Advertisement

- United States

- /

- Software

- /

- NasdaqGS:DBX

Is Dropbox (DBX) Pricing Reflect Its Cash Flow Strength And Low P/E Ratio?

Reviewed by Bailey Pemberton

- If you have ever wondered whether Dropbox shares are pricing in too much optimism or not enough, you are not alone and valuation is exactly what this article is going to unpack.

- At a last close of US$27.28, the stock has recent returns of 1.3% over 7 days, 0.3% over 30 days, 1.3% year to date, 18.2% over 3 years, 23.6% over 5 years, and a 7.2% decline over the past year. These figures can change how investors think about both opportunity and risk.

- Recent coverage has focused on how investors are assessing cloud software names and subscription based models. This helps frame how moves in Dropbox's share price are being interpreted. This broader context is important when you are trying to judge whether current pricing reflects the company's cash flow profile and growth potential or leans more on sentiment.

- Right now Dropbox has a valuation score of 5 out of 6 on our checks, which suggests it screens as undervalued on most of them. Next we will walk through those methods before finishing with a way of thinking about value that goes beyond any single model.

Find out why Dropbox's -7.2% return over the last year is lagging behind its peers.

Approach 1: Dropbox Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, model takes Dropbox's expected future cash flows and then discounts them back to what they might be worth in today's dollars. It is essentially asking what a rational buyer might pay today for all of those future cash flows.

Dropbox's latest twelve month free cash flow is reported at about $906 million. Using a 2 Stage Free Cash Flow to Equity model, analysts have specific projections through to 2027, with free cash flow for that year at $935.1 million. Beyond that, Simply Wall St extrapolates cash flows out to 2035, with discounted values ranging from about $872.3 million in 2026 to $424.6 million in 2035.

