Advertisement

- United States

- /

- Specialty Stores

- /

- NYSE:CVNA

Could Carvana’s (CVNA) New Dallas Center Reveal Its Evolving Logistics Strategy?

Simply Wall St

Reviewed by Simply Wall St

- Carvana recently announced the expansion of its Inspection and Reconditioning Center capabilities at the ADESA Dallas wholesale auction site, adding operational capacity and creating around 150 new jobs in Hutchins, Texas.

- This move grows Carvana's national reconditioning network while increasing same-day delivery inventory and offering enhanced services to both retail and wholesale customers in the Dallas-Fort Worth area.

- We'll now explore how the integration of reconditioning operations at ADESA Dallas could influence Carvana's broader business outlook and growth narrative.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Carvana Investment Narrative Recap

To believe in Carvana, investors need confidence that online used car buying will continue to scale efficiently, with operations and logistics not becoming barriers to profitability as the company grows. The Dallas IRC integration expands Carvana’s network, which can incrementally address operational bottlenecks, a short-term catalyst for fulfillment and customer experience. However, the most pressing risk remains margin compression if these new facilities face delays or underutilization; this event is unlikely to materially change that risk in the near term.

Recently, Carvana also announced an expansion of IRC capabilities at its ADESA Seattle location, adding 100 jobs and increasing reconditioning throughput in the Pacific Northwest. This mirrors the Dallas announcement, highlighting management's commitment to bolstering operational infrastructure in markets with robust demand, a key component for delivering faster turnaround times, potentially affecting near-term margin and sales drivers.

Yet, in contrast to Carvana’s expansion and job growth, cost overruns and utilization delays at new sites remain risks investors should be aware of...

Read the full narrative on Carvana (it's free!)

Carvana's outlook anticipates $33.2 billion in revenue and $2.2 billion in earnings by 2028. This scenario assumes annual revenue growth of 26.8% and an increase in earnings of $1.6 billion from the current $563.0 million.

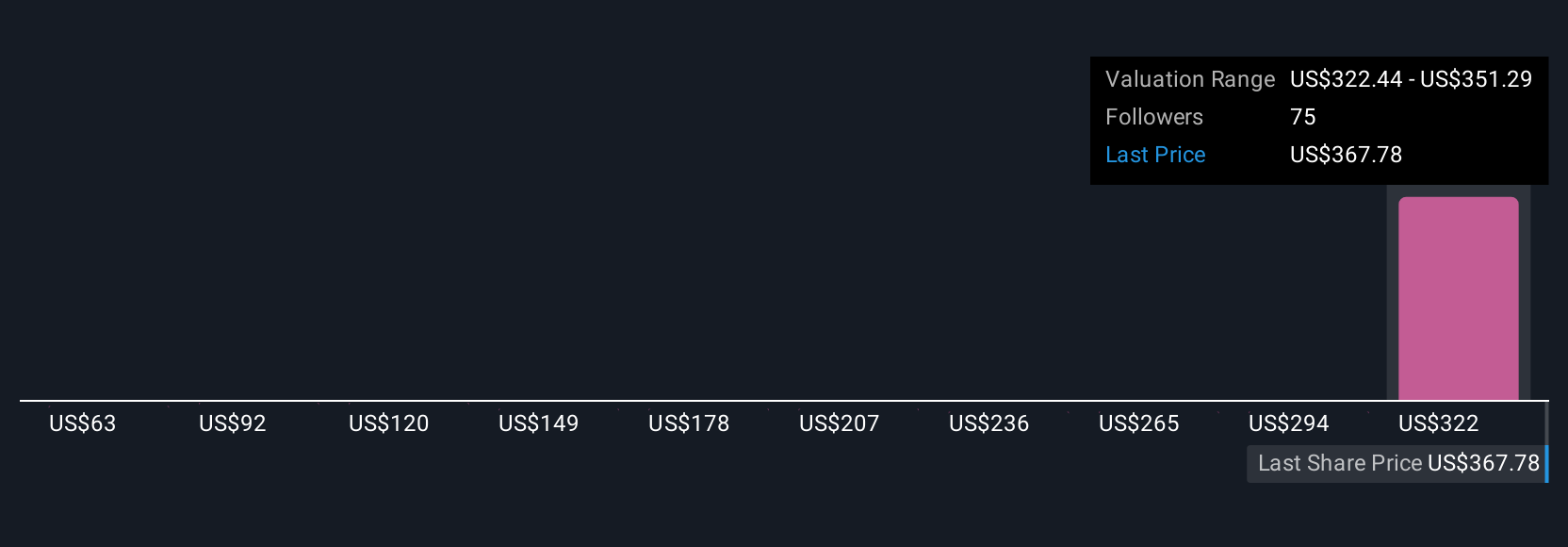

Uncover how Carvana's forecasts yield a $414.20 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Fifteen fair value estimates from the Simply Wall St Community span a wide range, from US$62.76 to US$500 per share. While some investors project substantial upside, the risk of margin pressure from underutilized facilities could weigh on actual outcomes, so review several viewpoints for a more balanced understanding.

Explore 15 other fair value estimates on Carvana - why the stock might be worth less than half the current price!

Build Your Own Carvana Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Carvana research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Carvana research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Carvana's overall financial health at a glance.

Interested In Other Possibilities?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CVNA

Carvana

Operates an e-commerce platform for buying and selling used cars in the United States.

Exceptional growth potential with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|75.8% undervalued

JO

Community Contributor

PayPal's Future Growth Through Venmo and Merchant Solutions

Fair Value US$105.25|34.2% undervalued

ZW

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$26.54|9.7% overvalued

BL

Community Contributor