrends on Bambuser ·

Bambuser is today the only listed company in Europe that simultaneously possesses an 85% gross margin, proprietary AI infrastructure for the

Fair Value:SEK 238.2685.7% undervalued

35 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

HE

HedgeY on Constellium ·

Constellium jet another cyclical aluminum processor, or a mispriced aluminum platform?

Fair Value:US$3410.9% undervalued

9 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

CE

Ceazar on Sparc Al ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2533.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

ES

Esteban on MSCI ·

MSCI 04-2026

Fair Value:US$267112.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WI

WIn2026 on CoreWeave ·

Deep Dive: Assessing the Sustainability of CRWV’s Compute-as-a-Service Model

Fair Value:US$7067.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TR

tripledub on Microsoft ·

Everyone's Terrified Microsoft Will Keep Spending. I'm Terrified They'll Stop.

Fair Value:US$3955.8% overvalued

52 followersusers have followed this narrative

3 commentsusers have commented on this narrative

43 likesusers have liked this narrative

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.233.8% undervalued

63 followersusers have followed this narrative

1 commentusers have commented on this narrative

21 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$579.5727.9% undervalued

1372 followersusers have followed this narrative

2 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Trending Discussion

GT

GT1 on Gulf Keystone Petroleum ·

Have been in and out of this one and Genel for years. I think that delayed and non payments are a bi...

0

|0