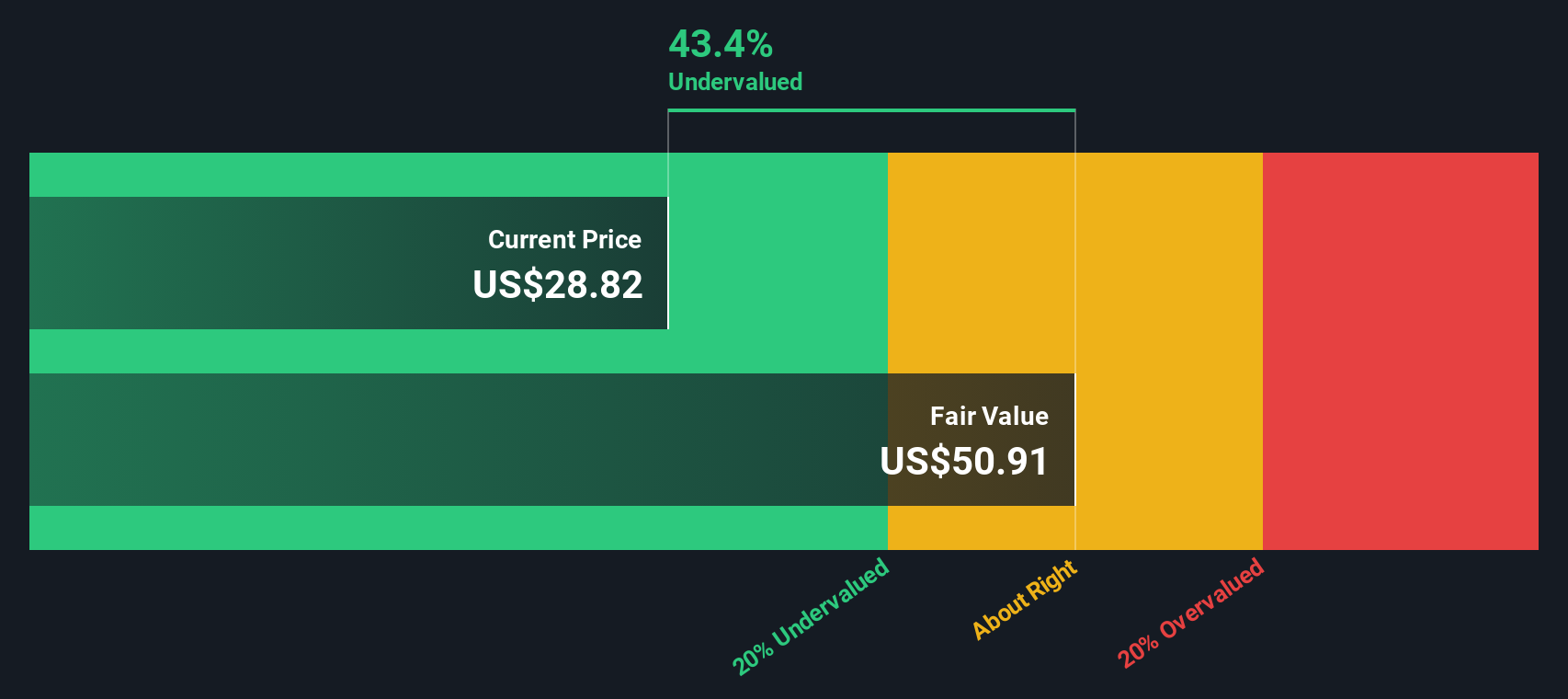

When all of those projected and discounted cash flows are added together, the model arrives at an estimated intrinsic value of US$49.44 per share. Compared with the recent share price of US$27.28, this implies a 44.8% discount, which indicates that Dropbox appears undervalued on this DCF view.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Dropbox is undervalued by 44.8%. Track this in your watchlist or portfolio, or discover 879 more undervalued stocks based on cash flows.

Approach 2: Dropbox Price vs Earnings

For a company that is generating earnings, the P/E ratio is a useful way to see how much you are paying for each dollar of profit. It also tends to reflect what the market is thinking about future growth and the risks around those earnings.

