Advertisement

- United States

- /

- Software

- /

- NasdaqCM:RNWK

This Broker Just Slashed Their RealNetworks, Inc. (NASDAQ:RNWK) Earnings Forecasts

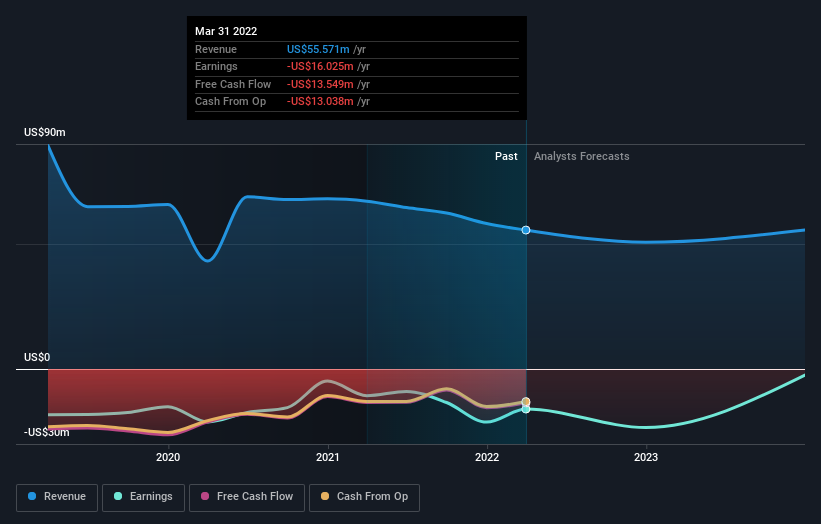

Market forces rained on the parade of RealNetworks, Inc. (NASDAQ:RNWK) shareholders today, when the covering analyst downgraded their forecasts for this year. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting the analyst has soured majorly on the business. Bidders are definitely seeing a different story, with the stock price of US$0.56 reflecting a 13% rise in the past week. Whether the downgrade will have a negative impact on demand for shares is yet to be seen.

After the downgrade, the consensus from RealNetworks' solo analyst is for revenues of US$51m in 2022, which would reflect a chunky 8.8% decline in sales compared to the last year of performance. Per-share losses are expected to explode, reaching US$0.50 per share. However, before this estimates update, the consensus had been expecting revenues of US$59m and US$0.35 per share in losses. So there's been quite a change-up of views after the recent consensus updates, with the analyst making a serious cut to their revenue forecasts while also expecting losses per share to increase.

View our latest analysis for RealNetworks

The consensus price target fell 25% to US$3.00, implicitly signalling that lower earnings per share are a leading indicator for RealNetworks' valuation.

Of course, another way to look at these forecasts is to place them into context against the industry itself. Over the past five years, revenues have declined around 3.5% annually. Worse, forecasts are essentially predicting the decline to accelerate, with the estimate for an annualised 12% decline in revenue until the end of 2022. Compare this against analyst estimates for companies in the broader industry, which suggest that revenues (in aggregate) are expected to grow 14% annually. So while a broad number of companies are forecast to grow, unfortunately RealNetworks is expected to see its sales affected worse than other companies in the industry.

The Bottom Line

The most important thing to take away is that the analyst increased their loss per share estimates for this year. Unfortunately the analyst also downgraded their revenue estimates, and industry data suggests that RealNetworks' revenues are expected to grow slower than the wider market. After such a stark change in sentiment from the analyst, we'd understand if readers now felt a bit wary of RealNetworks.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. At least one analyst has provided forecasts out to 2023, which can be seen for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:RNWK

RealNetworks

RealNetworks, Inc. provides digital media software and services in the United States, Europe, and internationally.

Adequate balance sheet and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Conexeu Sciences ·

This small biotech is developing technology that could potentially change how tissue is rebuilt

Fair Value:US$25.3451.9% undervalued

50 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

HE

HedgeY on Quanta Services ·

The Picks-and-Shovels Leader of the Grid Supercycle

Fair Value:US$7104.2% overvalued

52 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

FU

FundamentalFlow on Karman Holdings ·

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Fair Value:US$105.654.8% undervalued

34 followersusers have followed this narrative

2 commentsusers have commented on this narrative

16 likesusers have liked this narrative

DO

Double_Bubbler on Invinity Energy Systems ·

Invinity Energy Systems: All About That BESS

Fair Value:UK£161.9% undervalued

40 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

JA

Jacobm2488123 on Netflix ·

Netflix's Revenue Surge Will Hit 18% Despite Market Lows

Fair Value:US$115.9137.1% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BR

browser on Space Exploration Technologies ·

SpaceX: A Sober Look at Catalysts, Risks, and Long‑Term Value After the IPO

Fair Value:US$0.4633.5k% overvalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Abitibi Metals ·

Abitibi Metals’ High-Grade B26 Polymetallic Deposit Trading at a Fraction of Peers, 96% Undervalued?

Fair Value:CA$1.2949.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7443.8% undervalued

67 followersusers have followed this narrative

0 commentsusers have commented on this narrative

16 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9639.1% undervalued

61 followersusers have followed this narrative

9 commentsusers have commented on this narrative

17 likesusers have liked this narrative

HE

HedgeY on AST SpaceMobile ·

AST SpaceMobile: The Boldest Direct-to-Cell Bet in Public Markets

Fair Value:US$17056.9% undervalued

51 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative