- United States

- /

- Software

- /

- NasdaqGS:DOCU

DocuSign (DOCU) Advances Government Solutions with FedRAMP Authorized Intelligent Agreement Platform

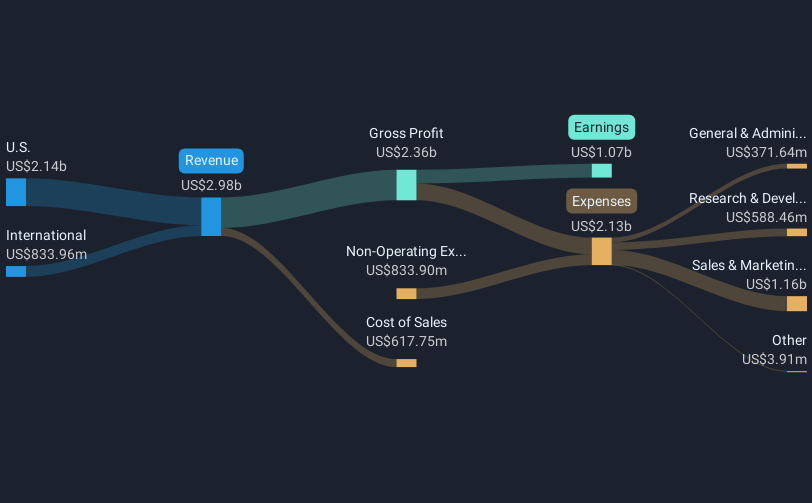

DocuSign (DOCU) has recently achieved a significant milestone by securing FedRAMP Moderate authorization for its Intelligent Agreement Management platform, aiding compliance and efficiency in government contracts. This development aligns with the company's strategy to strengthen ties with public sector entities, positioning them as an ideal partner for modernization. Amidst this backdrop, DocuSign's share price rose by 13% over the past month, mirroring a broader positive market sentiment as both the Nasdaq and S&P 500 hit record highs. The company's strong performance could be further buoyed by ongoing technology sector gains, propelled by investor optimism regarding Fed rate cuts.

DocuSign has 1 risk we think you should know about.

The recent FedRAMP Moderate authorization for DocuSign's Intelligent Agreement Management platform is poised to bolster its strategy of strengthening public sector ties. This development aligns well with the company's focus on expanding its digital workflows, especially within government contracts. By enhancing compliance and efficiency, this approval could catalyze an uptick in long-term revenue and earnings forecasts, given the persistent demand for secure, compliant digital solutions across sectors.

Over the past three years, DocuSign's total shareholder return, including dividends, was 41.98%. This solid performance reflects the company's capacity to capitalize on evolving digital needs despite market fluctuations. In the past year, DocuSign exceeded both the broader US market's 18.5% return and the US Software industry's 25.9% return, underscoring its resilience and strategic execution within a competitive arena.

With the current share price at US$80.19 and facing a 16.91% discount to the consensus price target of US$93.75, there remains potential for future gains. However, analysts expect moderate growth in revenue and profitability, with significant variance in predictions, indicating potential volatility. The recent FedRAMP authorization could impact these forecasts positively, pushing DocuSign closer to or beyond these targets, contingent upon the effective integration and utilization of its solutions in governmental contracts.

The valuation report we've compiled suggests that DocuSign's current price could be inflated.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DOCU

DocuSign

Provides electronic signature solution in the United States and internationally.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Weekly Picks

This small biotech is developing technology that could potentially change how tissue is rebuilt

The Picks-and-Shovels Leader of the Grid Supercycle

KRMN — Karman Space & Defense: Down 58% from Peak, Is the Market Mispricing a Hypergrowth Defense Compounder?

Invinity Energy Systems: All About That BESS

Recently Updated Narratives

A SPAC in the Endgame Between Lifeboat and Siren Song

Mastercard: The Best Dividend Stock You're Ignoring

Luca Mining, $176M Revenue, Strong FCF, 200K Oz AuEq Vision & Debt-Free by Mid-2026

Popular Narratives

Investment Analysis (May 2026)

Adobe: A Probabilistic Case for Undervaluation