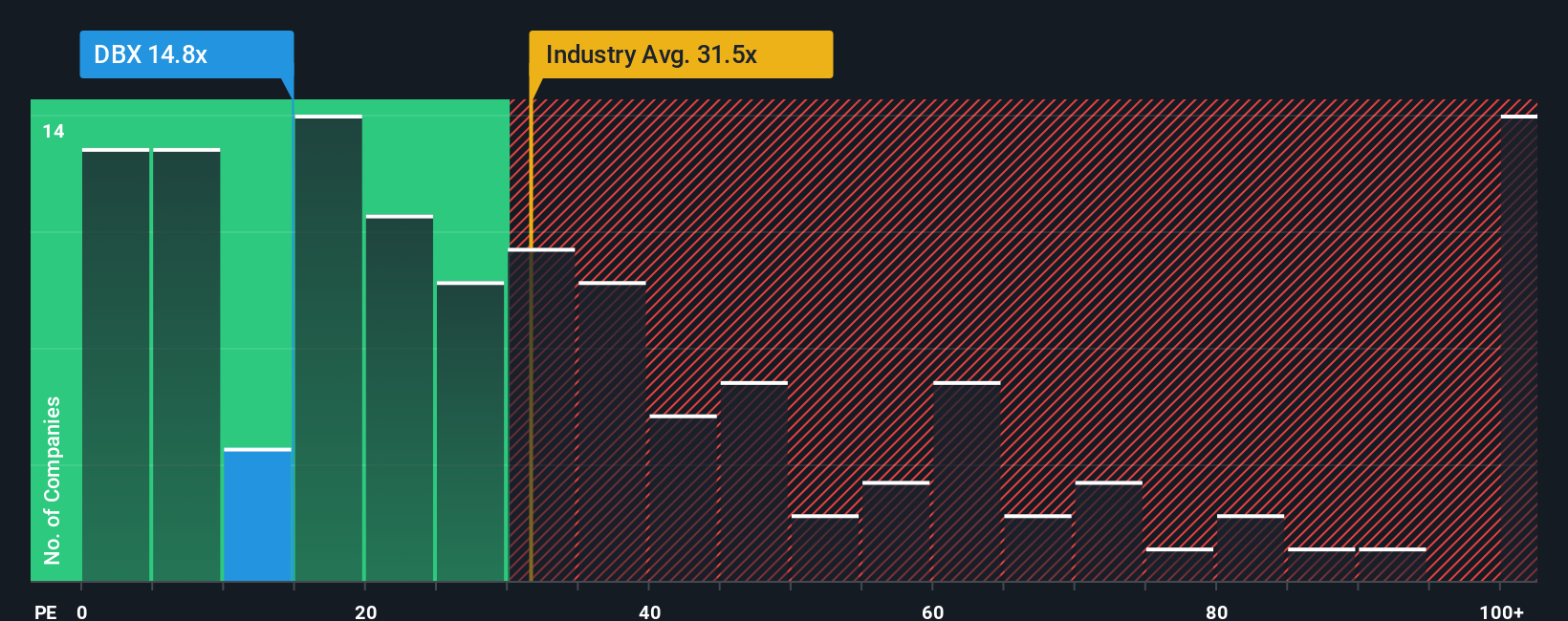

Higher growth expectations and lower perceived risk usually support a higher P/E, while slower growth or higher uncertainty often go with a lower P/E. Dropbox currently trades on a P/E of 14.0x, compared with the Software industry average of about 32.2x and a peer average of 22.0x, so it sits well below those simple benchmarks.

Simply Wall St also calculates a Fair Ratio of 24.2x. This is the P/E level it would expect for Dropbox after accounting for factors like earnings growth, profitability, industry, market cap and company specific risks. This Fair Ratio aims to be more tailored than a broad industry or peer comparison because it adjusts for the company’s own characteristics rather than relying on averages.

Comparing the Fair Ratio of 24.2x with the current P/E of 14.0x suggests Dropbox trades below this tailored valuation level.

Result: UNDERVALUED

P/E ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1444 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Dropbox Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. This is a simple way for you to attach a clear story about Dropbox to the numbers you care about, link that story to a financial forecast and a fair value, and then compare that fair value with the current price to help you decide whether to buy or sell, all within the Narratives tool on Simply Wall St's Community page. Views update as news or earnings arrive and can range from a more optimistic case that focuses on deeper AI integration, product tiers and margin strength to a more cautious view that centers on revenue declines, competition, pricing pressure and higher costs.

Do you think there's more to the story for Dropbox? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DBX

Dropbox

Provides a content collaboration platform in the United States and internationally.

Undervalued with acceptable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2537.9% undervalued

148 followersusers have followed this narrative

0 commentsusers have commented on this narrative

26 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0327.9% undervalued

33 followersusers have followed this narrative

3 commentsusers have commented on this narrative

11 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.521.1% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

4 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.723.9% undervalued

43 followersusers have followed this narrative

3 commentsusers have commented on this narrative

18 likesusers have liked this narrative

Recently Updated Narratives

MO

MontyNorman on Platform Group SE KGaA ·

Unbelievable numbers. Be very careful!

Fair Value:€26.8397.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Argenta Silver ·

Frank Giustra Backed: The High-Grade Silver Project Acquired for Just $3.5M Could Deliver 30x Silver Torque

Fair Value:CA$40.3598.8% undervalued

16 followersusers have followed this narrative

9 commentsusers have commented on this narrative

1 likeusers have liked this narrative

HU

Hunter_Z on Oriental Kopi Holdings Berhad ·

Oriental Kopi's Indonesia JV Strengthens Regional Growth Narrative

Fair Value:RM 1.531.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28021.8% undervalued

265 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9119.0% overvalued

131 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0942.7% undervalued

161 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0