- United States

- /

- Software

- /

- NasdaqGS:ADBE

Adobe (NasdaqGS:ADBE) Launches AI Innovations and NFL Partnership to Enhance Creative Experience

Reviewed by Simply Wall St

Adobe (NasdaqGS:ADBE) recently introduced over 100 new innovations in its Creative Cloud suite and expanded its partnership with the NFL, enhancing user engagement with generative AI tools and fan-oriented features. These developments likely supported Adobe's stock performance, which rose by 2.3% over the past week. This movement mirrors broader market trends, as the tech-heavy Nasdaq also climbed 2.3%, buoyed by strong earnings reports from chipmakers and other tech companies. Adobe's continued focus on creative solutions and strategic collaborations could be perceived as aligning well with current market optimism for tech-driven innovation.

Buy, Hold or Sell Adobe? View our complete analysis and fair value estimate and you decide.

The introduction of over 100 new innovations and expanded partnerships, like Adobe's with the NFL, highlights a shift towards enhanced user engagement and AI integration. While the recent 2.3% weekly rise in Adobe's stock supports this narrative, it's important to consider the longer-term performance. Over the past five years, Adobe's total return, including share price changes and dividends, was 0.80%. This aligns less favorably compared to the broader market, which returned 5.9% in the past year, indicating a dichotomy between short-term investor optimism and long-term shareholder returns.

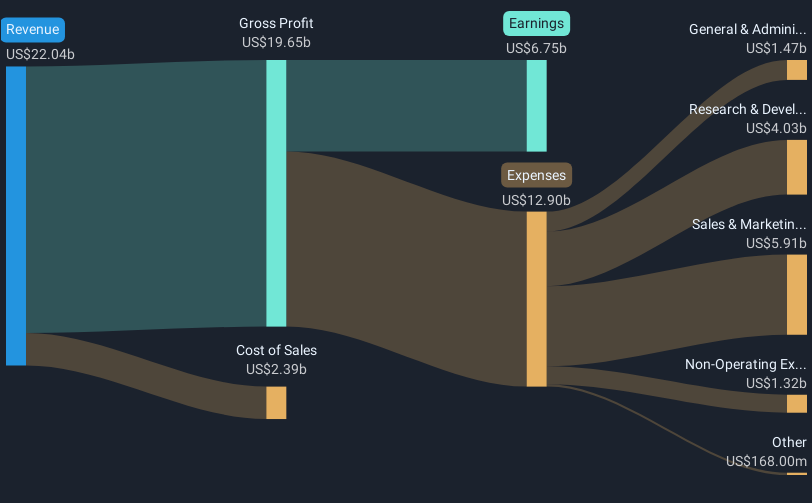

Adobe's focus on AI and expansion of web/mobile solutions could potentially influence revenue and earnings forecasts positively. The expansion of AI features, such as Firefly app tiers, aims to boost revenue and net margins through new user attraction and upsell opportunities. However, these ambitious plans entail execution risks, especially as analysts expect a 7% annual revenue growth over the next three years, alongside a slight decline in profit margins. With a current share price of US$351.96, the stock trades approximately 16.1% below the more bearish analyst price target of US$419.48, signifying potential for price appreciation but also reflecting divergent analyst views on Adobe's future prospects.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ADBE

Very undervalued with outstanding track record.

Similar Companies

Market Insights

Community Narratives