- United States

- /

- Diversified Financial

- /

- NasdaqCM:PAYS

Earnings Update: Here's Why Analysts Just Lifted Their PaySign, Inc. (NASDAQ:PAYS) Price Target To US$3.75

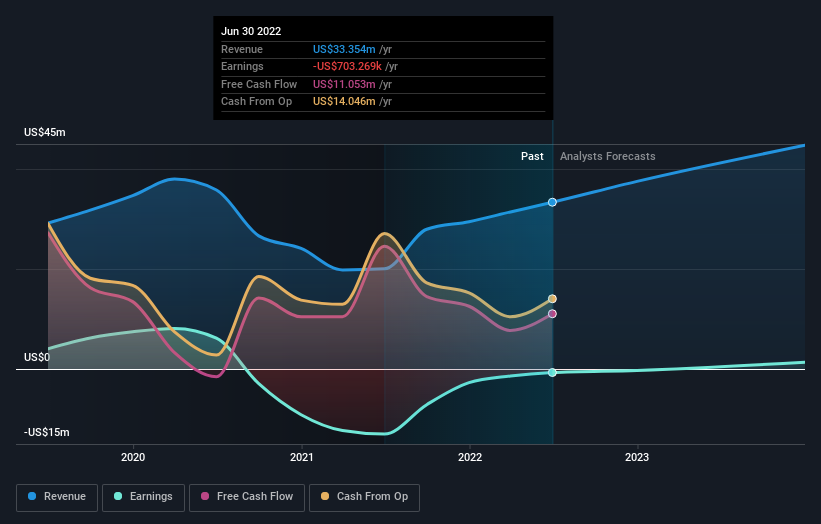

It's been a pretty great week for PaySign, Inc. (NASDAQ:PAYS) shareholders, with its shares surging 18% to US$2.48 in the week since its latest quarterly results. PaySign's revenues suffered a miss, falling 2.6% short of forecasts, at US$8.6m. Statutory earnings per share (EPS) however performed much better, reaching break-even. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we collected the latest post-earnings statutory consensus estimates to see what could be in store for next year.

See our latest analysis for PaySign

Taking into account the latest results, the current consensus from PaySign's four analysts is for revenues of US$37.5m in 2022, which would reflect a decent 12% increase on its sales over the past 12 months. The loss per share is expected to greatly reduce in the near future, narrowing 75% to US$0.0033. Before this earnings announcement, the analysts had been modelling revenues of US$37.0m and losses of US$0.015 per share in 2022. While the revenue estimates were largely unchanged, sentiment seems to have improved, with the analysts upgrading revenues and making a very favorable reduction to losses per share in particular.

The average price target rose 8.7% to US$3.75, with the analysts signalling that the forecast reduction in losses would be a positive for the stock's valuation. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on PaySign, with the most bullish analyst valuing it at US$4.00 and the most bearish at US$3.50 per share. Even so, with a relatively close grouping of estimates, it looks like the analysts are quite confident in their valuations, suggesting PaySign is an easy business to forecast or the the analysts are all using similar assumptions.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's clear from the latest estimates that PaySign's rate of growth is expected to accelerate meaningfully, with the forecast 27% annualised revenue growth to the end of 2022 noticeably faster than its historical growth of 12% p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 12% per year. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect PaySign to grow faster than the wider industry.

The Bottom Line

The most obvious conclusion is that the analysts made no changes to their forecasts for a loss next year. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

With that in mind, we wouldn't be too quick to come to a conclusion on PaySign. Long-term earnings power is much more important than next year's profits. We have estimates - from multiple PaySign analysts - going out to 2023, and you can see them free on our platform here.

Don't forget that there may still be risks. For instance, we've identified 1 warning sign for PaySign that you should be aware of.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:PAYS

Paysign

Provides prepaid card programs, comprehensive patient affordability offerings, digital banking services, and integrated payment processing services for businesses, consumers, and government institutions.

Flawless balance sheet with reasonable growth potential.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)